Posted on 05/08/2025 6:00:17 AM PDT by Red Badger

UPDATE — May 8, 2025, 3:30 AM

This is a corrected and expanded version of an article originally published at 1:08 PM on May 7, 2025. It includes critical factual updates and new findings resulting from an ongoing investigation. I am being fully transparent about an error I made at the outset of the investigation, how that error occurred, and how correcting it led to the discovery of something even more significant..

Building a Real Estate Empire, One Undisclosed Deed at a Time

The initial confusion was driven by a seemingly impossible coincidence: Senator Thom R. Tillis has a brother—also named Thom R. Tillis. That detail, obscured in legal and corporate filings, made it appear that the Senator himself had engaged in a self-dealing real estate transaction. I originally believed the Senator had acquired 5508 Enslow Place through an LLC via $0 quitclaim deed and later sold it for profit without reporting the transaction in mandatory senate financial disclosures.

That turned out to be incorrect. But rather than invalidate the story, correcting it uncovered something even more bizarre—and far more troubling.

Senator Thomas Roland Tillis, a senior Republican from North Carolina and sitting member of powerful Senate committees on Banking, Finance, and the Judiciary, is tied to a network of real estate transactions involving his family members, an array of limited liability companies, and a nonprofit corporation registered to a luxury residential address. The result is a financial and legal ecosystem that appears to be engineered for opacity and protected by bespoke legislation and corrupt government oversight.

This report presents evidence that raises serious questions about Tillis's conduct and financial transparency with regard to:

• Verifiable property records linking Tillis family entities to concealed or underreported assets

• Multiple examples of $0 property transfers between corporate and family-controlled interests

• Omitted financial disclosures in violation of the Ethics in Government Act

• Potential misuse of nonprofit resources and commingled addresses with real estate operations

These findings are based on public records filed with the IRS, North Carolina’s Secretary of State, the Mecklenburg County Register of Deeds, and other official, government-controlled property databases. The documents cited here are verifiable and evidence of obfuscation speaks for itself.

Correcting the Initial Claim Unmasked a Bigger Problem at 5508 Enslow Place

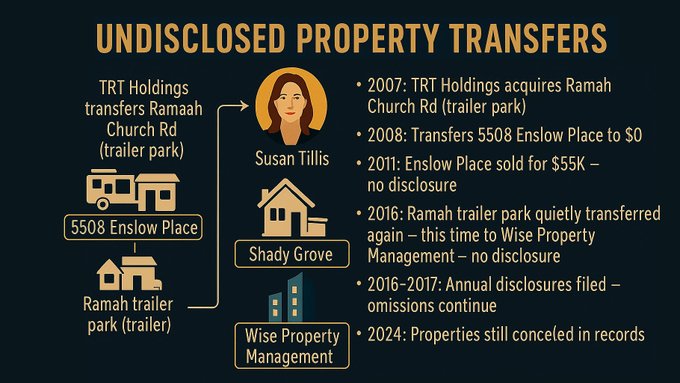

The most confounding example in this investigation remains 5508 Enslow Place. Initially, I reported that Senator Tillis personally acquired and sold this property. That claim was incorrect — in 2008, Thom “Rick” Tillis and his wife Terry quitclaimed the property to their family-controlled LLC, TRT Holdings. Five years later, in 2013, TRT Holdings sold the property via quitclaim deed to Theresa L. Baker, a woman from Connecticut who had recently relocated to North Carolina. The sale price was $55,000 — an unusually low figure considering the nature of the deed and the market value of comparable properties at the time.

That type of deed in this type of transaction is itself a red flag. Quitclaim deeds are used when the grantor offers no warranties of title, typically reserved for transfers between family members, spouses, or shell entities. They are not standard practice for retail property sales between unrelated parties. Why use one here?

Theresa Baker may not have known what a quitclaim deed was or what risks it carried. From her point of view, she was buying a modest home for a good price from a real estate company. But the seller — Thom “Rick” Tillis through TRT Holdings — chose to use a legal instrument that left her with no title protections, and that’s significant.

Baker died of cancer in 2016, just three years later. As of 2025, her name is still on the deed. The mortgage, originally taken out in her name, continued to be paid for seven years after her death, and was satisfied only recently — in 2023. No deed has been filed transferring ownership, no probate appears to have been opened, and no heirs have claimed the property.

