Posted on 06/08/2015 5:13:10 AM PDT by thackney

Although data_opacity makes objective_analysis difficult, market observers reported in April that China has surpassed the United States as the world’s largest oil_importer. This statistical inflection point needs context to understand global consumption trends. While oil bulls are anxious about China’s reduced crude growth appetite, fundamental shifts in Chinese currency and domestic consumption strategies point to long-term growth in Chinese hydrocarbon consumption generally.

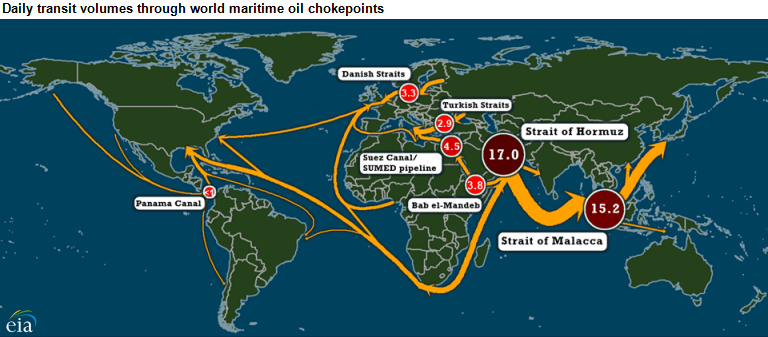

Keith Johnson wrote in Foreign Policy on May 11, 2015, “… China’s continued and, indeed, deepening reliance on volatile regions for the world for energy supplies, especially the Middle East, points to continued security vulnerabilities for Beijing for decades to come.” The recent South China Seas tensions confirm analyst observations that Beijing has strategic concerns surrounding safe hydrocarbon passage through the Malaccan Straits. China is taking advantage of lower priced crude today and ample crude tanker supply to build offshore and onshore reserves.

As China increases its reliance on crude imports from Saudi Arabia and natural gas imports from Russia, any possible political unrest in the Middle East or Eastern Europe could cause supply interruptions. Increased onshore and offshore strategic storage, as well as LNG import ability, will be needed to protect crude and natural gas flow stability...

Unlike Saudi_Arabia (which is ironically a net importer of refined product despite producing 10 million barrels of oil per day), China currently is a net exporter of petrochemicals. China’s rapidly increasing investment in downstream petrochemical refining and manufacture gives it the flexibility to export product while simultaneously meeting increasing domestic demand for both commodity and bespoke chemical products. In fact China is now is the “fastest growing petrochemical industry worldwide”. China’s push to close obsolete teapot refineries in favor of modernized, complex refineries that add more value per barrel of refined oil points to long-term need for increased feedstock imports.

(Excerpt) Read more at forbes.com ...

If you do a search for “china traffic jam” it makes complete sense that they need so much oil and gas, their cars never get off the highway once they get on.

;o)

It would seem to me that if American imports decrease because of increased domestic production, no change in China imports would still result in China becoming the largest importer.

- - - - -

China's total petroleum and other production, the fourth-largest in the world, has risen about 50% over the past two decades and serves only its domestic market. However, the production growth has not kept pace with demand growth during this period. In 2014, China produced nearly 4.6 million barrels per day (bbl/d) of petroleum and other liquids, of which 92% was crude oil and the remainder was non-refining liquids and refining gain. EIA forecasts China's oil production will increase slightly to higher than 4.6 million bbl/d by the end of 2016. In the medium and long term, EIA predicts China's oil production will grow incrementally to 5.1 million bbl/d by 2020, 5.5 million bbl/d by 2030, and 5.7 million bbl/d by 2040, based on the International Energy Outlook 2014 (IEO2014). Long-term growth will require continued success of enhancing recovery at mature crude oil fields, greater investment to access more technically challenging plays such as shale oil, tight oil, and deepwater fields, and growth in non-petroleum liquids such as gas-to-liquids, coal-to-liquids, and biofuels.

China's annual growth in oil consumption has eased after a recent high of 11% in 2010, reflecting the effects of the most recent global financial and economic downturn as well as China's policies to reduce excessive investment and capacity overbuilding. Despite the slower growth, the country still accounted for more than one-third of global oil demand growth in 2014, according to EIA estimates.

Thanks thackney.

Making China completely dependent on sea lanes we can shut down.

