Skip to comments.

Fed Admits Failure of ‘Plan A’ to Control Money Market Rates, Shifts Back to Repos ...

WolfStreet.com ^

| 20 September 2019

| Wolf Richter

Posted on 09/20/2019 11:35:56 PM PDT by Yosemitest

Fed Admits Failure of ‘Plan A’ to Control Money Market Rates,

Shifts Back to Repos (which was ‘Plan A’ till 2008)

The hullabaloo in the repo market torpedoed the function of Interest on Excess Reserves and forced the Fed to go back to the future.

With its announcement this morning, the New York Fed confirmed that the Fed’s Plan A of manipulating the federal funds rate into its target range – now between 1.75% and 2.0% — has miserably failed,

and that it will switch to Plan B to control short-term interest rates.

But this Plan B used to be Plan A that the Fed had routinely deployed to control short-term interest rates before the Financial Crisis.

So back to the future.

The “repo operations” the New York Fed has been conducting since Tuesday were overnight repurchase agreements (ultra-short-term loans),

where in the morning, the New York Fed offers up to $75 billion in cash at an interest rate that is within the Fed’s target range.

These loans are secured by collateral.

The allowed collateral are Treasury securities, Agency securities, and mortgage-backed securities guaranteed by the Government Sponsored Enterprises (GSEs).

These are overnight interest-bearing loans unwind the next morning, with the Fed getting its $75 billion in cash back, and the dealers getting their collateral back.

As these operations were undertaken every day for the past four days, it’s essentially the same $75 billion that gets recycled every day.

The daily amounts are not additive.

And these operations have nothing to do with QE.

Back in the day, the New York Fed used to conduct these repo operations routinely.

But in September 2008, when Lehman and AIG collapsed, the Fed switched from repo operations to emergency bailout loans, zero-interest-rate policy (ZIRP), QE, and other tricks and devices.

Repos were no longer needed to control rates.

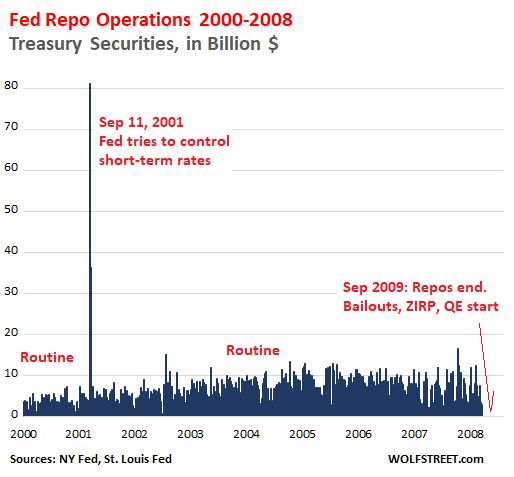

The chart below shows the tail-end of the era of repo operations through 2008.

The spike in repo operations following September 11, 2001, occurred when the Fed briefly injected massive amounts of cash via repos, as funding had dried up, and short-term rates were blowing out:

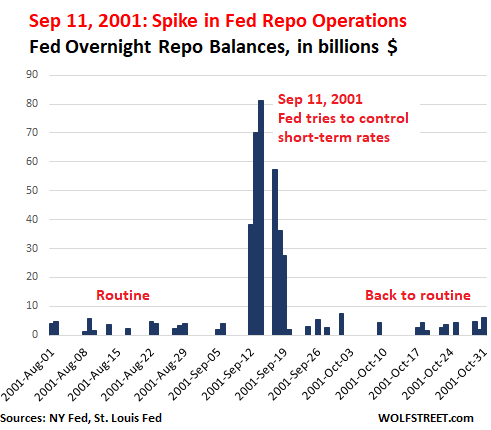

During the September 11, 2001 panic, the Fed conducted these massive repo operations for six mornings in a row.

Like all overnight repos, these repos unwound the next day, with the Fed getting its cash back and with banks getting their collateral back.

This chart shows the detail of those operations.

Note the amounts, reaching $81 billion on September 14, 2001.

Four days later, the operations were over, markets had settled down, overnight funding was plentiful, the Fed got its cash back, and the dealers got their collateral back:

In September 2008, when the US financial system was threatening to freeze up, the Fed developed new tools on the spot, including bailout emergency loans to banks, industrial companies, and market players under a variety of programs,

and it shifted to ZIRP and QE.

But it stopped the repo operations because they weren’t needed anymore.

