Posted on 11/14/2019 2:09:46 PM PST by LesbianThespianGymnasticMidget

But it’s even worse than it looks. And this time, there is no jobs crisis. This time, it’s the result of greed by subprime lenders.

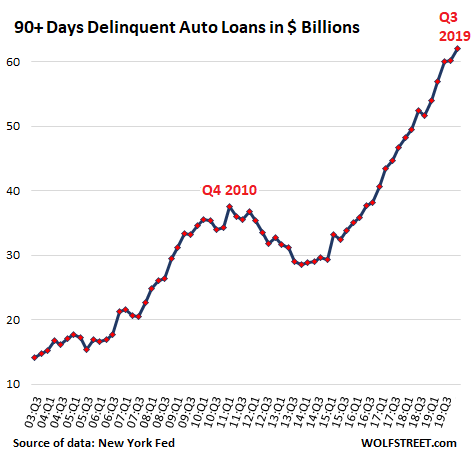

Serious auto-loan delinquencies – auto loans that are 90 days or more past due – in the third quarter of 2019, after an amazing trajectory, reached a historic high of $62 billion, according to data from the New York Fed today:

This $62 billion of seriously delinquent loan balances are what auto lenders, particularly those that specialize in subprime auto loans, such as Santander Consumer USA, Credit Acceptance Corporation, and many smaller specialized lenders are now trying to deal with. If they cannot cure the delinquency, they’re hiring specialized companies that repossess the vehicles to be sold at auction. The difference between the loan balance and the proceeds from the auction, plus the costs involved, are what a lender loses on the deal.

The repo business, however, is booming.

But delinquencies are a flow: As current delinquencies are hitting the lenders’ balance sheet and income statement, the flow continues and more loans are becoming delinquent. And lenders are still making new loans to risky customers and a portion of those loans will become delinquent too. And now the flow of delinquent loans is increasing – and this isn’t going to stop anytime soon: These loans are out there and new one are being added to them, and a portion of them will be defaulting.

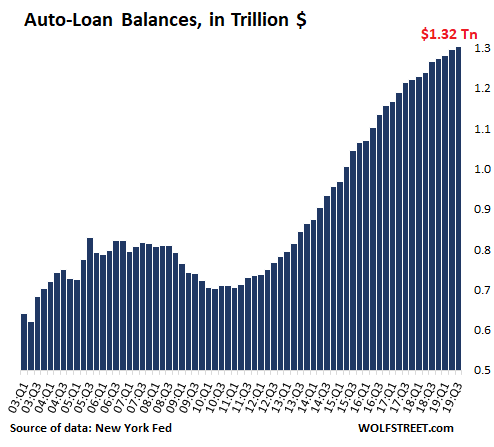

Total outstanding balances of auto loans and leases in Q3, according to the New York Fed’s measure (higher and more inclusive than the Federal Reserve Board of Governors’ consumer credit data) rose to $1.32 trillion:

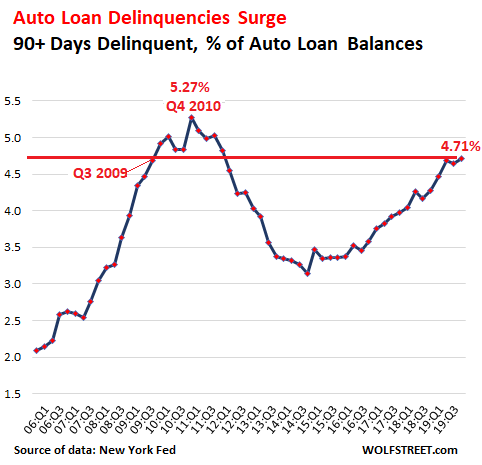

Serious delinquencies jumped to 4.71% of these $1.32 trillion in total loans and leases outstanding, the highest since Q4 2011, when the auto industry was emerging from collapse. And on the way up, this 4.71% is just above the level of Q3 2009, months after GM and Chrysler had filed for bankruptcy and a year after Lehman had filed for bankruptcy, when the US was confronting the worst unemployment crisis since the Great Depression, and when people were defaulting on their auto loans because they’d lost their jobs:

The current rate of 4.71% is just 56 basis points below the peak of Q4 2010. But these are the good times – and not an employment crisis, when millions of people who lost their jobs cannot make their loan payments.

