Skip to comments.

Fed Admits Failure of ‘Plan A’ to Control Money Market Rates, Shifts Back to Repos ...

WolfStreet.com ^

| 20 September 2019

| Wolf Richter

Posted on 09/20/2019 11:35:56 PM PDT by Yosemitest

Fed Admits Failure of ‘Plan A’ to Control Money Market Rates,

Shifts Back to Repos (which was ‘Plan A’ till 2008)

The hullabaloo in the repo market torpedoed the function of Interest on Excess Reserves and forced the Fed to go back to the future.

With its announcement this morning, the New York Fed confirmed that the Fed’s Plan A of manipulating the federal funds rate into its target range – now between 1.75% and 2.0% — has miserably failed,

and that it will switch to Plan B to control short-term interest rates.

But this Plan B used to be Plan A that the Fed had routinely deployed to control short-term interest rates before the Financial Crisis.

So back to the future.

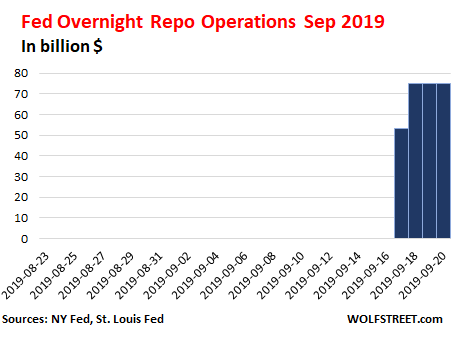

The “repo operations” the New York Fed has been conducting since Tuesday were overnight repurchase agreements (ultra-short-term loans),

where in the morning, the New York Fed offers up to $75 billion in cash at an interest rate that is within the Fed’s target range.

These loans are secured by collateral.

The allowed collateral are Treasury securities, Agency securities, and mortgage-backed securities guaranteed by the Government Sponsored Enterprises (GSEs).

These are overnight interest-bearing loans unwind the next morning, with the Fed getting its $75 billion in cash back, and the dealers getting their collateral back.

As these operations were undertaken every day for the past four days, it’s essentially the same $75 billion that gets recycled every day.

The daily amounts are not additive.

And these operations have nothing to do with QE.

Back in the day, the New York Fed used to conduct these repo operations routinely.

But in September 2008, when Lehman and AIG collapsed, the Fed switched from repo operations to emergency bailout loans, zero-interest-rate policy (ZIRP), QE, and other tricks and devices.

Repos were no longer needed to control rates.

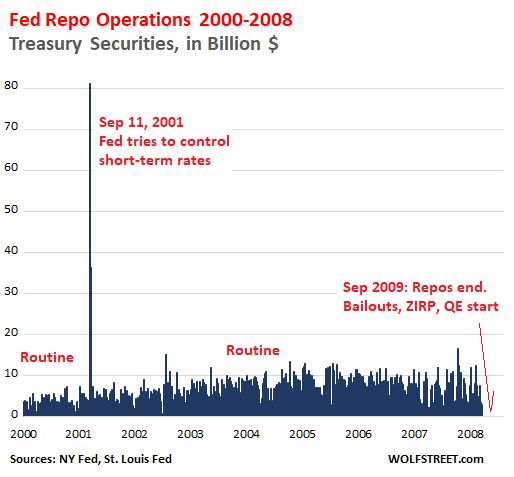

The chart below shows the tail-end of the era of repo operations through 2008.

The spike in repo operations following September 11, 2001, occurred when the Fed briefly injected massive amounts of cash via repos, as funding had dried up, and short-term rates were blowing out:

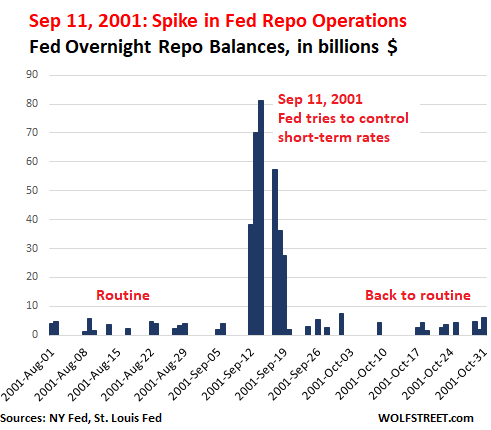

During the September 11, 2001 panic, the Fed conducted these massive repo operations for six mornings in a row.

Like all overnight repos, these repos unwound the next day, with the Fed getting its cash back and with banks getting their collateral back.

This chart shows the detail of those operations.

Note the amounts, reaching $81 billion on September 14, 2001.

