Skip to comments.

Stock Rally Adds Another Percent while Metals Fade: Week Ahead Worries-- Investor Thread Feb. 22

Weekly investment & finance thread ^

| February 22, 2015

| Freeper Investors

Posted on 02/22/2015 8:34:45 AM PST by expat_panama

|

Next week will be a busy week on Wall Street with a raft of big earnings reports including Target (TGT), Macy’s (M), Home Depot (HD) and Hewlett-Packard (HPQ) to name just a few. Investors will also have a lot of economic data and geopolitics to digest this coming week and in the weeks that follow. The Commerce Department will release the latest reading on third quarter Gross Domestic Product. Yahoo Finance’s Rick Newman thinks investors will be watching that report closely, as well as the situation in Greece. Newman predicts Greece will finally cave in its standoff with its European underwriters over the terms of its debt deal. “I think next week is going to be the week that Greece blinks,” says Newman. He believes Greek officials will “finally say ‘OK, we have to go along with the bailout terms.’” And Newman believes that will lead to a pop in European stocks. Yahoo Finance’s Aaron Task is looking to our nation’s capital and a couple of looming deadlines as the next potential trouble spots that could rankle financial markets. Funding for the Department of Homeland Security will run out at the end of February unless Congress can come to an agreement to extend funding. Task believes this is just the first in a series of contentious debates... [snip] ...The Treasury secretary can use a number of gimmicks to postpone the day of reckoning, and experts think such gimmicks can carry us through September or October. Then we’ll witness a serious confrontation of the sort we’ve seen before—a game of fiscal chicken between Congress and the White House. If Blinder is right and the United States does breach the debt ceiling, Task believes that will set off “all kinds of fireworks in the financial markets.”

The recent drop in oil prices has created a situation that is very complex for investors. Oil has become cheap again and the stocks tracking the oil and gas sector have tanked to the point that at least ... |

|

Females typically save 8.3% of their income, while men only save 7.9%, Fidelity found after looking at over 12 million retirement accounts and adjusting for certain pay disparities between men and women. That may not sound like a big difference, but it adds up over time. Consider that the median household income in the U.S. is around $50,000. If you apply those savings rates to the median income, women save about $200 more a year. So if their returns are about the same, women would end up with more. ..[snip]  After tight trading, volatility set to return to stocks After tight trading, volatility set to return to stocks

By Chuck Mikolajczak NEW YORK (Reuters) - After a holiday-shortened trading week that pinned stocks in a tight trading range, equities are poised for a bout of renewed volatility as investors watch the economy and the Federal Reserve for signs of policy changes and economic strength. Through Thursday's close, the S&P 500 was held to its narrowest trading week since Thanksgiving as investors dealt with uncertainty regarding a forward path for the economy and a deal for Greek debt. Late on Friday, the European Union agreed to a four-month extension for Greece, and a late rally pushed the S&P 500 above technical resistance level of 2,100 after several failed attempts earlier in the week. The index was up modestly for the week, building on a 5-percent gain over the prior two weeks. "The market has done quite well this week holding things together," said Frank Cappelleri, technical market analyst and trader at ...

|

--and not only has all this been written by experts, but everything here's been posted on the internet so we can to believe every single word. * * * * * * * * * * * * * *

|

TOPICS: Business/Economy; Government; News/Current Events

KEYWORDS: economy; financial; stockmarket; wallstreet

Navigation: use the links below to view more comments.

first previous 1-20, 21-40, 41-60, 61-80, 81-93 next last

To: Wyatt's Torch

Whoa... Puts new insight into what ‘dot.com’ really means. Facebook was an IPO just a minute ago, number one trillion dollar Apple wasn’t even on the list back in 2K.

tx!

To: expat_panama

I hate PP. That said I do an incredible amount of business with vendors that only use PP and have never had one problem transaction.

To: mad_as_he$$

...never had one problem transaction...They say we can't argue w/ success, though that's were most folks like to spend their time. My experience w/ PP was the excessive surprise hidden fees along with the inconvenience. The main thing that keeps me from using PP now is the fact that there are so many easier methods of paying online. If that changes then I suppose I'll become a regular happy PP customer.

To: expat_panama

24

posted on

02/23/2015 11:01:08 AM PST

by

Lurkina.n.Learnin

(It's a shame nobama truly doesn't care about any of this. Our country, our future, he doesn't care)

To: Lurkina.n.Learnin

tx! maybe I can use LoopPay w/ my andy emulator...

To: expat_panama

That said Loop Pay still uses your CC number. I don’t think much of that.

26

posted on

02/23/2015 11:37:39 AM PST

by

Lurkina.n.Learnin

(It's a shame nobama truly doesn't care about any of this. Our country, our future, he doesn't care)

To: abb; expat_panama

Why we need currency competition. Let everybody print currency. The market will quickly sort out the inflationists.