Before the Financial Crisis, there were no Excess Reserves, which are deposits that banks park at the Fed to earn the interest, have instant liquidity, and fulfill regulatory capital and liquidity requirements.

Excess Reserves started piling up in parallel with QE and peaked in December 2014.

Since then, they have fallen by nearly half, to $1.38 trillion.

By paying banks interest on the Excess Reserves (IOER) at a rate equal to the upper limit of its target range, the Fed figured that banks would see to it that the federal funds rate would be less than the IOER.

This would keep the federal funds rate within the Fed’s target range.

This worked until it didn’t.

Throughout 2018, the federal funds rate hobbled along at the upper limit of the Fed’s target range and occasionally exceeded the limit.

The Fed reacted several times by adjusting the IOER to where it was further and further below the upper limit of its target range.

That worked until it didn’t.

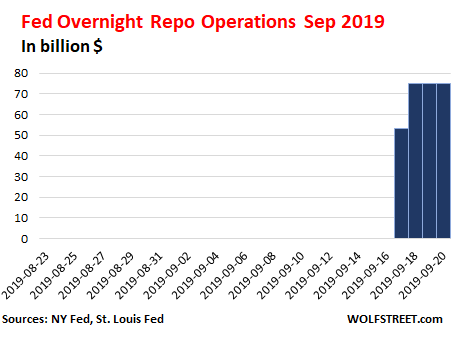

And on Monday this week, all heck broke loose in the short-term funding market, which is precisely what the Fed is supposed to be able to keep under control.

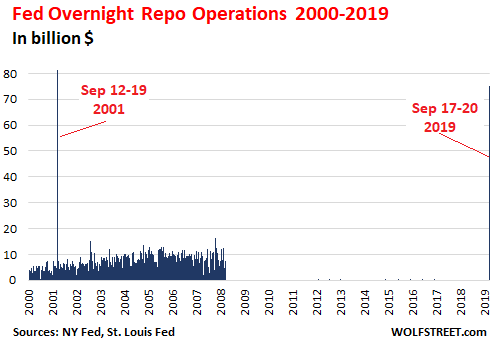

On Tuesday, the New York Fed announced its first repo operation since September 2008.

But the magnitude of the financial world has changed over those years: In 2001, the total amount of Treasury debt was $5.6 trillion.

Now it is over four times larger, $22.6 trillion.

Financialization of everything is a booming business,and the bets have gotten larger, the debt has gotten larger, there is more collateral, and so the amounts have gotten much larger.

If peak-repo day on Sep 14, 2001, is multiplied by four, in parallel with the growth of the US Treasury debt, an equivalent overnight repo operation today would amount to $244 billion.

So the $75 billion this morning is small fry.

In the chart below of 19 years of repo operations, the thin line on the right represents the past four days:

Just looking at the repo operations of the last 30 days:

Admission that Plan A failed; Plan B is now standard.

So here is what the New York Fed, which handles the repos, announced this morning “to help maintain the federal funds rate within the target range”:

1. Overnight repo operations will continue through October 10; on Sep 23, for “$75 billion”;

on the remaining days for “at least $75 billion.”

These repos unwind the next day, with the NY Fed getting its cash back and dealers getting their collateral back.

21. Three 14-day repo operations for “at least $30 billion each” (Sep 24, Sep 26, and Sep 27).

Each unwinds after 14 days, with the NY Fed getting its cash back, and dealers getting their collateral back.

3. After October 10, 2019, the NY Fed will conduct repo operations “as necessary to help maintain the federal funds rate in the target range.”

This third point is admission that the repo facility is now once again an integral part of managing short-term interest rates, as it was before September 2008.

The St. Louis Fed already proposed this months ago.

The St. Louis Fed published two papers on the benefits of a “Standing Repo Facility,” This standing repo facility is now in operation, officialized by the New York Fed as of this morning.

The two key – but “distinct” – motivations for a standing repo facility are, as cited in the follow-up paper:

First, the facility could be used to support interest rate control by establishing a ceiling on repo rates, thereby guarding against unwanted spikes in money market rates.

The use of a ceiling tool for this purpose would be seen as enhancing the monetary policy operating regime of the FOMC.

Second, the facility could be used to reduce the demand for reserves for any given rate of interest on excess reserves.

The first motivation is why the NY Fed uses the facility now: to control spikes in money market rates as seen over the past week

and keep the federal funds rate within the Fed’s target range.