Four days later, the operations were over, markets had settled down, overnight funding was plentiful, the Fed got its cash back, and the dealers got their collateral back:

In September 2008, when the US financial system was threatening to freeze up, the Fed developed new tools on the spot, including bailout emergency loans to banks, industrial companies, and market players under a variety of programs,

and it shifted to ZIRP and QE.

But it stopped the repo operations because they weren’t needed anymore.

Before the Financial Crisis, there were no Excess Reserves, which are deposits that banks park at the Fed to earn the interest, have instant liquidity, and fulfill regulatory capital and liquidity requirements.

Excess Reserves started piling up in parallel with QE and peaked in December 2014.

Since then, they have fallen by nearly half, to $1.38 trillion.

By paying banks interest on the Excess Reserves (IOER) at a rate equal to the upper limit of its target range, the Fed figured that banks would see to it that the federal funds rate would be less than the IOER.

This would keep the federal funds rate within the Fed’s target range.

This worked until it didn’t.

Throughout 2018, the federal funds rate hobbled along at the upper limit of the Fed’s target range and occasionally exceeded the limit.

The Fed reacted several times by adjusting the IOER to where it was further and further below the upper limit of its target range.

That worked until it didn’t.

And on Monday this week, all heck broke loose in the short-term funding market, which is precisely what the Fed is supposed to be able to keep under control.

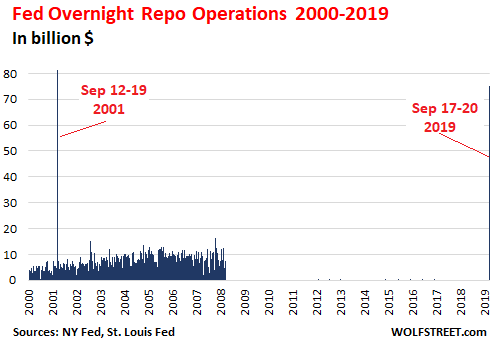

On Tuesday, the New York Fed announced its first repo operation since September 2008.

But the magnitude of the financial world has changed over those years: In 2001, the total amount of Treasury debt was $5.6 trillion.

Now it is over four times larger, $22.6 trillion.

Financialization of everything is a booming business,and the bets have gotten larger, the debt has gotten larger, there is more collateral, and so the amounts have gotten much larger.

If peak-repo day on Sep 14, 2001, is multiplied by four, in parallel with the growth of the US Treasury debt, an equivalent overnight repo operation today would amount to $244 billion.

So the $75 billion this morning is small fry.

In the chart below of 19 years of repo operations, the thin line on the right represents the past four days:

Just looking at the repo operations of the last 30 days:

Admission that Plan A failed; Plan B is now standard.

So here is what the New York Fed, which handles the repos, announced this morning “to help maintain the federal funds rate within the target range”:

1. Overnight repo operations will continue through October 10; on Sep 23, for “$75 billion”;

on the remaining days for “at least $75 billion.”

These repos unwind the next day, with the NY Fed getting its cash back and dealers getting their collateral back.

21. Three 14-day repo operations for “at least $30 billion each” (Sep 24, Sep 26, and Sep 27).

Each unwinds after 14 days, with the NY Fed getting its cash back, and dealers getting their collateral back.

3. After October 10, 2019, the NY Fed will conduct repo operations “as necessary to help maintain the federal funds rate in the target range.”

This third point is admission that the repo facility is now once again an integral part of managing short-term interest rates, as it was before September 2008.

The St. Louis Fed already proposed this months ago.

The St. Louis Fed published two papers on the benefits of a “Standing Repo Facility,” This standing repo facility is now in operation, officialized by the New York Fed as of this morning.

The two key – but “distinct” – motivations for a standing repo facility are, as cited in the follow-up paper:

First, the facility could be used to support interest rate control by establishing a ceiling on repo rates, thereby guarding against unwanted spikes in money market rates.

The use of a ceiling tool for this purpose would be seen as enhancing the monetary policy operating regime of the FOMC.

Second, the facility could be used to reduce the demand for reserves for any given rate of interest on excess reserves.

The first motivation is why the NY Fed uses the facility now: to control spikes in money market rates as seen over the past week

and keep the federal funds rate within the Fed’s target range.

The second motivation would be to reduce the excess reserves presumably needed to control the federal funds rate via the IOER.

These reserves and the IOER would become less important, because repo operations now pick up much of the work of controlling money market rates.

And the level of those reserves (currently $1.38 trillion) could be reduced further, allowing the Fed’s balance sheet to shrink further:

Why the desire to minimize the demand for reserves ?

In short, because it accords with the FOMC’s stated preference to operate a floor system with the minimum level of reserves necessary to permit the efficient and effective conduct of monetary policy: “minimally ample reserves” for short.

