SpaceX Low Earth Launch Costs - ARKInvest

SpaceX Low Earth Launch Costs - ARKInvest Posted on 06/08/2026 10:23:12 AM PDT by SeekAndFind

The most anticipated IPO in history will hit the market next week. When Elon Musk is involved, opinions tend to be firmly on one side or the other. In the case of the IPO S-1 filing , mention of colonizing Mars and mining asteroids only adds to the division.

Today we are avoiding the spectacle and having a look at what the business is really about: the opportunities, the challenges and what the listing could mean for investors.

Here’s a quick summary of what’s been going on:

🤖 India loses edge as investors flock to Asia’s AI hubs ( CNBC )

What happened: India has found itself on the wrong side of more than one trend lately. Energy and fertilizer costs are soaring due to the war in the Strait of Hormuz. Higher costs are hitting consumption, which is a key part of the growth narrative. At the same time investors are rushing to the Asian markets with AI exposure, an area where India lags. In particular, Taiwan and Korea’s markets are now highly concentrated AI bets.

How it impacts investors: The way capital is chasing growth and momentum should also be seen as a warning: things can turn very quickly. India is now becoming a contrarian bet in Asia. It may turn out to be an effective diversifier at some point.

Next steps: Use the Simply Wall St stock screener to hunt for potential opportunities in India;s equity market.

💸 Alphabet's $80 billion share sale puts capital markets in "unprecedented territory" ( CNBC )

What happened: Google's parent company has launched the largest equity offering in corporate history to fund its AI buildout. This is the first time one of the Mag 7’s AI capex ambitions have outgrown its ability to self-fund. Alphabet has raised projected capex for 2026 to between $180 billion and $190 billion, and said further increases in 2027 are likely too.

How it impacts investors: Google may also be anticipating a squeeze on capital, with three trillion dollar IPOs on the way, and competitors increasing capex at the same time.

Next steps: This is positive for the entire AI infrastructure supply chain. Check out the AI picks and shovels collection and this Powering the AI Revolution: Next-Gen Energy & Grid watchlist for some ideas.

⚡ SoftBank's €75bn french bet exposes Europe's AI power problem ( CNBC )

What happened: SoftBank plans to build 3.1 GW of AI data centers in northern France by 2031, including sites in Dunkirk, Bosquel, and Bouchain — its largest AI infrastructure investment in Europe. With over 60% of its power needs met by nuclear energy, France is uniquely placed to handle energy-intensive data center projects at a time when European industrial electricity prices are roughly double those in the US.

How it impacts investors: This is a reminder also a blunt reminder that Europe's energy costs remain a liability in the global AI arms race. SoftBank will partner with Schneider Electric on a large-scale industrial production cluster giving France a foothold in the AI supply chain.

Next steps: Europe’s tight energy markets make capacity expansion an imperative. You can explore the energy and utilities sectors in Europe with the Simply Wall St stock screener . You can also check the Schneider Electric company report to find peers and competitors.

Let’s start by laying out the key numbers:

The financials (2025):

| Revenue ($ Billions) | Operating profit/loss ($ Billions) | |

| Space (launch) | $4.1 | -$0.6 |

| Connectivity (Starlink) | $11.4 | $4.4 |

| AI (xAI and X) | $3.2 | -$6.4 |

| Total | $18.7 | -$2.6 |

Context for the $1.75 trillion valuation target:

SpaceX is known as a space business, but it’s evolving into more of an AI business now. The filing doc identifies a TAM (total addressable market) of $28.5 trillion. Regardless of how realistic that is, less than $2 trillion is related to space and connectivity.

The big vision might be about making ‘life multiplanetary’ and colonizing Mars, the biggest immediate opportunity (and capex) is very much focused on AI. Nevertheless the space and connectivity segments are also crucial cogs.