The second motivation would be to reduce the excess reserves presumably needed to control the federal funds rate via the IOER.

These reserves and the IOER would become less important, because repo operations now pick up much of the work of controlling money market rates.

And the level of those reserves (currently $1.38 trillion) could be reduced further, allowing the Fed’s balance sheet to shrink further:

Why the desire to minimize the demand for reserves ?

In short, because it accords with the FOMC’s stated preference to operate a floor system with the minimum level of reserves necessary to permit the efficient and effective conduct of monetary policy: “minimally ample reserves” for short.

So this standing repo facility, as we’re looking at it today, takes pressure off those reserves,

and it takes the Fed back a step closer to managing short term rates as it used to do before the Financial Crisis.

Nevertheless, the fact that the Fed was forced all of a sudden by a panicky market to abandon Plan A and revert to how it used to do it, rather than implementing the transition methodically, on its own, in its gradual manner,

must have come as a shock.

TOPICS: Business/Economy; Extended News; Government; News/Current Events

KEYWORDS: bailout; bank; blackswan; debt; deficit; fed; fedrate; inflation; mmt; modernmonetarytheory; moneyprinting; qe; repurchaseagreement

Navigation: use the links below to view more comments.

first 1-20, 21-40, 41-60, 61-80 ... 101-120 next last

Also there's this article from Sept 18, 2019.

Explainer: The Fed Has a Repo Problem.

What's That ?

As if the U.S. Federal Reserve didn't already have enough on its plate heading into its meeting on interest rates this week, chaos deep inside the plumbing of the U.S. financial system has thrown policymakers an unexpected curveball.

Cash available to banks for their short-term funding needs all but dried up on Monday and Tuesday, and interest rates in U.S. money markets shot up to as high as 10% for some overnight loans, more than four times the Fed's rate.

That forced the Fed to make an emergency injection of more than $50 billion, its first since the financial crisis more than a decade ago, to prevent borrowing costs from spiraling even higher.

It will conduct another one on Wednesday.

The exact cause of the squeeze is a matter of some debate, but most market participants agree that two coincidental events on Monday were at least partly to blame. First, corporations had to withdraw funds from money market accounts to pay for quarterly tax bills,

and then on the same day the banks and investors who bought the $78 billion of U.S.

Treasury notes and bonds sold by Uncle Sam last week had to settle up.

On top of that, the reserves that banks park with the Fed and are often made available to other banks on an overnight basis are at their lowest since 2011

thanks to the central bank's culling of its vast portfolio of bonds over the past few years.

Added together, these factors are testing the limits of the $2.2 trillion repurchase agreement - or repo - market, a gray but essential component of the U.S. financial system.

Whatever the cause, the episode has added fuel to the argumentthat the Fed needs to take steps to avoid more disruptions in the repo market down the road.

WHY IS THE REPO MARKET IMPORTANT ?

The repo market underpins much of the U.S. financial system, helping to ensure banks have the liquidity to meet their daily operational needs and maintain sufficient reserves.

In a repo trade, Wall Street firms and banks offer U.S. Treasuries and other high-quality securities as collateral to raise cash, often overnight, to finance their trading and lending activities.

The next day, borrowers repay their loans plus what is typically a nominal rate of interest and get their bonds back. In other words, they repurchase, or repo, the bonds.

The system typically hums along with the interest rate charged on repo deals hovering close to the Fed's benchmark overnight rate, currently set in a range of 2.00% to 2.25%.

That rate is expected to be cut by a quarter percentage point on Wednesday.

But sometimes, investors get fearful of lending, as seen during the global credit crisis,

or at other times there are just not enough reserves or cash in the system to lend out, as appeared to be the case this week.

And that can cause a squeeze on the market and send borrowing costs zooming higher.

But when investors get fearful of lending, as seen during the global credit crisis, or when there are just not enough reserves or cash in the system to lend out, it sends the repo rate soaring above the Fed Funds rate.

Trading in stocks and bonds can become difficult.

It can also pinch lending to businesses and consumers and, if the disruption is prolonged, it can become a drag on a U.S. economy that relies heavily on the flow of credit.

WHAT HAS CAUSED THE DROP IN BANK RESERVES ?

Coming out of the financial crisis, after the Fed cut interest rates to near zero and bought more than $3.5 trillion of bonds, banks built up massive reserves held at the Fed.