27

posted on

02/23/2015 8:07:19 PM PST

by

1010RD

(First, Do No Harm)

To: 1010RD

You have described the most simple of transactions, barter. The problem is getting the folks on the other side of the trade to accept your currency.

For something to meet the description of “money,” it must meet several tests: A medium of exchange, a common measure of value (or unit of account), a standard of value (or standard of deferred payment), and a store of value.

http://en.wikipedia.org/wiki/Money

28

posted on

02/24/2015 1:42:54 AM PST

by

abb

("News reporting is too important to be left to the journalists." Walter Abbott (1950 -))

To: abb

A medium of exchange, a common measure of value (or unit of account), a standard of value (or standard of deferred payment), and a store of value.All of which are experiential. US government greenbacks are simply barter if you look at it as a promise to pay. Money competition removes the power to manipulate the economy via interest rate and reserve requirements, etc.

Money is fungible.

29

posted on

02/24/2015 4:28:20 AM PST

by

1010RD

(First, Do No Harm)

To: 1010RD

Yes it is. But it still must be accepted. Notice how during the “bitcoin” craze, the value was still measured in dollars.

And watch all the ads for gold on TV. They can’t wait to sell it to YOU and convert it into something that will spend, namely dollars.

30

posted on

02/24/2015 4:36:55 AM PST

by

abb

("News reporting is too important to be left to the journalists." Walter Abbott (1950 -))

To: 1010RD; A Cyrenian; abb; Abigail Adams; abigail2; AK_47_7.62x39; Aliska; aposiopetic; Aquamarine; ..

There are no words that can describe today's markets, but that never slows me down.

Yesterday's upside reversal saw the NASDAQ rise for the 9th day in a row. It's something that's happened as many times since Mar. '09. "Half the time, the streaks ended with the market pulling back or turning choppy. The other half of the time, there have been declines of 5% to 19%." [from IBD] Futures traders right now see stock indexes up +0.04%; they also got metals -0.09% after yesterday's sideways trends. Later this AM we get reports from Case-Shiller 20-city Index and Consumer Confidence. News links:

Another big heads-up from IBD is "Tax System Gives Edge To Foreign Buys Of U.S. Firms" Bottom line is Canadian VRX shot up 14% after buying North Carolinan SLXP which tanked. While others can argue whether Obama hates America, the rest of us have understand that feeding our families means investing outside the U.S -and I'll cry for the U.S. all the way to the bank.

Related FR Econ thread: As free trade pacts expand, U.S. trade deficit soars. Why add one more?

To: expat_panama

There are no words that can describe today's markets, but that never slows me down. I hear Fox Business and CNBC are looking for new talent... Maybe we all should apply, LOL!

32

posted on

02/24/2015 5:14:13 AM PST

by

abb

("News reporting is too important to be left to the journalists." Walter Abbott (1950 -))

To: 1010RD

...we need currency competition. Let everybody print currency...

...we need currency competition. Let everybody print currency...We already tried that:

For America’s first 70 years, private entities, and not the federal government, issued paper money. Notes printed by state-chartered banks, which could be exchanged for gold and silver, were the most common form of paper currency in circulation. From the founding of the United States to the passage of the National Banking Act, some 8,000 different entities issued currency, which created an unwieldy money supply and facilitated rampant counterfeiting. By establishing a single national currency, the National Banking Act eliminated the overwhelming variety of paper money circulating throughout the country and created a system of banks chartered by the federal government rather than by the states. The law also assisted the federal government in financing the Civil War.

To: 1010RD

Money competition removes the power to manipulate the economy via interest rate and reserve requirements, etc. Competition between Euro, Dollar and Yen hasn't removed that power, why would competition between banks or other domestic issuers?

34

posted on

02/24/2015 5:34:38 AM PST

by

Toddsterpatriot

(Science is hard. Harder if you're stupid.)

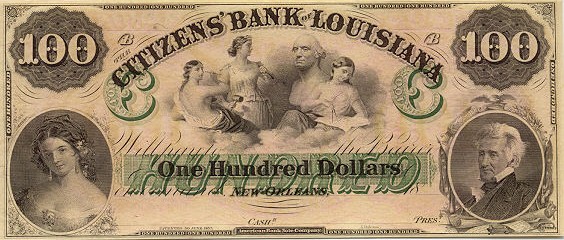

To: expat_panama; 1010RD

Some history of that bank and its “money.”

http://www.waymarking.com/waymarks/WM99BQ_The_Birthplace_of_Dixie_New_Orleans_LA

The Birthplace of “Dixie”

On this site from 1835 to 1924 stood the Citizens State Bank, originator of the “Dixie.” In its early days, the bank issued its own $10 bank note, with the French word “Dix” for “ten” printed on the note’s face. As this currency became widespread, people referred to its place of origin as “the land of the Dix,” which eventually shortened to “Dixieland.” Through song and legend, the word became synonymous with America’s southland.”