The Opportunity

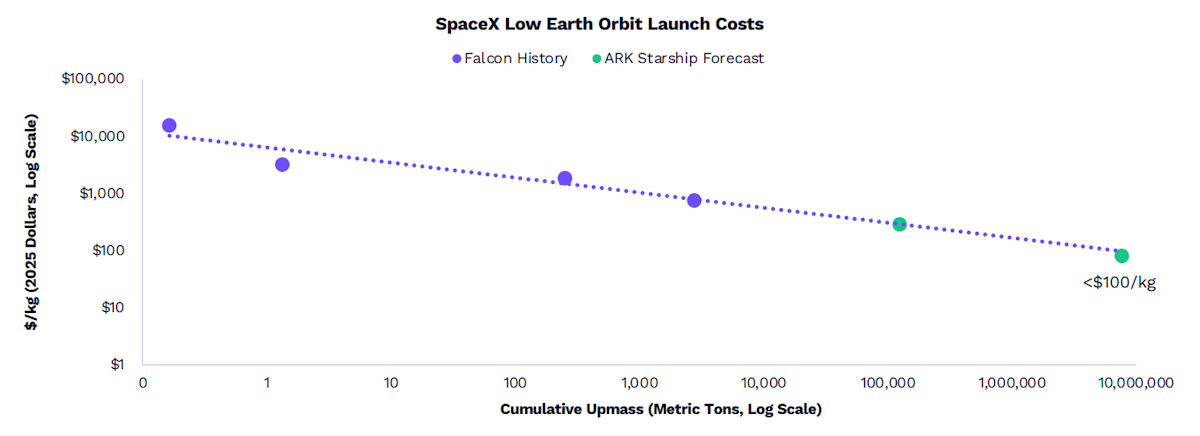

SpaceX effectively dominates the global launch market. The company’s success with reusable boosters, and its ability to scale, have completely changed the economics of getting objects into orbit. SpaceX Low Earth Launch Costs - ARKInvest

Significantly lower launch costs make more use cases viable for SpaceX and for its customers. And owning the dominant launch business also gives SpaceX a cost advantage for any of its businesses that use the platform.

Challenges and Risks

The launch business is a low margin, and capital intensive business, though it exists to provide a platform for SpaceX’s other ambitions.

The future of SpaceX depends largely on making the massive Starship vehicle fully and rapidly reusable. In particular, the heat shield material needs to repeatedly withstand thermal stress. This is a crucial engineering challenge that hasn’t been solved yet. In fact, the S-1 even warns that the rocket program (amongst other programs) "may never achieve commercial viability"

In addition, the launch business has struggled to get to a reliable launch cadence for its V2 Starlink satellites.