So what is going to happen to auto loan delinquencies when employment experiences a pullback, even a fairly modest one, such as when one million people lose their jobs? That was a rhetorical question. We know what will happen: The serious delinquency rate will set a record for the annals of history. But it’s even worse than it looks.

“Prime” auto loans have minuscule default rates. The total of $1.3 billion in auto loans and leases outstanding includes leases to consumers who could pay cash for the vehicles but lease them for various reasons. According to a different measure by Fitch, “prime” auto loans currently have a 60-day delinquency rate hovering at a historically low 0.28%.

Of the $1.32 trillion in auto loans outstanding, about 22% are subprime, so about $300 billion. Of them roughly, $62 billion are seriously delinquent – or around 20% of all subprime loans outstanding. One in five!

But this subprime delinquency fiasco is not a sign of an employment crisis and a brutal recession as these types of numbers indicated during the Financial Crisis. Employment is still growing, and unemployment claims are near historic lows. Nevertheless, subprime auto loans are defaulting at astounding rates. What’s going on? Greed – not an economic crisis.

Subprime lending is risky but immensely profitable. The thing is: Customers who have a subprime credit rating are painfully aware of it. They have been turned down for low-interest rate loans. They have been turned away. And now they walk on a car lot where their credit rating suddenly is no problem. And they become sitting ducks. The industry knows this.

They don’t even negotiate. They just accept the price, the payment, the interest rate, and the trade-in value. They’re ecstatic to get a car. And they end up with a huge payment at a high interest rate, and given how strung out they already are to be subprime rated in the first place, that loan is doomed.

That’s the irony: a low-interest-rate loan on an affordable car, sold at an average profit, would give the customer a much higher chance of keeping the loan current than a loan with a 15% interest rate on a car the customer cannot afford, including a big-fat dealer profit of the type that can only be obtained from a sitting duck. Those loans, born out of greed, and are doomed.

This is what we’re seeing here. These loans were born out of greed over the past few years, as the industry was getting very aggressive in pursuing subprime rated customers because they’re sitting ducks and so immensely profitable. What we’re seeing now are the consequences of that greed.

Bad debts are written off.

They should be... but sometimes the creditors are bailed out. See relatively recent history.

I’ve been waiting to pick up a lightly used SUV cheap.

If people can’t afford to make payments on their subprime loan, no collection agency is going to go after them.

Not worth it. You don’t loan money to people who are poor credit risks.

Perhaps if the stopped giving loans to delinquents, there would be fewer delinquent loans

Do some people buy or lease cars they really can’t afford? Is that part of the problem? How do so many afford the Lexus and Lincoln Navigator vehicles, which seem to be all over the place, at least in my area?

How much of that is from loans to “protected groups” who cannot be turned down lest the lender face discrimination lawsuits?

Well, you do if you can charge 25% interest. For a car loan.

All you have to do is observe what’s parked at Walmart to know how bad this problem is.

How the lenders are making money is baffling to me.

What’s the point to this doom and gloom article?

Should the government step in and regulate auto industry interest rates? How about debt forgiveness like socialists want for student loans?

The real problem today in the auto industry is NOT subprime loans.

It’s the fact that a new car today has an average sale price of over 35,000 bucks. Even middle class 700 plus FICO scoring Americans who could buy these cars - Aren’t.

“Not worth it. You don’t loan money to people who are poor credit risks“

You do if the government backs them. There are limitless tax payers

How do so many afford

they cant

Yup. I don’t shed tears for creditors who approve bad loans. If they want to lose the shirt off their backs, that’s their business.

These lenders are running a racket that literally leaves them broke the minute money leaves the house.

Nobody should be in the subprime loan market in the first place.

You’re talking about government-guaranteed loans. Not the subprime market.

> I’ve been waiting to pick up a lightly used SUV cheap.

Yep, I read the article as an opportunity and a reminder.

They’re still making a ####ing fortune and who are they kidding??

The interest rates are astronomical on the MAJORITY that are paying off their loan.

The loss is the DIFFERENCE between car value and sale at auction, not a TOTAL loss like credit cards.

Cry me a ####ing river.

No bailouts...

Save cash. Pay cash. Save cash.

But its a Golden Age for the repo business.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.