PWND.

At some point I expect they will demand that oil exporters accept the Yuan in payment.

That would really screw the USA

And if the exporter says "no"?

Where China imports oil from is more important than how much.

One of the justifiable reasons China has for increasing the capability of its Navy is to secure its sea lines of communication/commerce (oil supply routes).

Currently ~70% of China’s oil is imported from the Middle East. This clearly necessitates traversing the Indonesian straits (Sunda or Malacca) or circumnavigating most of the world to skirt below the Cape of Good Hope and Cape Horn.

China cannot fight any protracted war involving the US Navy under this situation for at least 15+ years. Indeed, without using its nukes, it could not currently force the Indonesian straits against a local coalition. In a war involving India, China would be forced to convoy its tankers, which would be difficult without a secure base in the Western IO.

If India becomes an anti-China belligerent (which I think China would do much to avoid), I would expect China to promise Pakistan the areas of Jammu, Kashmir, and most of Gujarat in return for a well timed attack and basing, with a large Chinese force making an attack through the Uttarakhand (Himalaya Mountains) to flank the Indian armies and put pressure on New Delhi. The strategy being to knock India out and force concessions, not take all of India. The mere threat of this would likely force Indian neutrality.

With a few more aircraft carriers, the Chinese will own the South China Sea and be able to dominate local powers, but they will still not be able to force the Indonesian straits without putting boots on the ground. I think landing a force to control the Straights of Malacca would be too difficult and costly, but an amphibious assault on both sides of the Sunda Straight wouldn’t be as difficult and would have the dual effect of putting Jakarta in peril, likely forcing Indonesia to accept Chinese terms.

If I were running the PLAN, I would be looking to establish a minimum of 8 fleet carrier strike groups, the amphibious capability to put 50,000 troops ashore, and a robust anti-submarine capability. I would also be sorting out a plan to take forward operating bases (islands) near the approaches to the Indonesian straights, should the need arise. In the IO, I’d be looking for a secure naval base near the Horn of Africa or on the Arabian Peninsula itself.

If I were the Chinese government, I’d be looking for secure supplies of oil, either domestic fracking or more pipelines from Russian and the ‘stans.

China produces ~40% of their oil themselves. Of the ~60% imported, about half of that comes from the Middle East.

You want to see the world REALLY change, just watch what happens when the US becomes a net exporter of energy in a few years. Think about what it will mean to:

... have no use for middle-Eastern tyrants,

... benefit fiscally by the price of oil going UP,

... have oil importers like Exxon-Mobil lose clout relative to oil producers like Sinclair,

... have zero economic benefit to pretending that global warming is real.

That 5.1 million barrels imported per day is down from 12.5 million barrels per day in 2005. It’s on track to drop another million in 2015 alone. Simply replacing the cars on the road, which average ten years old, with the average cars sold new today would drop it another 2 million barrels. And firing up the gas production which has been idled by lowered prices could drop it another 2 million. Then BAM!, we’re EXPORTING oil. And ours is on average very light and sweet, so at no net imports, we’re actually making a lot of money.

Can YOU see why China is very motivated to contract with Russia to build oil pipelines?

No, half that with the drop in oil prices and the corresponding drop in drilling and well completions.

U.S. crude oil production is projected to increase from an average of 8.7 million b/d in 2014 to 9.2 million b/d in 2015 and remain flat in 2016. The 2015 and 2016 production forecasts are 40,000 b/d and 100,000 b/d lower than in last month's STEO, respectively. The reduction in the crude oil production forecast reflects a reduced WTI price forecast for 2016 in this STEO and a sustained drop in rig counts beyond what EIA had initially expected. Oil-directed rigs declined to the lowest level in almost five years as of early May.

Whoops, the imports will drop even less than half a million. While the production is projected to climb half a million, the consumption is projected to grow 0.34 MMBPD, so imports will likely only fall 0.16 MMBPD.

Total U.S. liquid fuels consumption rose by an estimated 70,000 b/d (0.4%) in 2014. In 2015, total liquid fuels consumption is forecast to grow by 340,000 b/d (1.8%). EIA projects that in 2016, liquid fuels consumption growth will slow to 70,000 b/d (0.4%).

Because it worked so well for Europe’s secure and economic Natural Gas supply?

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.