Posted on 03/12/2023 4:36:51 PM PDT by DoodleBob

"When you’re not working, what do you do to de-stress?”

That was the last question Greg Becker, CEO of Silicon Valley Bank, fielded at an investor conference on Tuesday this week.

“Cycling is my advice,” he replied. “Living in Northern California and being on the peninsula. That’s just—I think it’s the best bike-riding cycling in the world, period.”

Three days later, Becker’s bank is in receivership.

We’ve talked before about the interest rate risk that lurks on banks’ balance sheets and how the industry manages it. During the pandemic, banks took in record volumes of new deposits. Between the end of 2019 and the first quarter of 2022, deposits at US banks rose by $5.40 trillion. With loan demand weak, only around 15% of that volume was channelled towards loans; the rest was invested in securities portfolios or kept as cash. Securities portfolios ballooned to $6.26 trillion, up from $3.98 trillion at the end of 2019, and cash balances went up to $3.38 trillion from $1.67 trillion.

When banks purchase securities, they are forced to decide up-front whether they intend to hold them to maturity. The decision dictates whether the securities are designated as “held-to-maturity” (HTM) assets or as “available-for-sale” (AFS) assets. HTM assets are not marked to market: Banks can look on nonchalantly as bonds lose value; they remain glued to balance sheets at amortised cost regardless. By contrast, AFS assets are marked-to-market—a purer designation but one that injects an element of volatility into a bank’s capital base. For smaller banks, regulators look through this volatility but for banks with over $700 billion in assets, that volatility directly impacts regulatory capital.

Initially, banks favoured the flexibility that AFS gave them. If conditions changed and they wanted to sell, they could do so without much fuss. Sell even a single bond out of an HTM portfolio, however, and the entire portfolio would need to be re-marked accordingly. Through 2020, around three quarters of banks’ securities portfolios were held as AFS.

But then interest rate expectations started to shift and bond prices began to slide. Having been sitting on mark-to-market gains on their securities portfolios, banks started to see losses emerge. Unrealised gains of $39 billion across banks’ AFS portfolios at the end of 2020 swung to unrealised losses of $31 billion by the end of 2021.

To staunch the bleed, many banks reclassified AFS securities as HTM. This meant recognising losses upfront, but the switch would protect balance sheets from further losses as bond prices continued to fall. The largest bank, JPMorgan transferred $342 billion of securities from AFS to HTM, taking its weighting of AFS down to 30%. Others followed suit: Across the industry, the weighting of banks’ securities held as AFS shrank from three-quarters to just over half by the end of 2022.

But rising rates didn’t just present cosmetic challenges around how banks classify their bond holdings; they also gave rise to more fundamental challenges around how to manage the portfolio. Although bank treasury executives witnessed a brief tightening cycle in 2017/18, they had never had to contend with as sharp a rates move as occurred in 2022.

Different banks adopted different strategies. JPMorgan retained a lot of cash and chose to manage its AFS book aggressively. “We sell rich securities and buy cheap,” said CEO Jamie Dimon on his third quarter earnings call. Fifth Third decided to wait before deploying its excess deposits in securities. “We can afford to be patient,” its CFO said on an earnings call in January 2021. Fifth Third arguably made its move too early in 2022 but nevertheless was able to lock in slightly better yields than banks that had bought into the market sooner.

Some banks got it completely wrong. First Republic is one we discussed in October. Another, now apparent, is Silicon Valley Bank.

Silicon Valley Bank was set up in 1983 to service the burgeoning tech ecosystem taking root in the Valley. Revised regulations eased the process for acquiring a bank licence, and Silicon Valley Bank became one of 72 new banks launched in California that year. It grew slowly, surviving a real estate wobble that led to a big write off in 1992, before confronting the tech boom and bust several years later.

Silicon Valley Bank offers tech companies a range of products: deposit services, loans, investment products, cash management, commercial finance and more. Because younger companies tend to have more cash on hand than debt, most of the bank’s money is traditionally made on the deposit side of the business.

