Skip to comments.

Fed Admits Failure of ‘Plan A’ to Control Money Market Rates, Shifts Back to Repos ...

WolfStreet.com ^

| 20 September 2019

| Wolf Richter

Posted on 09/20/2019 11:35:56 PM PDT by Yosemitest

Fed Admits Failure of ‘Plan A’ to Control Money Market Rates,

Shifts Back to Repos (which was ‘Plan A’ till 2008)

The hullabaloo in the repo market torpedoed the function of Interest on Excess Reserves and forced the Fed to go back to the future.

With its announcement this morning, the New York Fed confirmed that the Fed’s Plan A of manipulating the federal funds rate into its target range – now between 1.75% and 2.0% — has miserably failed,

and that it will switch to Plan B to control short-term interest rates.

But this Plan B used to be Plan A that the Fed had routinely deployed to control short-term interest rates before the Financial Crisis.

So back to the future.

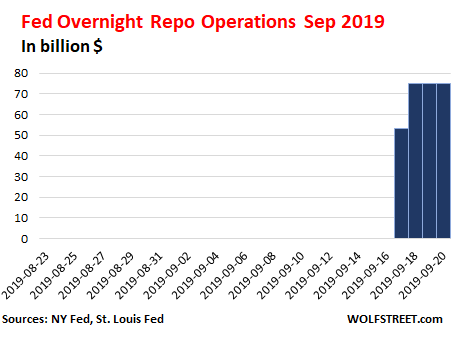

The “repo operations” the New York Fed has been conducting since Tuesday were overnight repurchase agreements (ultra-short-term loans),

where in the morning, the New York Fed offers up to $75 billion in cash at an interest rate that is within the Fed’s target range.

These loans are secured by collateral.

The allowed collateral are Treasury securities, Agency securities, and mortgage-backed securities guaranteed by the Government Sponsored Enterprises (GSEs).

These are overnight interest-bearing loans unwind the next morning, with the Fed getting its $75 billion in cash back, and the dealers getting their collateral back.

As these operations were undertaken every day for the past four days, it’s essentially the same $75 billion that gets recycled every day.

The daily amounts are not additive.

And these operations have nothing to do with QE.

Back in the day, the New York Fed used to conduct these repo operations routinely.

But in September 2008, when Lehman and AIG collapsed, the Fed switched from repo operations to emergency bailout loans, zero-interest-rate policy (ZIRP), QE, and other tricks and devices.

Repos were no longer needed to control rates.

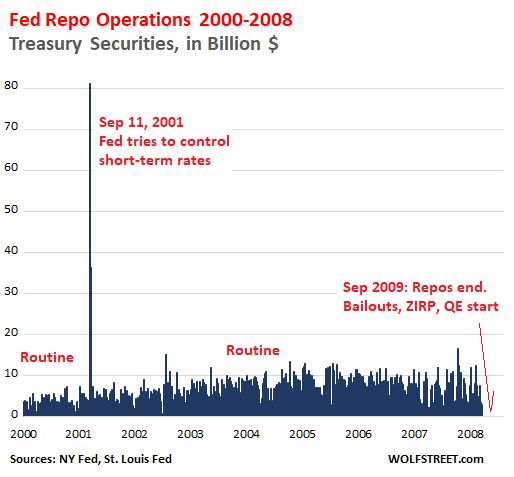

The chart below shows the tail-end of the era of repo operations through 2008.

The spike in repo operations following September 11, 2001, occurred when the Fed briefly injected massive amounts of cash via repos, as funding had dried up, and short-term rates were blowing out:

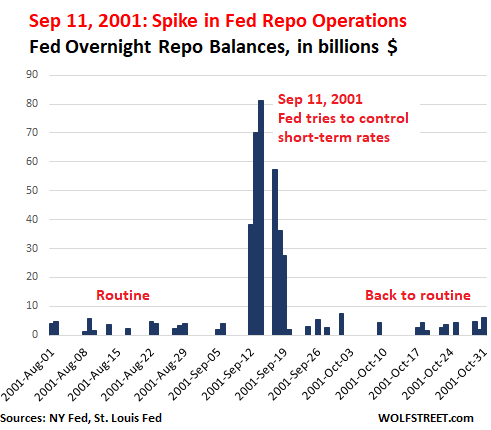

During the September 11, 2001 panic, the Fed conducted these massive repo operations for six mornings in a row.