The Opportunity

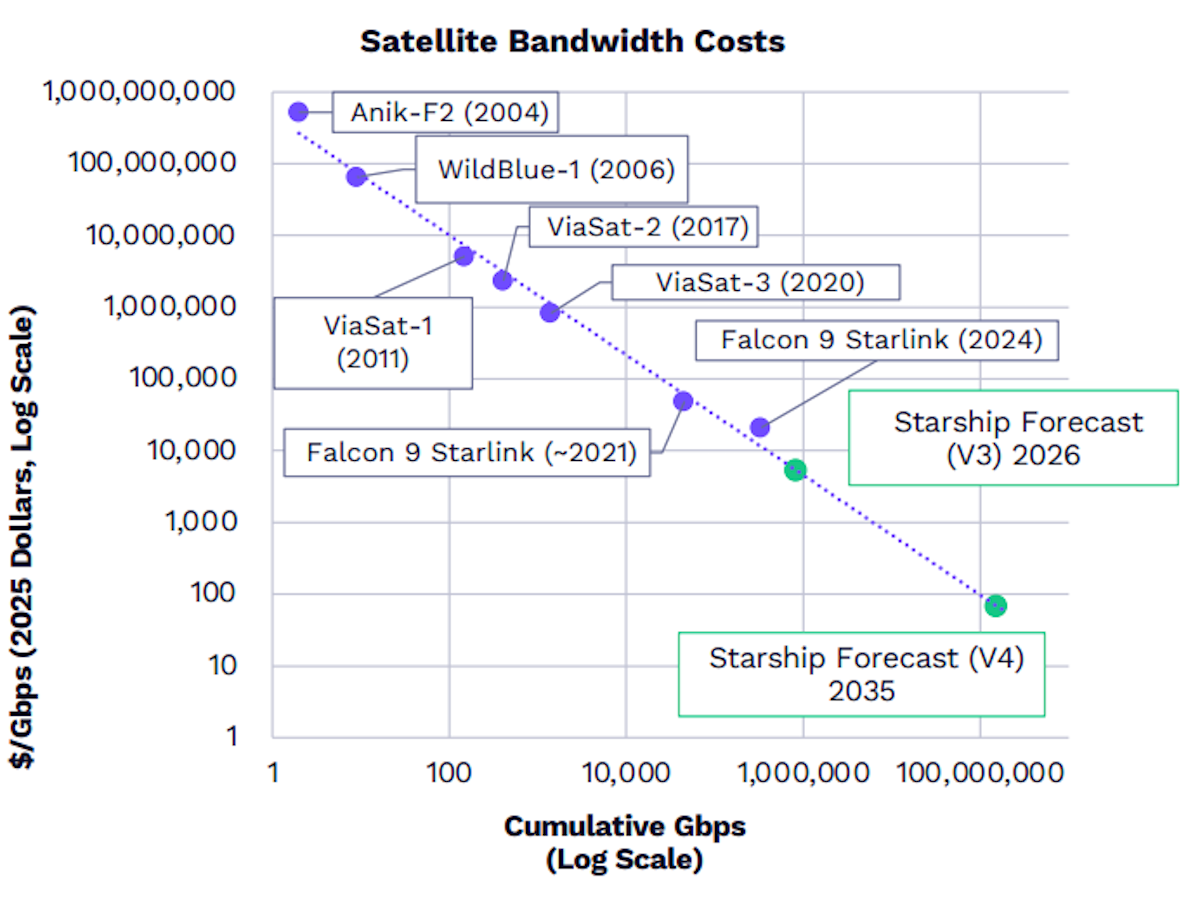

Starlink, which provides fixed broadband and direct-to-cell connectivity via satellite, is the most profitable segment. Falling launch costs have resulted in falling bandwidth costs, allowing Starlink to target a larger market. Satellite Bandwidth Costs - ARKInvest

Satellite Bandwidth Costs - ARKInvest

Starlink currently has 10 million subscribers, a fraction of its potential market . In particular, parts of the world that are underserved by mobile and terrestrial networks are key opportunities. Africa’s mobile penetration rate is below 50%, with mobile internet penetration at 28% (i.e. ~400 million people).

Direct-to-cell connections (which don’t require special hardware) mean mobile carriers around the world could ultimately be disrupted. SpaceX has also acquired spectrum licenses from EchoStar, expanding its footprint substantially.

Competition in this space is increasing, but Starlink has a major scale and cost advantage.

Challenges and Risks

Starlink has several challenges, on the technical, financial and regulatory front:

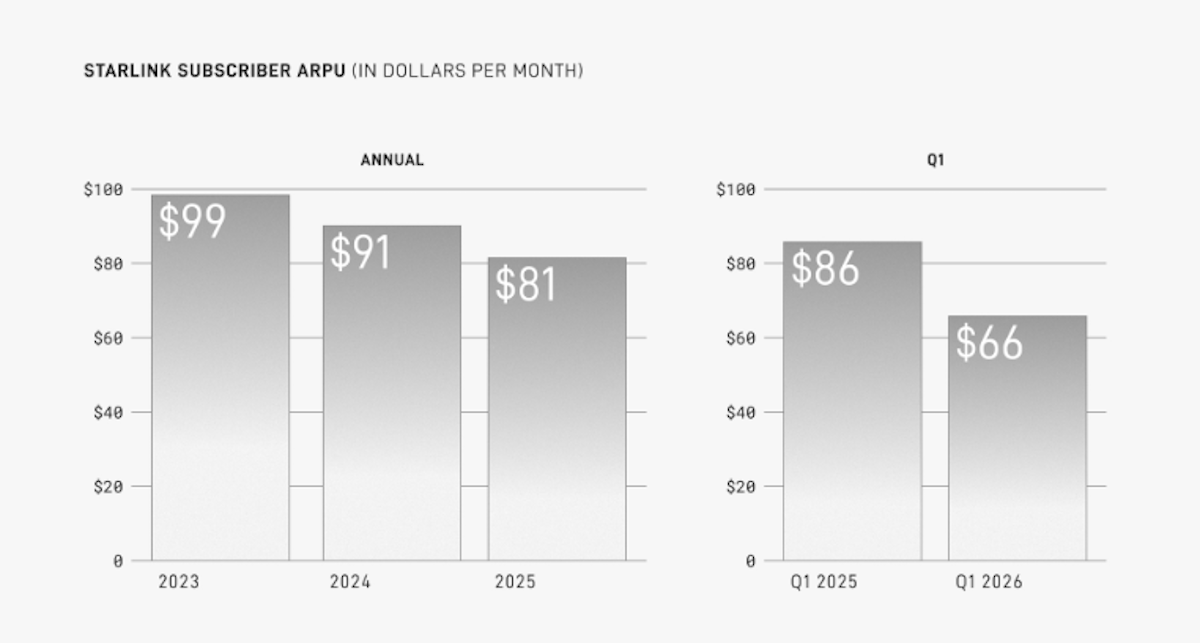

Starlink monthly ARPU - SpaceX S-1 Document

Starlink monthly ARPU - SpaceX S-1 Document The Opportunity

Whether by accident or design, AI has become the core opportunity for SpaceX. Demand for AI compute power is surging, as shown by xAI’s recent deal with Anthropic.

Anthropic will be paying $1.25 billion per month for compute power from the Colossus 1 data center. This implies that xAI doesn’t anticipate enough demand for its own Grok LLM, but it's not a bad plan B, and almost doubles the company’s revenue.

If demand for AI compute does continue to grow, then SpaceX is building the full AI stack:

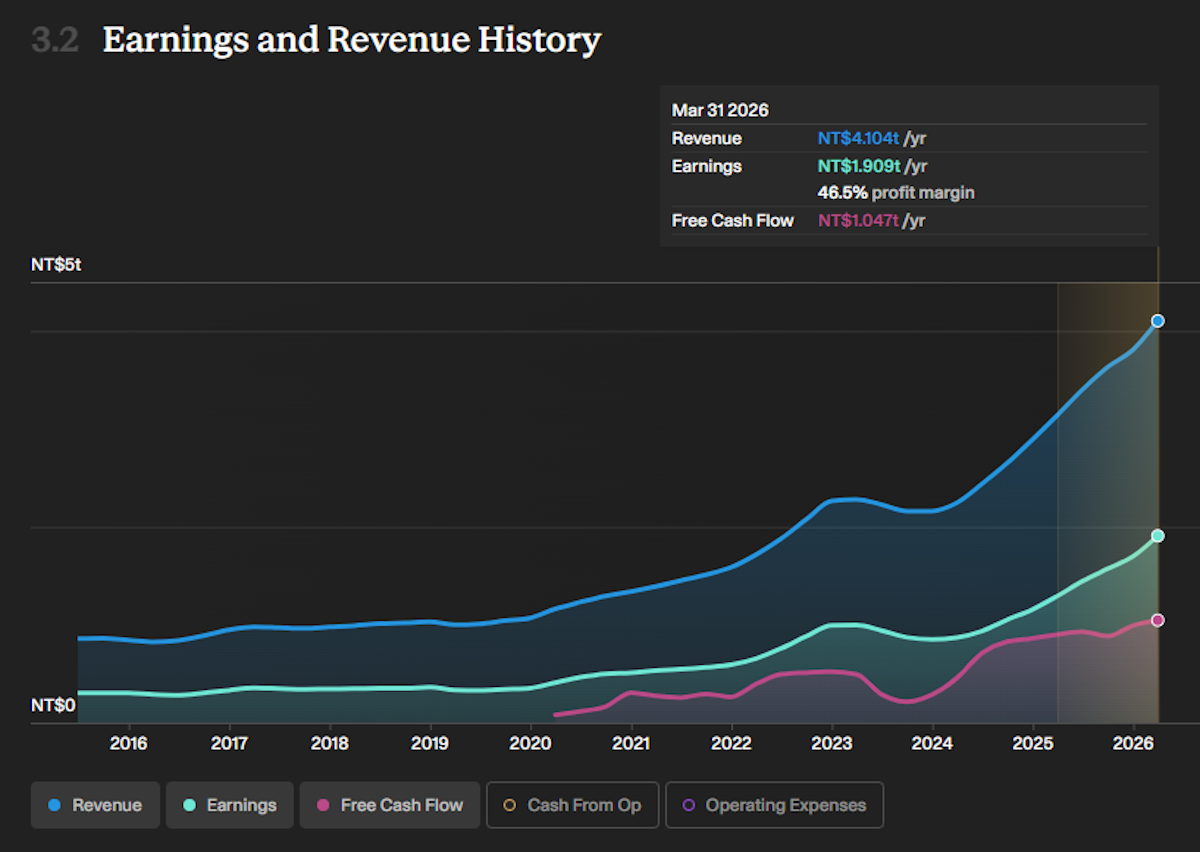

The chart below shows TSMC’s net margin, which is currently 46%, and it’s been above 30% for the past 10 years. This is a key part of the SpaceX strategy. Every bit of margin that SpaceX can avoid paying is an opportunity to gain a cost advantage. TSMC: revenue, earnings and cash flow - Simply Wall St

TSMC: revenue, earnings and cash flow - Simply Wall St

Challenges and Risks

This incredibly ambitious plan obviously comes with incredibly big challenges. These are the most notable ones:

This IPO is unprecedented in size, and is likely to have implications for the broader market. Based on closing prices on 3rd June, and a $1.75 billion market cap, SpaceX would rank as #9 in the global market cap table. Coincidentally this is just ahead of Tesla.

The Trillion Dollar Club

| No. | Company | Market cap (US$ Billions) | S&P 500 weight | Nasdaq 100 weight | Price to sales (P/S) ratio | Net income margin |

| 1 | Nvidia | $5,220 | 8.4% | 8.6% | 21 | 63% |

| 2 | Apple | $4,540 | 6.9% | 7.1% | 10 | 27% |

| 3 | Alphabet | $4,330 | 6.0% | 6.7% | 10 | 38% |

| 4 | Microsoft | $3,160 | 5.3% | 5.4% | 10 | 39% |

| 5 | Amazon | $2,670 | 3.9% | 5.1% | 3.6 | 12% |

| 6 | Broadcom | $2,290 | 3.3% | 3.5% | 34 | 37% |

| 7 | TSMC | $2,200 | n/a | n/a | 17 | 47% |

| 8 | Saudi Aramco | $1,760 | n/a | n/a | 4 | 22% |

| 9 | SpaceX | ~$1,750 | TBC | TBC | ~95 | -26% |

| 10 | Tesla | $1,590 | 1.8% | 3.3% | 16 | 4% |

Bending the Index Rules

Based on market cap alone, SpaceX belongs in major indexes like S&P 500 and Nasdaq 100. But index providers usually have other rules, covering free float size, months listed and profitability.

This time, index providers seem to be going out of their way to accommodate SpaceX:

If the S&P inclusion only happens in 6 months time, hedge funds will be attempting to pre-empt the rotation, which could be easier said than done.

If SpaceX does go into the S&P 500 index, anyone invested in any product tracking that index will end up with SpaceX, whether they like it or not, and whether they like the price, at the time of inclusion, or not. It’s worth noting the anticipated price-to-sales ratio of 94 times sales. The highest comparable ratios are Broadcom (34 times sales) and Palantir (65 times sales) both of which are growing and very profitable.