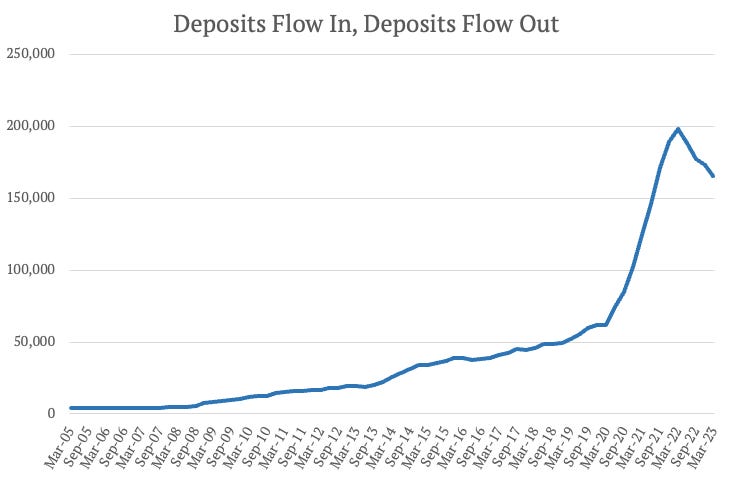

Driven by the boom in venture capital funding, many of Silicon Valley’s customers became flush with cash over 2020 and 2021. Between the end of 2019 and the first quarter of 2022, the bank’s deposit balances more than tripled to $198 billion (including a small acquisition of Boston Private Financial Holdings). This compares with industry deposit growth of “only” 37% over the period. Around two-thirds of the deposits were non-interest-bearing demand deposits and the rest offered a small rate of interest. All-in, at the end of 2022, the cost of Silicon Valley’s deposits was 1.17% (up from 0.04% at the end of 2021).

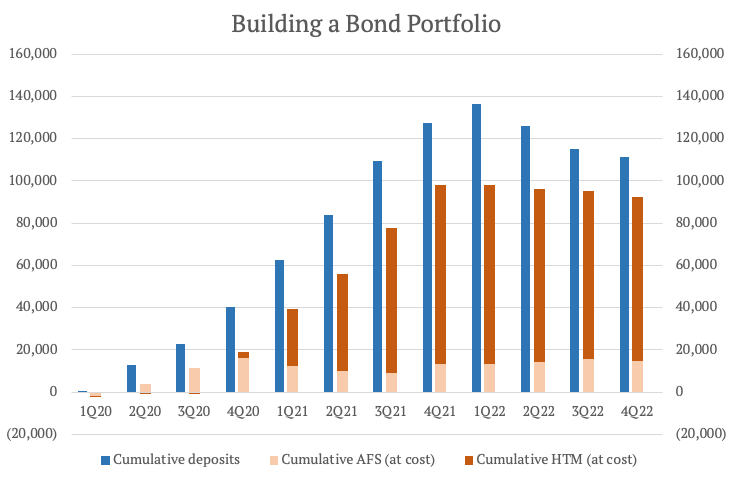

The bank invested the bulk of these deposits in securities. It adopted a two-pronged strategy: to shelter some of its liquidity in shorter duration available-for-sale securities, while reaching for yield with a longer duration held-to-maturity book. On a cost basis, the shorter duration AFS book grew from $13.9 billion at the end of 2019 to $27.3 billion at its peak in the first quarter of 2022; the longer duration HTM book grew by much more: from $13.8 billion to $98.7 billion. Part of the increase reflects a transfer of $8.8 billion of securities from AFS to HTM, but most reflected market purchases.

“Based on the current environment, we’d probably be putting money to work in the 1.65%, 1.75% range,” said the bank’s CFO at the beginning of 2022, referring to the yields he wanted to achieve. “The vast majority of that…being agency mortgage backed, mortgage collateral, things along those lines.”

The trouble is that when rates started to go up, mortgage assets got hit hard. The duration of Silicon Valley’s HTM portfolio extended to 6.2 years, as at the end of 2022, and unrealised losses snowballed, from nothing in June 2021, to $16 billion by September 2022. That’s a 17% mark-to-market hit. The smaller AFS book was also impacted, but not as badly. Mark-to-market losses there amounted to 9% by the end of September.

So big was this drawdown that on a marked-to-market basis, Silicon Valley Bank was technically insolvent at the end of September. Its $15.9 billion of HTM mark-to-market losses completely subsumed the $11.8 billion of tangible common equity that supported the bank’s balance sheet.

Remember, though, that these losses don’t have to be recorded on the bank’s books and so Silicon Valley’s CEO could take his bike for a spin without a care. Although not great for its margin – much higher yields were now available in the market than the 1.65%, 1.75% the bank had chased – the situation wasn’t fatal. “The good news is that the securities portfolio is constantly paying down. And so we’re roughly seeing about $3 billion a quarter,” said the group’s CFO on his third quarter earnings call. It would take a long time, but the losses were expected to unwind as the bonds redeemed.

What neither the CEO nor the CFO anticipated, however, was that deposits might run off faster. Which is odd, because they’d seen deposits run off before. In the aftermath of the dotcom crash 20 years ago, deposits at the bank fell from $4.5 billion to $3.4 billion by the end of 2001 as customers drew down on their cash reserves.