Like all overnight repos, these repos unwound the next day, with the Fed getting its cash back and with banks getting their collateral back.

This chart shows the detail of those operations.

Note the amounts, reaching $81 billion on September 14, 2001.

Four days later, the operations were over, markets had settled down, overnight funding was plentiful, the Fed got its cash back, and the dealers got their collateral back:

In September 2008, when the US financial system was threatening to freeze up, the Fed developed new tools on the spot, including bailout emergency loans to banks, industrial companies, and market players under a variety of programs,

and it shifted to ZIRP and QE.

But it stopped the repo operations because they weren’t needed anymore.

Before the Financial Crisis, there were no Excess Reserves, which are deposits that banks park at the Fed to earn the interest, have instant liquidity, and fulfill regulatory capital and liquidity requirements.

Excess Reserves started piling up in parallel with QE and peaked in December 2014.

Since then, they have fallen by nearly half, to $1.38 trillion.

By paying banks interest on the Excess Reserves (IOER) at a rate equal to the upper limit of its target range, the Fed figured that banks would see to it that the federal funds rate would be less than the IOER.

This would keep the federal funds rate within the Fed’s target range.

This worked until it didn’t.

Throughout 2018, the federal funds rate hobbled along at the upper limit of the Fed’s target range and occasionally exceeded the limit.

The Fed reacted several times by adjusting the IOER to where it was further and further below the upper limit of its target range.

That worked until it didn’t.

And on Monday this week, all heck broke loose in the short-term funding market, which is precisely what the Fed is supposed to be able to keep under control.

On Tuesday, the New York Fed announced its first repo operation since September 2008.

But the magnitude of the financial world has changed over those years: In 2001, the total amount of Treasury debt was $5.6 trillion.

Now it is over four times larger, $22.6 trillion.

Financialization of everything is a booming business,and the bets have gotten larger, the debt has gotten larger, there is more collateral, and so the amounts have gotten much larger.

If peak-repo day on Sep 14, 2001, is multiplied by four, in parallel with the growth of the US Treasury debt, an equivalent overnight repo operation today would amount to $244 billion.

So the $75 billion this morning is small fry.

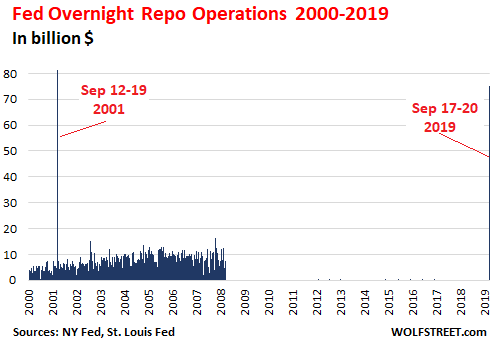

In the chart below of 19 years of repo operations, the thin line on the right represents the past four days:

Just looking at the repo operations of the last 30 days:

Admission that Plan A failed; Plan B is now standard.

So here is what the New York Fed, which handles the repos, announced this morning “to help maintain the federal funds rate within the target range”:

1. Overnight repo operations will continue through October 10; on Sep 23, for “$75 billion”;

on the remaining days for “at least $75 billion.”

These repos unwind the next day, with the NY Fed getting its cash back and dealers getting their collateral back.

21. Three 14-day repo operations for “at least $30 billion each” (Sep 24, Sep 26, and Sep 27).

Each unwinds after 14 days, with the NY Fed getting its cash back, and dealers getting their collateral back.

3. After October 10, 2019, the NY Fed will conduct repo operations “as necessary to help maintain the federal funds rate in the target range.”

This third point is admission that the repo facility is now once again an integral part of managing short-term interest rates, as it was before September 2008.

The St. Louis Fed already proposed this months ago.

The St. Louis Fed published two papers on the benefits of a “Standing Repo Facility,” This standing repo facility is now in operation, officialized by the New York Fed as of this morning.