So this standing repo facility, as we’re looking at it today, takes pressure off those reserves,

and it takes the Fed back a step closer to managing short term rates as it used to do before the Financial Crisis.

Nevertheless, the fact that the Fed was forced all of a sudden by a panicky market to abandon Plan A and revert to how it used to do it, rather than implementing the transition methodically, on its own, in its gradual manner,

must have come as a shock.

TOPICS: Business/Economy; Extended News; Government; News/Current Events

KEYWORDS: bailout; bank; blackswan; debt; deficit; fed; fedrate; inflation; mmt; modernmonetarytheory; moneyprinting; qe; repurchaseagreement

Navigation: use the links below to view more comments.

first previous 1-20, 21-40, 41-60, 61-80 ... 101-120 next last

To: babble-on

what conspiracy theory is that? I was asking for an explanation on what the Fed is doing now, in simple terms. I don’t need anyone to tell me about the derivatives market and all that other Wall St bullsh*t and then accuse me of wearing tinfoil hat.

And thinking that they big banks, the Fed and Wall St are screwing us over, isn’t a conspiracy, in any shape or form.

21

posted on

09/21/2019 6:44:08 AM PDT

by

qaz123

To: qaz123

The Fed’s employees are paid a fraction of what they would make doing similar jobs in the private sector and all the net profits the Fed earns from its operations are refunded to the American people’s Treasury, averaging about $100 billion a year in recent times.

To: Yosemitest

Raise your hand if you believed the big banks were not under collateralized.

23

posted on

09/21/2019 7:24:34 AM PDT

by

Georgia Girl 2

(The only purpose of a pistol is to fight your way back to the rifle you should never have dropped)

To: Yosemitest

I believe the FED is planning to engineer a market downturn for next year’s election just like they did last year.

24

posted on

09/21/2019 7:25:33 AM PDT

by

OrioleFan

(Republicans believe every day is July 4th, Democrats believe every day is April 15th.)

To: Moonman62

The Fed prints all money out of thin air then lends it to us at interest. All US dollars are debt from inception. Thats the problem. Trump knows this.

25

posted on

09/21/2019 7:30:26 AM PDT

by

Georgia Girl 2

(The only purpose of a pistol is to fight your way back to the rifle you should never have dropped)

To: qaz123

The sole purpose of the Federal Reserve is to transfer wealth from the people to banks and corporations. That is all.

26

posted on

09/21/2019 7:32:57 AM PDT

by

Georgia Girl 2

(The only purpose of a pistol is to fight your way back to the rifle you should never have dropped)

To: Herakles

For some reason I feel like I’m driving down the road and have just seen a big fat bug hit the windshield.

And it’s blocking the view of the 400 lb rutting buck deer that is about to jump out in the road in your lane while you’re traveling 80 mph.

27

posted on

09/21/2019 7:39:03 AM PDT

by

Old Yeller

(Auto-correct has become my worst enema.)

To: Yosemitest

Two very long articles filled with good information and then you come up with a conclusion that makes no sense.

“...to operate a floor system with the minimum level of reserves necessary to permit the efficient and effective conduct of monetary policy:

“minimally ample reserves” for short.”

The Fed controls short term rates AND dictates overnight bank holding requirements. TWO different things.

Increasing or decreasing reserve requirements is meant to provide liquidity, prevent a “run on the bank” and goes hand in hand with a “tight or loose money” stance. With inflation low there is no reason for “tight money” now.

This is a return to normalcy from Keynesian insanity of the Obama years.

28

posted on

09/21/2019 8:19:44 AM PDT

by

jdsteel

(Americans are Dreamers too!!!)

To: dp0622

“10 percent overnight? Wow.”

That’s 10% annualized. Overnight they got 1/365th of 10% thanks to a short term situation.

Not so Wow.

29

posted on

09/21/2019 8:21:48 AM PDT

by

jdsteel

(Americans are Dreamers too!!!)

To: jdsteel

Well yeah it is compared to 1/365th of 2.5 percent.

I’d say 4 times more is wow.

30

posted on

09/21/2019 9:07:33 AM PDT

by

dp0622

(Bad, bad company Till the day I die.)

To: RummyChick

>>>Trump has really hired some disastrous people. Powell is one of them

Are you kidding? I have it on very good sources that this is all part of a brilliant plan to destroy the FED. Heard it on X22 report (yes-I’m serious). You see-Trump hires Powell to destroy the Economy so the FED would take the blame and the country will be smart enough to know that this disaster is not Trumps fault-but the Fed’s. Yes-seriously.

