Skip to comments.

The Griffin Comprehensive Health Care Cost Reform Plan

self

| 11/04/2025

| Brian Griffin

Posted on 11/04/2025 5:32:04 AM PST by Brian Griffin

While the shutdown is needless, the Democrats are right to be concerned about healthcare cost coverage.

MEDICAID EXPANSION FAIRNESS

What I’m thinking of is to slightly and generally increase the state Medicaid expansion share to 5% plus the highest rate of state income tax. That would make Medicaid expansion cheaper for no income tax red states like Florida and Texas, and fairer. Right now, California pays for Medicaid expansion at 10% and rakes in 13% income tax from doctors.

To help finance likely Medicaid expansion to states like Texas and Florida, the state Medicaid shares (traditional & expansion) would increase annually starting in 2028 by a percentage equal to the deficit in the fiscal year ending prior to the calendar year divided by $1 trillion. That would be a 1.5% increase on a $1.5 trillion deficit, or a .6% increase on a $600 billion deficit. To soften this increase for the states, I would have the federal government likewise increase its share of Medicaid drug expenditures. This would have states assume more responsibility for medical service costs, which they regulate, and the federal government assume more responsibility for drug costs, which it has the power to regulate.

Be aware that property tax supported public hospitals such as Parkland in Dallas and Jackson Memorial in Miami exist in Texas and Florida and are heavily used by the indigent. George Bush Jr. would have had to pay about $5,000/year in hospital tax after buying his house after his presidency. If an indigent from another Florida county without a public hospital gets care at my county hospital, my county hospital can collect from that county.

[NOTE: I'm a Floridian.]

SNAP BENEFIT REDUCTION [by 2027]

To free up funds for Medicaid expansion to Florida and Texas, SNAP benefits would be capped at $2.50/day/person, increasing as the CPI does.

[NOTE: For an adult to eat the food my mother prepared would cost about half the current maximum.]

Benefits paid in daily instead of monthly to prevent binge eating disorder.

SNAP benefits would pay for things WIC does, excluding fish but including chicken and pork.

PARTIAL ENHANCED SUBSIDY CONTINUATION [to 2036]

Except as required by the Fair Share PPACA premium minimums below, the monthly to be paid on a plan would not exceed the Schumer formula amount by more than 1.5 times the household's income in percentage terms of FPL exceeds 90% FPL in terms of dollars.

If the household's income is 400% of FPL, the percentage difference is 310% and increase would typically be capped at $465/month.

If the household's income is 300% of FPL, the percentage difference is 210% and increase would typically be capped at $315/month.

FAIR SHARE PPACA PREMIUM MINIMUMS

To help fund likely Medicaid expansion to red states like Texas and Florida, I would impose a premium minimums of the higher of: 1. 1/65th of the Medicare Part B premium amount per insured year of age as of the start of coverage 2. one-tenth the percentage of the policy premium of the household income's as a percentage of FPL.

For a 5-year-old, 7-year-old, 32-year-old and 34-year-old, the ages would sum to 88 and the monthly absolute minimum premium amount would be a (88/65)*$185 or $250.46.

For a 5-year-old kid and a 27-year-old mom the ages would sum to 32 and the monthly absolute minimum premium amount would be (32/65)*$185 or $91.07.

For the second minimum, a family whose income is 300% of FPL would have to pay at least 30% (one-tenth of 300%) of the cost of the policy.

[NOTE: About half the premium is to subsidize unhealthy people. Paying 30% is covering well over 60% of true risks of most such insureds.]

Insurers could waive the mimimums for up to 20% of their PPACA policy holders after the first month's premium is paid provided $20 is paid upfront for a financial review fee. Waivers may not be granted in any space open to insureds (to prevent racial discrimination and threats). Insurers need not waive for the entire remaining term.

HOSPITAL COST REDUCTION [by 2028]

Break most hospitals into two highly competitive entities. Convert other hospitals into real estate leasing entities with competing surgical suites and nursing wings.

INTERSTATE DRUG PLANS

I would allow Federal PPACA exchanges to offer Interstate Class Drug Plans, exempt from state control that cover under contract at the time of policy issue at least: 1. 80% of all FDA-approved recombinant drugs by key active entity 2. 80% of all key FDA breakthrough chemical active entities under patent as of January 1 of the coverage year used in a drug approved by the FDA by August 1 prior 3. 80% of all key chemical active entities under patent as of January 1 of the coverage year used in a drug approved by the FDA by August 1 prior 4. 90% of all WHO “essential” drugs

Plans with lower percentages could be sold, but not on an federally subsidized exchange, only directly or through an agent.