The two key – but “distinct” – motivations for a standing repo facility are, as cited in the follow-up paper:

First, the facility could be used to support interest rate control by establishing a ceiling on repo rates, thereby guarding against unwanted spikes in money market rates.

The use of a ceiling tool for this purpose would be seen as enhancing the monetary policy operating regime of the FOMC.

Second, the facility could be used to reduce the demand for reserves for any given rate of interest on excess reserves.

The first motivation is why the NY Fed uses the facility now: to control spikes in money market rates as seen over the past week

and keep the federal funds rate within the Fed’s target range.

The second motivation would be to reduce the excess reserves presumably needed to control the federal funds rate via the IOER.

These reserves and the IOER would become less important, because repo operations now pick up much of the work of controlling money market rates.

And the level of those reserves (currently $1.38 trillion) could be reduced further, allowing the Fed’s balance sheet to shrink further:

Why the desire to minimize the demand for reserves ?

In short, because it accords with the FOMC’s stated preference to operate a floor system with the minimum level of reserves necessary to permit the efficient and effective conduct of monetary policy: “minimally ample reserves” for short.

So this standing repo facility, as we’re looking at it today, takes pressure off those reserves,

and it takes the Fed back a step closer to managing short term rates as it used to do before the Financial Crisis.

Nevertheless, the fact that the Fed was forced all of a sudden by a panicky market to abandon Plan A and revert to how it used to do it, rather than implementing the transition methodically, on its own, in its gradual manner,

must have come as a shock.

TOPICS: Business/Economy; Extended News; Government; News/Current Events

KEYWORDS: bailout; bank; blackswan; debt; deficit; fed; fedrate; inflation; mmt; modernmonetarytheory; moneyprinting; qe; repurchaseagreement

Navigation: use the links below to view more comments.

first previous 1-20 ... 41-60, 61-80, 81-100, 101-120 next last

To: Yosemitest

Inevitable consequences of pretending debt is money...

To: Drago

Also, what is your opinion on the “2% inflation target” shouldn’t it be “0%/stable prices”0% is too difficult to hit. Their price measurements have a lag. Deflation is bad. It's easier to just try to target a low, positive number.

I see 5-6% annual inflation in what I buy

What are you buying?

Or do you think Jim W. is way off?

Yes, his imaginary calculations are way, way off.

To: babble-on

The New York Fed fired their chief of market operations earlier this year, Mr. Simon Potter. The new guy was apparently not ready for prime time.

Interesting. Why did the fire Simon Potter?

To: Drago

“OK, then the repo market is a “bank has bond holdings and sells them short term for reserve cash then buys them back in 24 hours” type thing? “

Yep.

“That I sorta get...but the N.Y. Fed has to get the cash to buy the bonds from somewhere, so sort-term QE I guess?”

The Fed creates a cash balance to exchange for the bonds. That cash then “disappears” when the Fed hands the bonds back to the banks. It’s converting illiquid bonds into liquid money for the life of the repo.

“Also, what is your opinion on the “2% inflation target” shouldn’t it be “0%/stable prices”, or does that mess with the “full employment mandate”? “

IMO it comes from the full employment mandate- something that Congress has ordered the Fed to aim at. If we still had the gold standard I think they’d have to go for price stability.

“I see 5-6% annual inflation in what I buy when they shoot for a “2%” “core” rate,”

In the view of Milton Friedman and the Quantity of Money school, inflation is a purely monetary phenomenon that will cause a rise in all prices, not just some prices.

Prices rise (and fall) for all sorts of reasons having nothing to do with the quantity of money, so the prices of familiar items isn’t always a reliable guide.

If we have another inflation like the 1970s you will spend your money on hard goods as fast as you get it. You’ll know there is inflation. Everyone will know.

“Or do you think Jim W. is way off?

I wouldn’t dismiss Williams. Interest rates aren’t including any inflation premium at all. So if he’s right on inflation it would pay to borrow long and pay off the loan in depreciated dollars.

64

posted on

09/21/2019 3:12:29 PM PDT

by

Pelham

(Secure Voter ID. Mexico has it, because unlike us they take voting seriously)

To: Toddsterpatriot

What I am seeing:

Healthcare ave.yearly increase: 12%-18%

PG&E elect. & nat. gas: ave. 8% increase per year.

