Posted on 08/05/2011 2:23:37 PM PDT by Kaslin

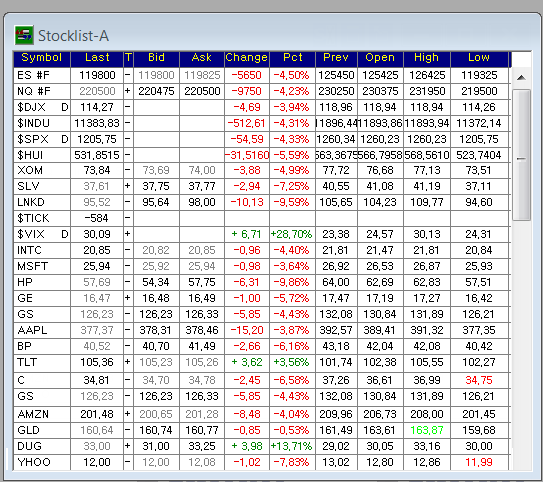

The BNY Mellon apparently does not want money, not to lend, not at all. In a mad dash for cash Mellon has been flooded with it. Overnight lending rates went negative.

Please consider BNY Mellon to Slap Fees on Some Big Deposits Amid Global Race to Cash

Bank of New York Mellon Corp. is preparing to charge some large depositors to hold their cash, in the latest sign of the worries roiling global markets.Everyone Hoarding Cash

The big U.S. custodial bank said this week in a note to clients that it will begin slapping a fee next week on customers that have vastly increased their deposit balances over the past month.

The bank cited the heavy dollar deposits it has received over recent weeks, as investors and corporations retreat from financial markets amid Europe's debt crisis and the recent debate over U.S. government borrowing.

BNY Mellon's decision sent money-market mutual funds and financial institutions scrambling to put their cash to work in short-term markets Thursday, sending rates falling across many investments. Treasury bill prices rose, pushing down their yields down sharply, and interest rates on overnight securities repurchase, or repo, agreements tumbled.

The cost of borrowing overnight in this market tumbled below zero Thursday, after starting the day at around 0.08%.

BNY Mellon said that it will charge 0.13% plus an additional fee if the one-month Treasury yield dips below zero on depositors that have accounts with an average monthly balance of $50 million "per client relationship," according to a letter reviewed by The Wall Street Journal. The charges will take effect on accounts held on Aug. 8, and will be charged in the subsequent billing cycle.

The torrent of cash looking for a safe place continues to grow. The Bank of Japan this week intervened in currency markets, essentially printing yen and buying dollars. "Those dollars need to find a home and it's probably going to come to the Treasury market," BofA Merrill Lynch's Mr. Smedley said.

PING

Don’t hear too many economists predicting deflation these days.

PIMCO expects a near Sovereign Default.

I expect both.

Buy and hold cash, both in the bank and under your mattress. I would say buy gold except it's too expensive right now...but it does protect against sovereign default.

Buy it when it crashes.

How can this be with the US printing money by the wheelbarrow load?

Neither do I, just the opposite

In its grand QE experiment the Fed pushed rates to zero, flooded the world with cash, then expected banks to lend and businesses to expand. Did it work?

I have been wondering about something. I do not have much stock market savvy....but what are the chances that a lot this money has left this country? I know that many companies have very good balance sheets but it seems to me they are talking about a lot more money than that. I only say this because the day after we passed the debt ceiling increase we managed to spend upwards of 400 billion. Where exactly did that go?

This is probably the most bizarre thing I have seen.

Why hoard cash? It will be like Confederate money when the whole thing collapses. Totally worthless.

What say youse?

Agreed - and why not take on debt if you can pay it back with worthless dollars?

I'm sure the advice being given out is based on wisdom, but I've not heard good explanations yet.

Soros is hoarding cash too.

He doesn’t have confidence in his boy.