But that level of bank reserves, which peaked at nearly $2.8 trillion, began falling when the Fed started raising interest rates in late 2015.

They fell even faster when the Fed started to cut the size of its bond portfolio about two years later.

The Fed stopped raising interest rates last year and cut them in July and is expected to do so again on Wednesday.

It has also now ceased allowing to bonds to roll off its balance sheet.

The question vexing policymakers now is whether those actions are enough to stop the downward drift in reserves, which are a main source of liquidity in funding markets like repo.

Bank reserves at the Fed last stood at $1.47 trillion, the lowest level since 2011 and nearly 50% below their peak from five years ago.

WHAT CAN THE FED DO TO CALM THE REPO MARKET ?

1. RUN SPOT REPO OPERATIONS

Through the Federal Reserve Bank of New York, the Fed can conduct occasional spot repo operations at times of funding stress, allowing banks and dealers to swap their Treasuries and other high-quality securities for cash at a minimal interest rate.

It did this on Tuesday and will do it again on Wednesday.

2. LOWER THE INTEREST IT PAYS ON EXCESS RESERVES

By making it less profitable for banks, especially foreign ones, to leave their reserves at the Fed, it may encourage banks to lend to each other in money markets.

3. CREATE A STANDING REPO FACILITY

Such a permanent financing program will allow eligible participants to exchange their bonds for cash at a set interest rate.

Fed and its staff have considered such a facility, but they have not determined who qualifies, what would be the level of interest paid and the timing for a possible launch.

4. RAMP UP BUYING OF TREASURIES

The Fed can replenish the level of bank reserves by slightly increasing its holdings of U.S. government debt.

This comes with the risk that it may be perceived as a resurrection of quantitative easing rather than a technical adjustment.

----------------------------------------------------------------------

Well, here we go again,

back intoBAILING OUT BANKS,

and THE FEDERAL RESERVE JUST PRINTING MONEY OUT OF THIN AIR !

To: Yosemitest

10 percent overnight? Wow.

2

posted on

09/20/2019 11:40:01 PM PDT

by

dp0622

(Bad, bad company Till the day I die.)

To: Yosemitest

For some reason I feel like I’m driving down the road and have just seen a big fat bug hit the windshield.

Just one of those feelings ya know.

3

posted on

09/20/2019 11:54:22 PM PDT

by

Herakles

(Diversity is applied Marxism!)

To: Yosemitest

4

posted on

09/21/2019 12:50:07 AM PDT

by

MarMema

To: Yosemitest

Trump has really hired some disastrous people. Powell is one of them

5

posted on

09/21/2019 1:44:33 AM PDT

by

RummyChick

("Pills, money .. this city is wicked. Your best friend will kill you here." Smoove about Baltimore)

To: Yosemitest

The problems elites have manipulating the markets.

6

posted on

09/21/2019 2:41:53 AM PDT

by

Moonman62

(Charity comes from wealth.)

To: Yosemitest

Well, here we go again,

back into

BAILING OUT BANKS,

and THE FEDERAL RESERVE JUST PRINTING MONEY OUT OF THIN AIR !

...

Did the you read the articles you posted?

7

posted on

09/21/2019 2:45:32 AM PDT

by

Moonman62

(Charity comes from wealth.)

To: Yosemitest

Due to the nature of my work I’ve been following this nonstop over the week. I believe though this is the first time anyone is posting it on FR

8

posted on

09/21/2019 2:56:23 AM PDT

by

spetznaz

(Nuclear-tipped Ballistic Missiles: The Ultimate Phallic Symbol)

To: Yosemitest

bookmrking

fed awaits a failure of plan a to control money market rates, shifts back to repo...

9

posted on

09/21/2019 3:02:12 AM PDT

by

SteveH

(intentionally blank)

To: Yosemitest

Admittedly, not a financial guy and have very basic understanding of the markets and Wall St. That doesn’t make me a bad guy or an idiot as some on this page would automatically assume. I could have went the Wall St/banking route like many of friends, I chose not too. That being said.....

Can someone explain, in layman’s terms, what this means and how the Fed seems to be, once again, playing a game to enrich itself and its cronies on Wall St, and the taxpayer will end up footing the bill if it all sh*ts the bed?

I understand completely how the Fed has taken over our banking system and they set the rates for loans, credit cards, etc. So, if the Fed disappeared tomorrow and the banks were forced to set their own rates, how does that happen and what would it mean for us?