CA gasoline @ about $3.55/gal. (fluctuates between $2.25 & $4.25 over prior decades).

Restaurants/fast food observed about 5%-7% per year over the last 15 years.

Misc. “Home Goods” (appliances, small electrics, etc.) about 2-3% per year.

Groceries, pretty stable, maybe 1%-2% per year over the last 10 years.

Several of those may be “CA specific” due to crazy regs..

My personal “inflation index” is my Carl’s, Jr./Hardees index: Southwest Chicken Sandwich large combo w/fries-drink = $7.25 in 2007....same combo in the same city in 2019 = $12.50...~73% increase over 12 years equals about 6% inflation per year. My math may be suspect, but my perception/feelings is/are key! ;-)

65

posted on

09/21/2019 3:19:57 PM PDT

by

Drago

To: northislander

“Inevitable consequences of pretending debt is money...”

During the National Bank Era from Lincoln until 1913, banks held Treasury paper (debt) as their reserves to back the money that they loaned.

Treating debt as money is about as old as banking itself. Pretty sure that Adam Smith was an advocate of the Real Bills doctrine, Real Bills being a name for short term commercial debt.

66

posted on

09/21/2019 3:22:38 PM PDT

by

Pelham

(Secure Voter ID. Mexico has it, because unlike us they take voting seriously)

To: Toddsterpatriot

"... but I believe the Fed's thinking" is that those interest rates will draw back in some of the worthless dollars they've printed."

"Draw back in from where ?

To where ?"

The Fed has printed all these worthless dollars, either in real paper or in electronic money (which, sooner or later, becomes real dollars) and put them in the banks to be loaned out and used, whether to cover Federal dollars in peoples' pay, or retirement, or whatever.

Remember the three aircraft that Obama took to the Muslims with pallet loads of cash (1.5 Billion Dollars), to get the four hostages back and a "Nuclear Deal", and the rest of the 150 Billon Dollars of funds were transfer electronically to them..

Then later, when their story is that "we're in better shape economically", they raise interest rates to take back in, or remove from the economy, those worthless dollars they suddenly made out of thin air.

67

posted on

09/21/2019 3:24:30 PM PDT

by

Yosemitest

(It's SIMPLE ! ... Fight, ... or Die !)

To: Pelham

Thanks for that info..

So if/when the U.S. has negative rates, I should borrow dollars and buy gold and come out ahead on the loan?!?! Sounds like a good deal! ;-) The Fed needs to publish a white paper/.PDF/web page titled “Why the Fed is on the side of Main Street middle-class Americans”. I get the basic premise...(1920’s/30’s bank failures/bank runs, “regional” currency problems, etc.), but I have a problem when their “inflation target”/core inflation #’s don’t line up with middle-class wage increases over a long time period (i.e. wages are behind the curve).

68

posted on

09/21/2019 3:35:19 PM PDT

by

Drago

To: Drago

“So if/when the U.S. has negative rates, I should borrow dollars and buy gold and come out ahead on the loan?!?! “

Your guess is as good as mine. Markets sometimes do the exact opposite of what appears to make sense to me.

I don’t think that negative interest rates filter down to the level of individual savers. I looked into that once and IIRC it’s aimed at huge balances.

69

posted on

09/21/2019 3:40:00 PM PDT

by

Pelham

(Secure Voter ID. Mexico has it, because unlike us they take voting seriously)

To: Pelham

Not fair!!! I should be able to borrow $$ at the rates “evil banks” get to!!! (So I can take it and lend it out at 5-12% interest in my “Lending Club” account {arbitrage}). That is why the “private bank owned Fed is ripping us off” argument comes about! They need a PR department.

70

posted on

09/21/2019 3:47:06 PM PDT

by

Drago

To: Drago

~73% increase over 12 years equals about 6% inflation per year. My math may be suspect, but my perception/feelings is/are key! ;-) That works out to a 4.7% increase per year.