These facts are not just strange. They point to the deliberate retention of a property in a dead woman’s name, while the home continues to be financially maintained and legally obscured. One possible explanation is that this was a planned placeholder title, allowing the true controllers of the property to remain invisible.

In April 2025, Senator Tillis co-sponsored S. 1334, a bill to raise the asset threshold for taxable Real Estate Investment Trust (REIT) subsidiaries. This legislative development sharpens the strategic picture and introduces a new layer of possible intent, opening the door for the Tillis family to roll “parked” assets — like those once held by TRT Holdings — into a REIT structure with preferential tax treatment and reduced disclosure obligations. In that light, Theresa Baker wasn’t just a buyer — she may have been an unwitting participant in a larger scheme to keep assets off Tillis’s disclosure forms and IRS visibility until they could be sanitized, bundled, and monetized.

What Makes This Legally Abnormal?

• Quitclaim deeds are rarely used in arms-length transactions between unrelated parties—yet one was used here.

• Title remained in the deceased buyer’s name for nine years—anomalous under standard probate practice.

• A mortgage remained active in her name for seven years after her death and was then quietly satisfied—without any transfer of title.

• The property was originally sold by TRT Holdings, a Tillis family-run LLC, which shared its address with a nonprofit founded by Susan Tillis.

• TRT Holdings was dissolved just five weeks before Theresa Baker’s death, raising questions about whether this was done to avoid potential entanglements with her estate.

These factors raise serious red flags. While not direct evidence of criminal conduct, the structure and timing resemble common patterns used to conceal beneficial ownership and circumvent both tax and ethics disclosure requirements.

What I Can Prove — and What I Can’t

I can prove:

TRT Holdings sold the home to Theresa Baker.

Baker died in 2016.

No deed has ever transferred the property out of her name.

The mortgage was paid off in 2023.

The address used by TRT Holdings is the same as the registered address of the Susan M. Tillis Foundation.

TRT Holdings was voluntarily dissolved shortly before Baker’s death.

I cannot prove—yet:

Who occupied or used the house after Baker died.

Who paid the mortgage from 2016 to 2023.

Whether anyone connected to the Tillis family benefited from continued use of the home.

Whether the quitclaim deed structure was used intentionally to avoid liability or prepare the property for reacquisition after Baker’s death.

Each of these unanswered questions signals a highly abnormal transaction with substantial implications. Subpoena power may be necessary to determine the true beneficiaries of the mortgage payments and posthumous occupancy.

Why Bother? The Strategic Value of a Low-Profile Asset

While 5508 Enslow Place is not a luxury property, its treatment within this network suggests it serves a strategic purpose. Low-value homes are ideal for obscured control because they attract less scrutiny from journalists, tax assessors, and regulatory agencies. If this model was used repeatedly—as records suggest TRT Holdings controlled up to 30 properties—it may reflect a scalable scheme involving:

Quiet asset control without title exposure

Use of terminal buyers to temporarily shield true ownership

Potential refinancing or leveraging of appreciated equity posthumously

Maintenance of mortgages for properties that can continue generating use, rent, or long-term title reacquisition via quiet legal means

The extended mortgage payments after Baker's death suggest a party with a long-game interest in the property. One plausible scenario is that the home was quietly re-controlled and leveraged over time while keeping it off ethics disclosures and tax rolls.

What About Susan Tillis?

The nonprofit founded by Senator Tillis’s wife, the Susan M. Tillis Foundation, was registered to the exact same luxury residential address—16116 North Point Road—as TRT Holdings, the LLC that executed these questionable real estate transactions. This overlap raises difficult questions:

Why would a nonprofit be registered to a private residence instead of commercial office space?

Why register it to the same address as a real estate LLC engaging in unorthodox transfers and dissolutions?

Was this address functioning as a command center for coordinated personal, political, nonprofit, and business activity?

These are unanswered questions. But they are also red flags. The IRS requires separation of nonprofit and for-profit activity. While sharing an address is not illegal by itself, doing so in the context of opaque real estate deals and family-controlled nonprofits is at minimum a governance issue, and at worst a concealment tactic.

Susan Tillis also appears in real estate records as the signatory on at least one deed involving another Tillis-linked property: a trailer park at 11826 Ramah Church Road. This suggests she played a direct role in facilitating real estate transfers between family-controlled entities, and further complicates any assertion that she was uninvolved.

