Posted on 06/10/2021 4:56:56 AM PDT by blam

Yields on 10-year Treasuries dipped below 1.50% today for the first time since early March amid a furious short squeeze discussed earlier…

… and as post-pandemic inflation concerns appear to be waning as quickly as they flared up.

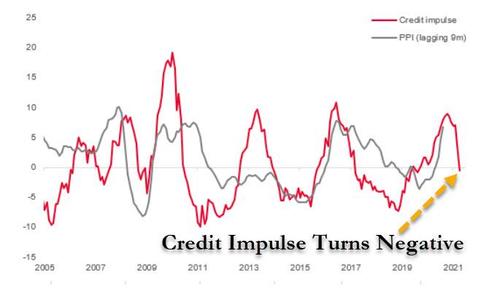

This is a point we first brought up last month when observing the collapse in China’s credit impulse, arguably the most important variable for the entire global reflationary narrative (see “China’s Credit Impulse Just Turned Negative, Unleashing Global Deflationary Shockwave“)…

… and it’s a point that Goldman’s chief economist Jan Hatzius reiterated in a note published on Tuesday titled simply “Why the Economy Won’t Overheat,” in which he argues – the same as the Fed – that the inflation we are seeing so far is likely to be temporary and prices will normalize again as we leg further away from unprecedented pandemic activity curtailments.

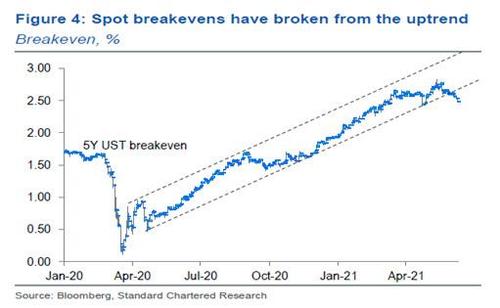

While we disagree – and so does Deutsche Bank, which sees nothing short of Weimar hyperinflation being unleashed by the Fed soon, something we first predicted in March 2009 as the ultimate endgame – it is interesting that today, at least, markets appear to be adopting this view judging by the collapse in 10Y nominal rates and the recent breach of the upward trendline in breakevens…

… this even as China’s PPI printed at a Lehman Sept 2008 high of 9.0% overnight.

So what, according to Goldman is the reason for receding inflation fears? As Hatzius and strategist Chris Hussey explain, the past 2 payrolls reports have been underwhelming as the rush back to work “is being slowed by generous stimulus as well as an inability — perhaps — to simply process so many new workers. On the one hand, fewer available workers should push up wages as companies compete to attract new workers. But a more orderly stream of employment in the post-pandemic recovery may also allow for a more extended reopening period and perhaps a bit less top-line pressure on prices.”

Another reason for receding inflation fears may also simply be time. According to Goldman, as Americans become more accustomed to getting back to their daily routines, the strangeness of such activity recedes. And it is perhaps easier for investors to envision what‘normal’ will look like. And perhaps that vision is collectively coalescing around a‘new normal’ that looks surprisingly similiar to the pre-pandemic ‘old normal’.

Hatzius then elaborates why the recent inflation pickup will remain transitory: “On the wage side, labor supply should increase dramatically over the next 3-6 months as fear of the virus diminishes further and the $300/week benefit top-up expires—over the next few weeks in most Republican-controlled states and on September 6 in the remaining states.”

In other words, employers will likely hold out another 3 months until the end of emergency benefits expire at which point they expect a flood of workers to reverse the calculus in the labor market, from one of no labor supply to a flood of supply.

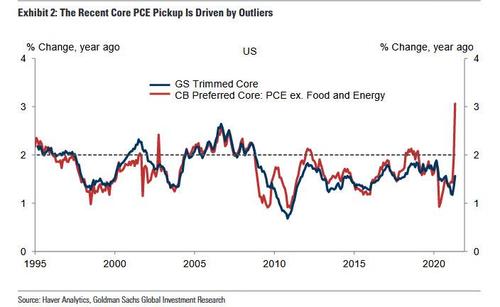

On the price side, Goldman’s trimmed core PCE—which excludes the 30% most extreme month-to-month price changes, and as a reminder the surge in inflation last month was largely driven by soaring used car prices and transportation services, or as Goldman puts it “outliers” — remains at just 1.56% year-on-year, half the standard core PCE rate. This gap illustrates the unprecedented role of outliers in the recent inflation pickup.

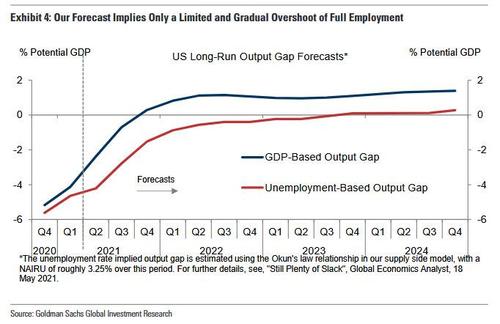

Ultimately, to Goldman, the biggest question in the overheating debate remains whether US output and employment will rise sharply above potential in the next few years. If the answer is yes, then inflation could indeed climb to undesirable levels on a more permanent basis. Predictably, Goldman’s answer continues to be no, and here’s why: “Even though real GDP is nearly back to the pre-pandemic level, we still see significant slack in the economy based on the remaining jobs shortfall of nearly 8 million and the pandemic-driven productivity gain of 4.1% year-on-year in Q1. Moreover, we think sequential GDP growth has probably already peaked in monthly terms and will trend down from here as the fiscal impulse wanes, modestly at first and then more sharply in late 2021 and 2022.”