I think it’s pretty obvious that the Fed and Big Banks act in collusion to screw over their captive audience, all of us, every chance they get to make more and more money, while we get left holding the bag.

10

posted on

09/21/2019 4:13:19 AM PDT

by

qaz123

To: qaz123

I think it’s pretty obvious that the Fed and Big Banks act in collusion to screw over their captive audience, all of us, every chance they get to make more and more money, while we get left holding the bag.

—

I remember long ago hearing interview with the author of a book called “The Creature from Jekyll Island” about the creation of the Federal Reserve. The takeaway line I remember from the interview was that the you hear the phrase “Federal Reserve” this “banking cartel”, because that’s what it is and that’s who it serves.

11

posted on

09/21/2019 4:52:01 AM PDT

by

Flick Lives

(MSM, the Enemy of the People since 1898)

To: Yosemitest

In 2008, overnight rates rose because firms didn’t trust their counterparties or their collateral. In this case, rates are being driven up by a lack of supply - banks have to hold more reserves post-crisis, other firms were making tax payments. There will likely be a shortage again at the end of this month when a bunch of Treasuries expire.

12

posted on

09/21/2019 5:25:08 AM PDT

by

oincobx

To: Yosemitest

The New York Fed fired their chief of market operations earlier this year, Mr. Simon Potter. The new guy was apparently not ready for prime time.

To: qaz123

If you’re not a financial guy, don’t make the first thing you read about the Fed be a paranoid conspiracy theory.

To: Flick Lives

Yup....just heard about that book, recently. I’m afraid to read it. But like so many things, it’s one of those things that I wish the President would bring up one day, during one of his off the cuff pressers, like the ones he does by Marine 1.

Something like....”You know, I just got done reading this book, The Creature From Jekyll Island. Eye opening book. Learned alot. When I get back from this trip I’m going to talk some folks about it. Probably be a good book for all of America to read.” And just walk away.

Then we can all watch that book fly off the shelves, the MSM and Wall St go into complete panic mode as he stirs up the masses. Getting a bill passed to audit the Fed, will go through Congress like a hot knife through butter, I think.

But then again, there are a lot of things the President could make mention of that could get people to learn a little more about what is going on and what has gone on. Even if he put it out on Twitter....

Everything about immigration by Dennis Michael Lynch ...... eye opening stuff America: Freedom to Fascism

What’s interesting, as disgusting as he is as a human, Alan Grayson tears them up in hearings. When he was in Congress, there are multiple videos of him, on Youtube, getting on them about all sorts of stuff I don’t understand. Personally, I think he’s about as disgusting as they come, but if an audit ever came and he was legit about the Fed, I’d put him on a committee to do the audit.

15

posted on

09/21/2019 6:06:13 AM PDT

by

qaz123

To: babble-on

Repeal the 16th amendment!!!

16

posted on

09/21/2019 6:06:24 AM PDT

by

central_va

(I won't be reconstructed and I do not give a damn.)

To: oincobx

As bonds and CDs mature now in my retirement portfolio, there is really no incentive to renew them since they pay no more than Schwab money market rates, in most cases.

And, if I do look for something else, the long term rates are, in many cases, no more than the short term rates. So I have renewed 90 days CDs and little else.

17

posted on

09/21/2019 6:12:34 AM PDT

by

Vigilanteman

(The politicized state destroys aspects of civil society, human kindness and private charity.)

To: central_va

To: babble-on

That doesn’t make me a bad guy or an idiot as some on this page would automatically assume....and obviously you made that assumption, shocking.

I’m not paranoid. Just asked for simple explanation, that’s all. But once again, you’ve proven that there are folks on FR that are so f*cking smart they should have monuments built for them. Instead of, possibly, explaining it and providing some insight, you’re a condescending asshole. Nothing but a D-bag.

19

posted on

09/21/2019 6:34:35 AM PDT

by

qaz123

To: qaz123

You didn’t ask for a simple explanation of what happened, you asked for an explanation in terms that comported with the conspiracy theory you’ve already embraced.

Navigation: use the links below to view more comments.

first 1-20, 21-40, 41-60, 61-80 ... 101-120 next last

Disclaimer:

Opinions posted on Free Republic are those of the individual

posters and do not necessarily represent the opinion of Free Republic or its

management. All materials posted herein are protected by copyright law and the

exemption for fair use of copyrighted works.

FreeRepublic.com is powered by software copyright 2000-2008 John Robinson