My favorite “money” story.

http://en.wikipedia.org/wiki/Magnetic_ink_character_recognition

Before the mid-1940s, cheques were processed manually using the Sort-A-Matic or Top Tab Key method. The processing and clearance of cheques was very time consuming and was a significant cost in cheque clearance and bank operations. As the number of cheques increased, ways were sought for automating the process. Standards were developed to ensure uniformity in financial institutions. By the mid-1950s, the Stanford Research Institute and General Electric Computer Laboratory had developed the first automated system to process cheques using MICR.[4] The same team also developed the E13B MICR font. “E” refers to the font being the fifth considered, and “B” to the fact that it was the second version. The “13” refers to the 0.013 inch character grid.[5]

In 1958, the American Bankers Association (ABA) adopted E13B font as the MICR standard for negotiable documents in the United States. By the end of 1959, the first cheques had been printed using MICR. The ABA adopted MICR as its standard because machines could read MICR accurately, and MICR could be printed using existing technology. In addition, MICR remained machine readable, even through overstamping, marking, mutilation and more.

35

posted on

02/24/2015 5:48:05 AM PST

by

abb

("News reporting is too important to be left to the journalists." Walter Abbott (1950 -))

To: expat_panama; 1010RD

Now we get into the history of banking and lending, which demands that we look at this bit of history. Note the most important component of said history: Trust.

http://en.wikipedia.org/wiki/History_of_the_Knights_Templar#Bankers

By 1150, the Order’s original mission of guarding pilgrims had changed into a mission of guarding their valuables through an innovative way of issuing letters of credit, an early precursor of modern banking. Pilgrims would visit a Templar house in their home country, depositing their deeds and valuables. The Templars would then give them a letter which would describe their holdings. Modern scholars have stated that the letters were encrypted with a cipher alphabet based on a Maltese Cross; however there is some disagreement on this, and it is possible that the code system was introduced later, and not something used by the medieval Templars themselves.[6][7][8] While traveling, the pilgrims could present the letter to other Templars along the way, to “withdraw” funds from their accounts. This kept the pilgrims safe since they were not carrying valuables, and further increased the power of the Templars.

Knights Templar playing chess, 1283.

The Knights’ involvement in banking grew over time into a new basis for money, as Templars became increasingly involved in banking activities. One indication of their powerful political connections is that the Templars’ involvement in usury did not lead to more controversy within the Order and the church at large. Officially the idea of lending money in return for interest was forbidden by the church, but the Order sidestepped this with clever loopholes, such as a stipulation that the Templars retained the rights to the production of mortgaged property. Or as one Templar researcher put it, “Since they weren’t allowed to charge interest, they charged rent instead.”[9]

36

posted on

02/24/2015 5:57:44 AM PST

by

abb

("News reporting is too important to be left to the journalists." Walter Abbott (1950 -))

To: Toddsterpatriot

What backs the Euro, Dollar, Yen, et al? Do we believe in free markets or not?

37

posted on

02/24/2015 5:58:15 AM PST

by

1010RD

(First, Do No Harm)

To: 1010RD; Toddsterpatriot; All

What backs any “money,” or currency, or economic system is “work.” That is productive human activity and/or creativity.

Which is why so many European economies are in the toilet. Save Germany, Europeans are not acquainted with the concept of “work.” Greece, especially so, and it is reflected in their economy.

And which is why we here in the USA still rule the world when it comes to economic activity.

Most of us still know how to work.

38

posted on

02/24/2015 6:05:48 AM PST

by

abb

("News reporting is too important to be left to the journalists." Walter Abbott (1950 -))

To: 1010RD

What backs the Euro, Dollar, Yen, et al?Well, you could say the Dollar is backed by $4.5 trillion in Fed holdings.

Do we believe in free markets or not?

Sure. What does that have to do with competing currencies eliminating interest rate and reserve requirement manipulation?

39

posted on

02/24/2015 6:09:59 AM PST

by

Toddsterpatriot

(Science is hard. Harder if you're stupid.)

To: expat_panama

unwieldy money supply and facilitated rampant counterfeitingHow are stores of value unwieldy? How are stores of value counterfeited?

Competition works. Bank clearing houses worked as well. Why not try an experiment?

40

posted on

02/24/2015 6:18:26 AM PST

by

1010RD

(First, Do No Harm)

Navigation: use the links below to view more comments.

first previous 1-20, 21-40, 41-60, 61-80, 81-93 next last

Disclaimer:

Opinions posted on Free Republic are those of the individual

posters and do not necessarily represent the opinion of Free Republic or its

management. All materials posted herein are protected by copyright law and the

exemption for fair use of copyrighted works.

FreeRepublic.com is powered by software copyright 2000-2008 John Robinson