A Curious 90 Days: Dissolution, Death, and a New Foundation

Between August and November 2016, three seemingly unrelated events occurred:

August 17, 2016 – TRT Holdings, LLC was voluntarily dissolved.

September 23, 2016 – Theresa Baker, purchaser of 5508 Enslow Place, died of cancer.

November 7, 2016 – The Susan M. Tillis Foundation was incorporated.

This 90-day period marks a critical pivot point. The entity that sold the property to a terminal buyer is shut down. The buyer dies. Then a federally tax-exempt nonprofit is launched—bearing the name of a sitting senator’s wife and sharing infrastructure with the now-defunct real estate operation.

This sequence doesn’t suggest coincidence. It suggests strategic reorganization:

Shut down the entity that carried legal and reputational risk.

Wait out the buyer’s death and preserve the deed in her name.

Launch a nonprofit that can offer cover for real estate-related expenses, activity, or new structuring efforts.

The nonprofit may have been intended to serve as a public-facing shield for a system that was previously private and exposed.

The timing strongly implies that Susan Tillis’s role was not incidental — but integrated into the broader Tillis family real estate framework.

Final Thought: Who Paid the Dead Woman’s Mortgage?

One question looms above all others:

Who was paying Theresa Baker’s mortgage for seven years after she died — and why?

That isn’t a procedural hiccup. That’s a deliberate action. Someone had access to her account or estate, continued to make regular payments on her behalf, and then paid off the loan entirely in 2023. All while keeping the deed frozen in her name.

Was it a relative? A friend? Or someone connected to the original seller — a Tillis-run LLC? I don’t know yet. But whoever it was, they had a powerful reason to keep that house legally invisible for as long as possible. And that raises perhaps the most pressing question of all:

What were they hiding?

“Shady Grove”.

Thanks for posting. Enemies domestic. CRIMINALS in CONgre$$ ALERT!

If you started peeling back ownership of real estate of House/Senate members over the age of 60...I would imagine 50-percent are engaged in some shady activities (White Water as example). Easiest way to buy for x-amount, and re-sell five years later at twice the original value, without state level noticing the scheme.

Lord of the Trailer Parks.

I did a tax return for a farmer once. It was complicated with a lot of entities. I commented on the complexity and he said he didn’t want the govt to know what he was doing. It turned out to be so complex that he didn’t know what was going on either and was filing bankruptcy a few years later.

This guy was inches away from becoming Senate Majority Leader, and he’s this corrupt. Shocking that Trump isn’t threatening to primary him like he’s doing to Rand Paul and Thomas Massie who are saints compared to Thom “the lithp” Thillis

One question looms above all others:

Who was paying Theresa Baker’s mortgage for seven years after she died — and why?

Tillis is a liar.

Open a DOJ investigation.

The State of NC might be interested as well................

“Oh, what a tangled web we weave, When first we practice to deceive.” - Sir Walter Scott, 1808

Not new wisdom by any means.

THIS^^^^

Thom Tillis is owned by SOMEONE; President Trump can change ownership in a heartbeat with DOJ attention pouring down on Tillis’ operation.

Might even be able to swing a quid pro quo out of it.

Vote right; retire, don’t run in ‘26.

This Tillis issue suddenly popped up in the news. 4-5 threads alone here at FR since yesterday.

I thought it was Rats as usual trying to bring down a conservative for the very things they themselves are guilty of. As usual.

But I’m seeing signs that Tillis is a RINO and it’s Conservatives who are out to get him.

If so... I’m cool with that.

He’s a snake in the grass as they say................

I did a tax return for a farmer once. It was complicated with a lot of entities. I commented on the complexity and he said he didn’t want the govt to know what he was doing. It turned out to be so complex that he didn’t know what was going on either and was filing bankruptcy a few years later.

xxxxxxxxxxxxxxxx

maybe the BK was part of the plan all along?

I wouldn’t mind if these crooks that are our overlords went to prison for a bit of time, too.

Final Thought: Who Paid the Dead Woman’s Mortgage?

previous thought: Who Held the Woman’s Mortgage? that got the pay off for 7 years

I also see retaliation as he’s on the Dem side of the Ed Martin issue.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.