31

posted on

09/21/2019 9:15:41 AM PDT

by

NELSON111

(Congress: The Ralph Wolf and Sam Sheepdog s<how. Theater for sheep. My politics determines my "hero")

To: babble-on

So you’re a fan of a central bank, that nowhere in the Constitution states that there should be one? You’re a fan of a group of people that can manipulate our economy however they want?

When you say its employees are paid a fraction of they would make doing similar jobs, feel free to provide an example. Not that I give a damn what any of them get paid.

It is a private bank that has no accountability to the American people. When talk of an audit is brought about folks get worried. I wonder why.

But, then again, entrusting our economy to the likes of Waters, Pelosi, AOC, Omar, Tlaib, Pressley, Schumer, Sanders, Harris, Warren and a whole slew of Republican’s is absolutely frightening.

32

posted on

09/21/2019 9:19:21 AM PDT

by

qaz123

To: Georgia Girl 2

not according to fellow commenter, babble-on. He/she apparently thinks the Fed is wonderful.

33

posted on

09/21/2019 9:21:32 AM PDT

by

qaz123

To: Georgia Girl 2

The Fed prints all money out of thin air then lends it to us at interest.I've got some FRNs in my wallet, no one ever came looking for interest from me. Who do you pay? How much? Where do you mail the check?

To: dp0622; Yosemitest; qaz123

The jump in overnight rates was an extremely brief spike that coincided with a tax payment deadline for large corporations, and a holiday in Japan which meant that normal borrowing there wasn’t available so it went here.

This article is making a big deal out of nothing.

35

posted on

09/21/2019 11:41:33 AM PDT

by

Pelham

(Secure Voter ID. Mexico has it, because unlike us they take voting seriously)

To: Pelham

Thank you for the insight.

36

posted on

09/21/2019 11:49:37 AM PDT

by

dp0622

(Bad, bad company Till the day I die.)

To: qaz123

The Fed can’t “enrich itself”. All income above salaries and normal expenses goes directly to the US Treasury. It’s been that way since day one.

The Fed began as a compulsory association of all nationally chartered American banks. You have to join, it’s not voluntary. It’s not a commercial bank. It’s job is to provide liquidity to the banking system to prevent a system collapse. All of the buying and selling of bonds it engages in is for adjusting the money supply available to commercial banks.

“I understand completely how the Fed has taken over our banking system and they set the rates for loans, credit cards, etc. So, if the Fed disappeared tomorrow and the banks were forced to set their own rates, how does that happen and what would it mean for us?”

We would go back to what existed before. Presidents would have to run hat in hand to the biggest money center bank and beg them to do something to keep the American economy from collapsing. Back then it was JP Morgan’s bank. So you’d go from our current system, which has some gov’t input, back to the days when there was no gov’t involvement at all. And you better hope that the big banker is another patriot like Morgan or you’re in a world of trouble. Today you’d likely be begging some Saudi prince or Chinese apparatchik for help.

“I think it’s pretty obvious that the Fed and Big Banks act in collusion to screw over their captive audience, all of us, every chance they get to make more and more money, while we get left holding the bag.”

The illusion that guarantees an endless audience for conspiracy theories.

37

posted on

09/21/2019 12:01:50 PM PDT

by

Pelham

(Secure Voter ID. Mexico has it, because unlike us they take voting seriously)

To: qaz123; Georgia Girl 2; babble-on

“not according to fellow commenter, babble-on. He/she apparently thinks the Fed is wonderful.”

That’s what happens when you read the history of the Panic of 1907, the Aldrich-Vreeland Act, the National Monetary Commission, and other dull stuff like the issuance of Clearinghouse receipts as emergency money.

Conspiracy stories are much more entertaining and I highly recommend them instead.

38

posted on

09/21/2019 12:12:52 PM PDT

by

Pelham

(Secure Voter ID. Mexico has it, because unlike us they take voting seriously)

To: Pelham

History, logic and facts have no place in a discussion of the evil Federal Reserve.

To: central_va

“Repeal the 16th amendment!!!”

That made the income tax legal. Didn’t have anything to do with the Federal Reserve, which was created by an act of Congress.

40

posted on

09/21/2019 12:20:51 PM PDT

by

Pelham

(Secure Voter ID. Mexico has it, because unlike us they take voting seriously)

Navigation: use the links below to view more comments.

first previous 1-20, 21-40, 41-60, 61-80 ... 101-120 next last

Disclaimer:

Opinions posted on Free Republic are those of the individual

posters and do not necessarily represent the opinion of Free Republic or its

management. All materials posted herein are protected by copyright law and the

exemption for fair use of copyrighted works.

FreeRepublic.com is powered by software copyright 2000-2008 John Robinson