The high percentage but not 100% drug cost coverage system would allow for genuine negotiation between drug plans and drug companies. Drug plans would have an incentive to try to buy drugs from drug companies and drug companies would have an incentive to make deals to make sales.

Formulary drugs would locked in for the policy year and be supplied at on an all-the doctors prescribe basis. Drug plans would typically contract for entire product lines. The co-pays would be roughly equal to mere manufacturing cost. The premiums would be used for R&D cost recovery.

If drug company overplays its hand with one drug plan, it can still get its products on the formulary of another plan.

As with Medicare Part D, a plan shopping system should get developed.

For individual and family plans, drugs not in the formulary need not be covered at all.

Group plans might issue vouchers to insureds at plan set amounts for out-of-formulary drugs. These vouchers might average 80% of average drug class (recombinant large volume, recombinant small volume, etc.) Canadian maximum price. The average would have to be stated. Let the patients wave the voucher at Walgreen's or CVS, or access a drug company voucher redemption webpage. The drug companies will probably gladly take $400 for a two week's supply that might cost them $120. The insurer might offer more in exchange for drug company stock of like value.

Voucher plans would not have fixed premiums.

The Interstate Class Drug Plans would not in the early years be PPACA subsidy eligible.

SEPARATE OUT DRUG COVERAGE

Without having to manage drug coverage, hospital systems can run care coverage systems and cut out most insurance company overhead and meddling. The co-pays and co-insurance would generally be equal to the hospital system's marginal cost so there would be little reason to say no to a doctor's request except for medical cause.

Hospital system plans might charge a monthly age-related fee if you lack a drug plan listed by the hospital system plan.

AFFORDABILITY

Silver plans would be limited to a maximum deductible of three times the Medicare Part A amount [2025: $1676]. A plan should be able to offer at least one maximum benefit premium cost reduction rider. The maximum benefit must not be less than twice the average operation payout of the insurer. The PPACA subsidy base would be reduced in proportion to the premium reduction.

I would also make bronze plans low cost by having co-insurance up to $10,000 at up to 50% with the policy upfront amount paid up front to the insurance company by the insured. Co-insurance percentages would normally be 20% and based on the Medicare amounts unless contractually specified otherwise. Policy percentages might be less for certain things and contractually capped by time periods, by say 50% of the upfront amount the first three months of the calendar year, 60% the first six months of the calendar year, 70% the first eleven months of the calendar year and the whole amount the whole calendar year. The rising percentages are so policyholders are cost sensitive most of the policy term. If and how an upfront amount would get invested would be subject to contract. Unused amounts of upfront money would be refunded after each policy is closed out. A policy would not be closed out until the time allowed for claim submission and needed for claim processing under the policy has expired.

Bronze and silver plans would retain drug coverage.

I would also make copper plans low cost by only covering Part A scope items plus what Part B would pay for any general or regional anesthesia surgery. These would be like the Blue Cross/Blue Shield plans of my youth.

The two operation hospital coverage plan would cover an amount equal to twice the median Medicare DRG hospital amount plus a percentage of say 20% minimum on the Medicare amount for the first operation if the hospital agrees prior to 10 days after discharge to perform any needed second operation for the remaining amount left on the policy. A Blue Shield equivalent rider for the amounts Medicare pays for the surgeon(s) and anesthesiologist(s) might be purchased too.

The new bronze, copper, and two operation hospital coverage plans are meant for higher income folks and would not be PPACA subsidy eligible.

PPACA SUBSIDY BASE AMOUNTS

The subsidy base amounts would be the average of the area's 2025 subsidy base amount and the 2025 subsidy base amounts of those other rating areas within 300 miles of the area the Secretary of HHS may deem appropriate to average in, increased by Medicare Part B premium inflation.

HOSPITAL EMTALA COST ASSISTANCE

I would allow hospitals collect up to $1,000 per incident of EMTALA service from employers, with payment not in excess of $50 per week per employee concerned being due to any and all EMTALA providers and not for more than 100 weeks after service. Such payments on behalf of an employee would be considered to be a debt of the employee to the employer. Employers could collect back from employees and ex-employees (and require EMTALA incident employees to participate in an employer plan). State and federal garnishment limitation laws would not apply.

EMTALA REFORM

To get care under the EMTALA for yourself (or custodial child), the hospital might require you to 1. pay $100 in cash or by financial organization card accepted at the emergency care facility, 2. present for recording a valid coverage card and appropriate matching ID if and as required to use the coverage card, 3. hand over your valid SNAP card and present a matching valid domestic governmental picture ID, 4. hand over your valid domestic driver’s license, 5. hand over your valid US passport, 6. hand over your operable cellphone whose model is listed by a current regulation issued by a Secretary of HHS, or 7. hand over a valid domestic governmental picture ID of yours and a matching financial institution statement less than 70 days old showing a domestic governmental or employer direct deposit of at least $150.