To: Yosemitest

The Fed has printed all these worthless dollars, either in real paper or in electronic money (which, sooner or later, becomes real dollars) and put them in the banks to be loaned out and used, whether to cover Federal dollars in peoples' pay, or retirement, or whatever.And these short term repos are the Fed temporarily "printing" more dollars. Still not sure what you meant by "draw back in some of the worthless dollars"

Then later, when their story is that "we're in better shape economically", they raise interest rates to take back in, or remove from the economy,

Raising the Fed Funds rate doesn't reduce the Fed's balance sheet. Doesn't remove "printed dollars" from the economy. FYI, they just cut the Fed Funds rate on Tuesday.

To: Yosemitest

73

posted on

09/21/2019 4:00:21 PM PDT

by

jdsteel

(Americans are Dreamers too!!!)

To: Yosemitest

The gold standard has it’s own problems. Nothing is perfect.

Like most people that have a hatred for the Fed you seem to hate things you THINK it does that are bad and miss all the valid reasons for hating the Fed.

I could go on about those, but in the end there isn’t a better solution....though it does need to be audited annually. More transparency would be a good thing.

74

posted on

09/21/2019 4:03:55 PM PDT

by

jdsteel

(Americans are Dreamers too!!!)

To: Toddsterpatriot

I think what's really going on is

banks are loaning out more money than they have to cover businesses

that are trying to raise funds thru buying and selling hedge funds.

When their "short bets" are going the wrong way, and they get a "Call", they have to come up with the cash to cover those "shorts" and they borrow it from the banks (who say they'll loan them the funds, but then at the end of the day, the banks realize that they don't have those funds to loan.)

Or a similar situation could happen with their "long bets" that those businesses were counting on to be able to sell at a profit, but come payroll time, the "longs" have lost money and they don't have the funds to cover payroll.

So they call the banks to borrow the funds to cover payroll, and the banks say they'll loan them the funds (that the banks don't have) and count on the Fed's repurchase (repo) loans.

All in all, it's a sign of really big trouble, bad management, and poor judgment.

The Fed is simple delaying the economic collapse that we need, in order to get rid of these bad managers and companies.

And the TAX PAYERS are the ones who'll get stuck with the bills, and who's savings are diminished with this 'pretend-it's-not-Quantitate Easing' farce called "Repurchase (repo) Loans".

The quicker we get a "reset" and weed out these bad players, the quicker we can have real recovery.

75

posted on

09/21/2019 4:05:37 PM PDT

by

Yosemitest

(It's SIMPLE ! ... Fight, ... or Die !)

To: Yosemitest

The Fed is simple delaying the economic collapse that we need, in order to get rid of these bad managers and companies. The last time we got a "needed collapse", we suffered through eight years of Obama's idiocy.

To: jdsteel

The Fed made the Great Depression WORSE,

and drug out a normal recovery, that should have only been 2 or 3 years long, and made it 10 years.

We need to get rid of the Fed !

This time, the Fed's setting us up for a Depression that will last a lot longer than 10 years, and will be much, much worse than in the 1930s.

77

posted on

09/21/2019 4:14:13 PM PDT

by

Yosemitest

(It's SIMPLE ! ... Fight, ... or Die !)

To: Toddsterpatriot

And the LAME STREAM MEDIA is still trying to say those years were a good economy.

78

posted on

09/21/2019 4:15:49 PM PDT

by

Yosemitest

(It's SIMPLE ! ... Fight, ... or Die !)

To: Yosemitest

The Fed made the Great Depression WORSE,Yup. And Bernanke was determined not to repeat that mistake in 2008.

This time, the Fed's setting us up for a Depression that will last a lot longer than 10 years

How?

To: Toddsterpatriot

By tinkering with everything, when the Fed should stay out of it.

The free economy, left to its own reactions, will solve the problems quickly.

And the corrections won't last 10 years or longer, i.e. Obama.

80

posted on

09/21/2019 4:58:54 PM PDT

by

Yosemitest

(It's SIMPLE ! ... Fight, ... or Die !)

Navigation: use the links below to view more comments.

first previous 1-20 ... 41-60, 61-80, 81-100, 101-120 next last

Disclaimer:

Opinions posted on Free Republic are those of the individual

posters and do not necessarily represent the opinion of Free Republic or its

management. All materials posted herein are protected by copyright law and the

exemption for fair use of copyrighted works.

FreeRepublic.com is powered by software copyright 2000-2008 John Robinson