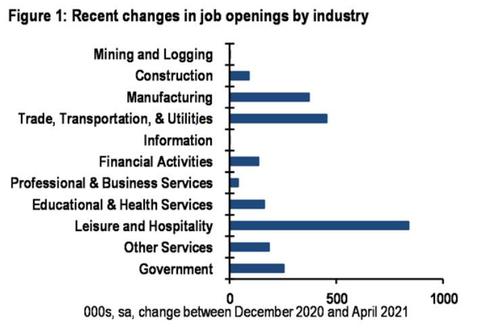

Here JPMorgan also chimes in and in a recent note from economist Dan Silver writes that as we prepare for the CPI print, it is worthwhile to consider the impacts of the removal of federal unemployment benefits and increasing hourly wages. In Silver’s note, he illustrates the growth in job openings among low-income jobs.

JPM then asks the right question: “will wage increases remain durable if business owners know that supply is coming back online?” A question we have asked previously, and the answer is a decisive not. To JPM, if the answer is indeed no, “we see a quicker than expected deceleration in wage growth, spending, and CPI.” Although, alternatively, it seems more likely that we will also see a surge in jobs taken and potentially another leg higher in absolute macro data.

With that in mind, what’s next on the inflation catalyst front and what will tomorrow’s critical CPI print show? Here, Goldman estimates a 0.50% increase in May core CPI (in line with consensus), which will boost the year-on-year rate by six tenths to 3.55%, up from 3.0% which however is largely impacted by the base effect collapse of last year. Goldman’s monthly core inflation forecast “reflects reopening-driven strength in airfares, hotel prices, and recreation prices.” Additionally, Goldman expects strong monthly readings in used cars (+6%) and new cars (+0.5%), reflecting “one-time” supply chain disruptions and microchip shortages.

And while the Fed is more concerned with PCE inflation rather than CPI, Goldman concludes that even though the inflation burst is transitory, “it will be interesting to see how markets react to a 3.5%+ inflation report in a monetary regime that presumably is focused on keeping inflation around 2%.”

Goldman will be protected in the crash as they will play a major part of the “Great Reset” that is coming.

GS talks their own book hoping others follow.

Got to separate the muppets from their money.

1. Low population growth.

2. Negative productivity growth.

3. Massive debt at all levels -- personal, corporate and government.

In a nutshell ... Demand for many things is going to be constrained simply because people won't have the money to buy them even at 2015 prices.

PCE inflation stands for personal consumption expenditures.

It’s different from the older consumer price index (CPI inflation) in that if CPI goes too high people will buy lower priced alternatives (Chinese goods).

Chase is saying that folks adapt to the dollar weakening, caused by democrat policies (which would rather you rely on government) to provide for your needs.

This inflation wouldn’t have anything to do with our $28 trillion deficit, would it? Printing money like mad to escape debt is a time-honored tradition of governments run by weasels.

Redundant

Overheat? You can have hyperinflation in a dead economy like Zimbabwe’s just so long as the government can afford paper, ink and a lot of extra zeros. And with digital money we done need the paper or ink and the zeros are free.

done->don’t. I hate ottokorrekt.

I'm skeptical. Not a word in there about the Biden-Harris-Pelosi-Schumer deliberate success at raising energy prices - that are deliberately intended to spike energy usage in their “Green New Deal”, plus a few trillion more in their perpetual-efforts to raise the national minimum wages and their perpetual effort to increase subsidies and increase the number of people on welfare (er, Basic Subsistence Allowance)

Lots of words in arcane minor indexes though!

Goldman is using stale data gathered months ago. They are also forecasting the labor market using guesses and not current supply and demand numbers that are unlikely to change.

While UI payments will run out, never underestimate the stupidity of government to extend other types of payments.

Also, Goldman fails to understand the labor market has radically changed where the younger generations do not want to work full time and all year. They want a gig job to make money then travel or do something else. Goldman also fails to understand that people have now learned to do without, so getting more is not in their personal agenda.

As far as inflation, it is here. Used cars prices are forecasted by industry experts to climb 50% in the next three months. New care dealers now have only 1-4% of their normal inventory due to supply issues. The farming and ranching shortages are real and will hit consumers later this summer. Goldman seems to discount that as a problem that somehow by childish magic will work itself out.

This whole bunch of crap is to inflate our way out of debt.....................

“Goldman will be protected in the crash as they will play a major part of the “Great Reset” that is coming.”

Explain what this “great reset” is and what part Goldman will play.

“Goldman will be protected in the crash as they will play a major part of the “Great Reset” that is coming.”

Explain what this “great reset” is and what part Goldman will play.

Big fat liars.

The Demagogic Party has all "systemically racist" business under attack. E.G. the residential construction business is being sent into a bust cycle in part thanks to lumber prices.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.