The Chief Risk Officer may have spotted some clouds, but she didn’t hang around to find out. She left her role in April 2022 (after selling some stock in December) and wasn’t replaced until January 2023.

This time around, deposits fell from $198 billion at the end of March 2022 to $173 billion at the end of December (and $165 billion by the end of February 2023). Part of the decline reflects a system-wide contraction. Prior to 2022, there had only been 10 quarters of deposit outflows in the US in the past fifty years; we’ve now seen four quarters of outflows. But the factors that led to Silicon Valley Bank gaining deposit share on the way up are instrumental in it losing share on the way down.

In order to reposition its balance sheet to accommodate the outflows and increase flexibility, Silicon Valley this week sold $21 billion of available-for-sale securities to raise cash. Because the loss ($1.8 billion after tax) would be sucked into its regulatory capital position, the bank needed to raise capital alongside the restructuring.

Unfortunately, the capital raise never got done. The bank chose to announce its balance sheet restructuring the same day that Silvergate Capital announced it is going into voluntary liquidation. We spoke about Silvergate here last week. The business models are quite different, but the treasury challenges are not. Both banks struggled to contain bond losses at a time they were losing deposits. Customer fear turned Silicon Valley Bank’s trickle of deposit outflows into a flood.

We’ve never really had a bank run in the digital age. Northern Rock in the UK in 2007 predated mobile banking; it is remembered via images of depositors lining up (patiently) outside its suburban branches. In 2019, a false rumour on WhatsApp started a small run on Metro Bank, also in the UK, but it was localised and quickly resolved. Credit Suisse lost 37% of its deposits in a single quarter at the end of last year as concerns mounted about its financial position although, at least internationally, high net worth withdrawals would have had to have been phoned in rather than executed via an app.

The issue, of course, is that it is quicker and more efficient to process a withdrawal online than via a branch. And although the image of a run may be different, it is no less visible. Yesterday, Twitter was alight with stories of venture capital firms instructing portfolio companies to move their funds out of Silicon Valley Bank. People posted screenshots of Silicon Valley Bank’s website struggling to keep up with user demand. Greg Becker, the bank’s CEO, was forced to hold a call with top venture capitalists. “I would ask everyone to stay calm and to support us just like we supported you during the challenging times,” he said.

[Edit: According to an order filed by California’s bank regulator, the Department of Financial Protection and Innovation, customers initiated withdrawals of $42 billion in deposits from the bank on March 9, 2023, equivalent to a quarter of its overall deposit base.]

The problem at Silicon Valley Bank is compounded by its relatively concentrated customer base. In its niche, its customers all know each other. And Silicon Valley Bank doesn’t have that many of them. As at the end of 2022, it had 37,466 deposit customers, each holding in excess of $250,000 per account. Great for referrals when business is booming, such concentration can magnify a feedback loop when conditions reverse.

The $250,000 threshold is in fact highly relevant. It represents the limit for deposit insurance. In aggregate those customers with balances greater than this account for $157 billion of Silicon Valley Bank’s deposit base, holding an average of $4.2 million on account each. The bank does have another 106,420 customers whose accounts are fully insured but they only control $4.8 billion of deposits. Compared with more consumer-oriented banks, Silicon Valley’s deposit base skews very heavily towards uninsured deposits. Out of its total $173 billion deposits at end 2022, $152 billion are uninsured.

So how could the bank have satisfied customers’ deposit demands?

One thing it couldn’t do is tap into its held-to-maturity securities portfolio. The sale of a single bond would trigger the whole portfolio being market to market which the bank didn’t have the capital to absorb.

It could have enticed depositors back with higher rates (as Credit Suisse has tried to do). In particular, Silicon Valley Bank oversees $161 billion of off-balance sheet client funds (as at end February) which it could have seduced back onto its balance sheet. But the bank already offers 1.17% on deposits which is almost twice the 0.65% median of large US peers. And… well… over $250,000 and you’re not insured.

It could have borrowed the funds. Last year, Silicon Valley Bank tapped the Federal Home Loan Bank of San Francisco for $15 billion and it had capacity to borrow more. We discussed the Federal Home Loan Bank of San Francisco here last week in the context of Silvergate. They’re the ones who pulled their funding lines to Silvergate, tipping it into liquidation. At year end, Silicon Valley Bank was already their biggest borrower, accounting for 17% of advances. To lock in that borrowing, Silicon Valley Bank had to pledge $19 billion of assets. The problem is that it doesn’t come cheap. The bank paid 4.17% on its total short-term borrowings at the end of 2022, of which Federal Home Loan Bank funding is the largest slice. Against a yield of 1.79% on the HTM securities portfolio, it’s not a particularly attractive enterprise.