Some are anticipating a move to equal weighted index funds. If this works out badly for ETF investors that could be the case.

Market Liquidity

The implications for index funds will take a while to unfold. In the meantime,

$75 billion is a massive amount of liquidity to be absorbed by the market. The combination of unknown demand, unknown supply from existing shareholders, and a potential liquidity squeeze in other markets, means extreme volatility could be on the cards.

The Tesla Scenarios

There’s a lot of speculation around Tesla, and a potential merger of Musk’s two companies. An amended IPO filing doc included the following text: “may issue a significant amount of equity in connection with future transactions” which only added to the speculation.

There are good reasons for a merger, but it may be worth keeping an open mind. Some analysts have pointed out that it might be more difficult to raise further capital after a merger, and terms for a deal would be difficult to negotiate.

Whether it happens or not this could become a major part of the narrative around Tesla share price. Check the Tesla Community Page to see what others are saying about the outlook.

The Space and AI Ecosystems

Some of the capital being raised will stay within SpaceX. But a lot will ultimately flow to suppliers and partners. Based on the capex plans, the AI ecosystem is in line for the bigger share. That means companies supplying GPUs, CPUs, networking, and energy infrastructure equipment.

But the developments are also positive for the broader aerospace and defense industry , which is also smaller, and getting a lot of attention now. The Beyond the Moon watchlist includes the key space related companies, large and small.

It really isn’t surprising to see the market so divided on the valuation and outlook for SpaceX.

The bull thesis combines innovation, vertical integration, economies of scale and a (currently) very real demand story. If everything goes right, the competitive advantages stack up quickly. But that thesis also includes unproven ideas and problems that still need to be solved.

If you base your thesis only on proven technologies, revenue and margins, the price tag won’t make sense.

The reality for capital intensive businesses is that things take longer and cost more than expected. All the hurdles that need to be overcome or solved, are milestones that need to be ticked off.

If you pay for all the success upfront, there’s no margin for error, and possibly no upside either.

Shareholders living on the Moon will find the gravity of the situation to be somewhat lessened.

LANDING! SpaceX lands B1067 for its 35th time during the Starlink Group 10-35 mission

0:33

Launch Heaven

13.9K subscribers

(buncha) views

June 8, 2026

https://www.youtube.com/watch?v=bUe-N4aeya8

Over 10,000 Starlink sats are up there, Sam’s Club just started carrying (or at least, I just noticed it) the Starlink downlink kits, $55 a month basic service.

Fidelity is making the SpaceX initial public offering (IPO) available to any customer with a retail brokerage account with $2,000 or more in the account.

https://www.fidelity.com/learning-center/trading-investing/spacex-ipo-explained

Is $135 a bargain price? It was $45 in November: https://finance.yahoo.com/quote/SPAX.PVT/

From dial up to compuserve til today, Starlink is by far the best Internet Service I have ever had.I have 3 of them, 1 at each house.

I’m a fan as well, being out in the boonies.

Way better than the copper DSL from Frontier that was my only other option.

Part of me likes the idea of owning a piece of Starlink, but I don’t know the first thing about IPOs other than how to spell them.

The SPCX IPO will open priced according to future valuation, ie at the top. AMZN and META(nee Facebook) opened at a more objective valuation. This will not be the same as buying in early.

“Is $135 a bargain price?”

DYODD of course, but IMO it will be when they add Tesla down the road.

Fidelity has an Indication of Interest or (IOI) while at Schwab you can submit a Conditional Offer to Purchase (COTP) but have to affirm the finalized IPO price, which should already be locked in at $135 but can expect it officially by 6/11 close of Business. I haven’t seen an affirmation yet myself. If your plan is to hold for long term growth, its a good buy at the IPO price.

What the price will do soon after is anyone’s guess, likely rocket higher (no pun intended) before crashing back to Earth and then over compensating for a time. The S&P500 wont change their rules, good for them. Just note there will be increments of unlock at 90, 120 days etc., float is 5% (I think) however Elon and close associates are subject to a one year + one day lock up.

.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.