It was most probably used to pay back the unofficial "loans" the government had been taking. In order to avoid default, the government had been borrowing money from, among other places, the federal employee accounts in the Thrift Savings Plan. They had to put that money back and make good any lost interest. However, since most of the TSP funds went down in July, quite likely it ended up being the equivilant of a profitable short sale for the government.

I suspect that what's happening here is that the Fed is printing more money than ever, but the level of economic activity has declined so much that the money isn't circulating with the same velocity anymore. So even in an "easy money" environment we still see some deflationary indicators such as negative interest rates.

Probably a good reason to put some money on it. All those people hoarding cash want to save it for when everything costs more. Right.

less are working now than in June

At these interest rates, you could borrow money to speculate in commodities and other assets and make a fortune.

Since “Great Depression” has been taken we need to call what is about to happen the “Great Fall”.

1. Imagine a person out there who bought a home in the early 1990s for about $250,000.

2. For the sake of this discussion, let's also assume that they either paid cash for the home or financed it with a mortgage that was fully paid off in less than 15 years. This means that the person owned the home in the mid-2000s "free and clear" with no mortgage on it.

3. Suppose this person sells the home in 2006 for $500,000 to a buyer who puts down $50,000 and gets a mortgage for the remaining $450,000. For the sake of this discussion, let's assume that the bank extended this loan under very easy terms with a low short-term interest rate and the fairly lax lending standards that were common at the time.

4. Let's also suppose that the person who sold the home for $500,000 executed some kind of transaction with the money shortly after the sale was done. Maybe they invested in some mutual funds, or paid cash for another home, or donated the money to his favorite charity.

5. Now fast-forward a few years to 2010. The person who bought the home in 2005 for $500,000 learns that the home will only appraise for $375,000.

6. Let's also suppose that the 2005 buyer still owes $425,000 on the original $450,000 mortgage. In effect, this person is "underwater" to the tune of $50,000 because he owes $50,000 more than the home is currently worth.

Now let's go back to #3 and #4 and review what transpired in 2005. The sale of this home and the financial transaction described in #4 would have counted as $1 million worth of economic activity -- including the sale of the home for $500,000 and the subsequent transaction(s) by the seller for another $500,000.

But the 2005 purchase price of the home ($500,000) was based on nothing more than a banking transaction that had no sound basis due to the easy lending standards at the time. Basically, this $450,000 was fabricated out of thin air because the money never "existed" until a bank extended the loan. If the current owner defaults on the mortgage and walks away from the home, the bank is left with a $375,000 home that was put up as collateral for what is now a $425,000 balance on the mortgage. And if the home is now worth only $375,000 then I would legitimately question how much of the original $500,000 sale (or the subsequent activity by the seller) ever really "existed" at all.

If the bank forecloses on the home and finds a buyer at a price of $375,000 now in 2011, then the bank absords a $50,000 loss on the deal. More importantly, there is only $375,000 for the bank to put to work elsewhere. So the $1 million worth of transactions in 2005 becomes $750,000 worth of transactions in 2011.

My suspicion is that most of this money the Fed is dumping into the economy is being picked up by the banks (in the form of low-interest deposits or bank purchases of U.S. Treasury bills) to prop up their balance sheets in order to offset these massive losses on their mortgages.

THANK YOU!!!!! that was a very informative explanation. I can’t tell you how confusing it is listening to what everyone has been saying. Thank you for making sense out of something terribly confusing. Freeper are the best! How much do you know about the effects of an S&P downgrade? I suspect it is just a rumor, but it scares the heck out of me.

“Agreed - and why not take on debt if you can pay it back with worthless dollars?

I’m sure the advice being given out is based on wisdom, but I’ve not heard good explanations yet. “

I’m with you...why pay back in REAL dollars. Just sit on a loan balance (assuming the interest rate is fixed) and then pay back with WORTHLESS dollars.

This deflation stuff only applies when the Fed isn’t out to wreck our currency.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.