All of this is now moot. Its crisis meant that the capital raise to cover AFS portfolio losses was pulled, leaving Silicon Valley Bank undercapitalised. Earlier today, the bank was closed by the California Department of Financial Protection and Innovation (who have had a busy week, what with Silvergate as well) which cited inadequate liquidity and insolvency. [Edit: the California DFPI disclosed that as of the close of business on March 9, Silicon Valley Bank had a negative cash balance of approximately $958 million and that despite attempts to transfer collateral from various sources, it didn’t meet its “cash letter” with the Federal Reserve.]

The Federal Deposit Insurance Corporation (FDIC) was appointed as receiver. All insured deposits have been transferred to a newly created bank, the Deposit Insurance National Bank of Santa Clara (DINB). Uninsured depositors meanwhile are left hanging. They will receive an “advance dividend” next week, with future dividend payments contingent on FDIC selling Silicon Valley Bank assets.

Fortunately, Silicon Valley Bank’s resolution plan is still fresh. The bank became large enough in 2021 that regulators required it to draw up a “living will” on a three-yearly cycle. Silicon Valley Bank submitted its first one in December.

For the industry overall, the episode is likely to cast a long shadow. It’s been 868 days since a bank last failed in the US, close to the longest stretch on record. In the meantime, consumers have become inured to the risk, evidenced by the growth of uninsured deposits, including in digital wallets.

One of the features of banking crises is that they rarely repeat consecutively. This matters because policymakers have a tendency to craft regulation around the last war. US stress tests include all manner of scenarios for bad credit, but few for interest rate shocks. The severely adverse scenario for 10 years Treasury yields is 0.8-1.5%; the baseline scenario, reflecting a shallower recession, incorporates yields of 3.2-3.9%.

In Europe, interest rate risk is overseen by regulators through the Liquidity Coverage Ratio (LCR). It requires banks to hold enough high-quality liquid assets (HQLA) – such as short-term government debt – that can be sold to fund banks during a 30-day stress scenario designed by regulators. Banks are required to hold HQLA equivalent to at least 100% of projected cash outflows during the stress scenario.

Credit Suisse withstood its surge in deposit outflows with an average LCR of 144% (albeit down from 192% at the end of the third quarter). Silicon Valley Bank was never subjected to the Federal Reserve’s LCR requirement – even as the 16th largest bank in America, it was deemed too small. It’s a shame. Regulation is not a panacea since banks are paid to take risk. But a regulatory framework to suit the risks of the day seems appropriate and it’s one US policymakers may now be scrambling for.

Those insurance premiums are paid indirectly by savers in the form of lower yield on their savings.

And who will pay that special fee mr. grey_whiskers? It will be savers in the form of lower yield on sacings and people wo get loans from banks in the form of higher interest rates. Savers & borrowers are tax payers

There is no free lunch. Tax payers always pay what government spends. There is no other source of money for gov't. The FUGLY big national debt is a burden on future tax payers.

Not everyone uses commercial banks.

Some people use credit unions, which have their own setup: and won’t be bailing out banks.

Come on man...(quoting Biden)

Credit Unions do not operate in a vacuum.

They compete with banks.

What affects banks will affect Credit unions.

You really are a troll.

Black in 2008 when the FDIC was closing several banks they ran low in their funds and to replenish they forced the banks to prepay 3 years worth of premiums to refill the fund.

All banks pay roughly the same premium formula. Instead of assessing risk like regular insurance companies do, those at risk pay more, they don’t do that. It’s a pretty screwed up way they do things.

Not from the taxpayers.

It is always tax payers receiving reduced dividends to pay FDIC insurance.

That's awful. You can avoid that by not owning any bank stocks.

You should be aware that any dividend or interest paying entity does NOT operate in vacuum. They all compete for depositors and borrowers. In other words yield is competitively priced everywhere. If some non-bank is paying out higher yield but is not insured for $250,000 then people will prefer bank for reducing risk.

In summary, every tax payer pays directly or indirectly for FDIC.

You can not escape taxes or death.

Come on man...stop repeating the same phrase when you can’t refute my point of view. Very low IQ behavior on your part.

All you have to do to avoid it is don’t own bank stock and don’t have an interest-bearing account in a bank.

It must suck to be so old and feeble.

Here’s a hint.

Get over yourself.

Nobody cares about your treadmill workout, and just because you express an opinion, doesn’t obligate everyone to fall at your feet and worship just because you deigned to speak.

FDIC is for banks, National Credit Union Share Insurance Fund is for Credit Unions.

You still breathing?

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.