Items handed over may be retained by the emergency care facility until retrieved within one month by the responsible party by paying $100, or more, for the care, plus a retrieval fee not exceeding $50 in a manner the facility accepts. Items not timely retrieved may be disposed of in a legally allowable manner.

MEDICAID ER REFORM

Hospitals may require similar requirements to those of EMTALA Reform but with dollar amounts that are 2/5ths as much.

SNAP CARD ER DEBIT

States might be allowed to authorize emergency care facilities to debit SNAP cards within 30 days of service for ER incidents.

DRUG PATENT REFORM [future]

Drug patents would be limited by government sourced product revenue and overall domestic government health care spending and not strictly by time so drug companies and their shareholders would have an incentive to fight to minimize government health care funding.

Upon FDA marketing approval of a covered entity, a Kirchoff patent would collapse to that entity.

MEDICAL/DENTAL EDUCATION/LICENSING REFORM [near future]

Medical and dental education would be broken down into far simpler chunks (with some overlap) and start in the first year of college.

States may choose to create new licensing categories. Reform would not include federal licensing.

STUDENT LOAN REFORM

To encourage states to go along with reform, total federal student loans would be capped at $60,000/student (outstanding & discharged) except for those in existing programs as of a certain date.

States could provide student loans if they don't wish to participate in reform.

New money Parent Plus loans would no longer be issued.

AI USE

Subject to state law, and hopefully starting in 2027, most primary doctoring, psychiatry and medical image analysis would be replaced with AI.

Health care cost coverage for a human doctor would still apply to: 1. confirm AI diagnosis, 2. prescribe ionizing radiation imaging/treatment, 3. prescribe addictive/psychotropic/voucher/government co-pay drugs.

Doctors could still operate on a private pay basis.

TOPICS: AMERICA - The Right Way!!; Business/Economy; Education; Health/Medicine

KEYWORDS: emtala; healthcare; medicaid; ppaca

To: Brian Griffin

No. Don’t rationalize it. Get rid of it and all other government participation in “healthcare” and insurance. It’s none of the governments proper business.

2

posted on

11/04/2025 5:42:25 AM PST

by

arthurus

(l| covfeve |l -|\)

To: arthurus

“Get rid of it”

What you want isn’t going to happen.

Leftists now get about 2/3rds of the taxable income and they feel they should get something they want for their taxes.

“It’s none of the governments proper business.”

Patents issued under ARTICLE I, SECTION 8 allow drugs to be priced out of the reach of many individuals.

Preexisting condition is generally another way of saying regular consumption of expensive prescription drugs.

To: Brian Griffin

I still say a personal Healthcare investment plan, with a $2 million limit to the savings, that can be withdrawn for medical purposes tax free, is best.

4

posted on

11/04/2025 6:11:12 AM PST

by

Jonty30

(I've been diagnosed as being polemic and there is no cure. )

To: Jonty30

“I still say a personal Healthcare investment plan, with a $2 million limit to the savings, that can be withdrawn for medical purposes tax free, is best.”

You probably live in a similar plan with a limit of around $400,000. It probably has lots of plywood and 2x4s.

To: Jonty30

“$2 million limit”

You would need a $600,000/year doctor and round the clock nurses fawning over you for two years?

To: Brian Griffin

Put it back into the market.

7

posted on

11/04/2025 6:24:18 AM PST

by

arthurus

(l| covfeve |l )

To: Brian Griffin

I. N. O.

Insurance in Name Only

All scam

Stock Market - Banking

All scam. ✖️

8

posted on

11/04/2025 6:27:26 AM PST

by

Varsity Flight

( "War by 🙏 the prophesies set before you." ) I Timothy 1:18. Nazarite warriors. 10.5.6.5 These Days)

To: Brian Griffin

75% of healthcare costs are in the last 6 months of one’s life, so you will probably not outlive your savings if you plan carefully.

9

posted on

11/04/2025 6:33:46 AM PST

by

Jonty30

(I've been diagnosed as being polemic and there is no cure. )

To: Brian Griffin

None of these programs are in Article I, Section 8, nor in any Amendment.

Get govt out of all wealth-transfer activities.

Student loans (especially) should be entirely privately-sourced. Force the schools to underwrite the loans from their endowments.

10

posted on

11/04/2025 8:20:18 AM PST

by

castlebrew

(Gun Control means hitting here you're aiming!))

To: Brian Griffin

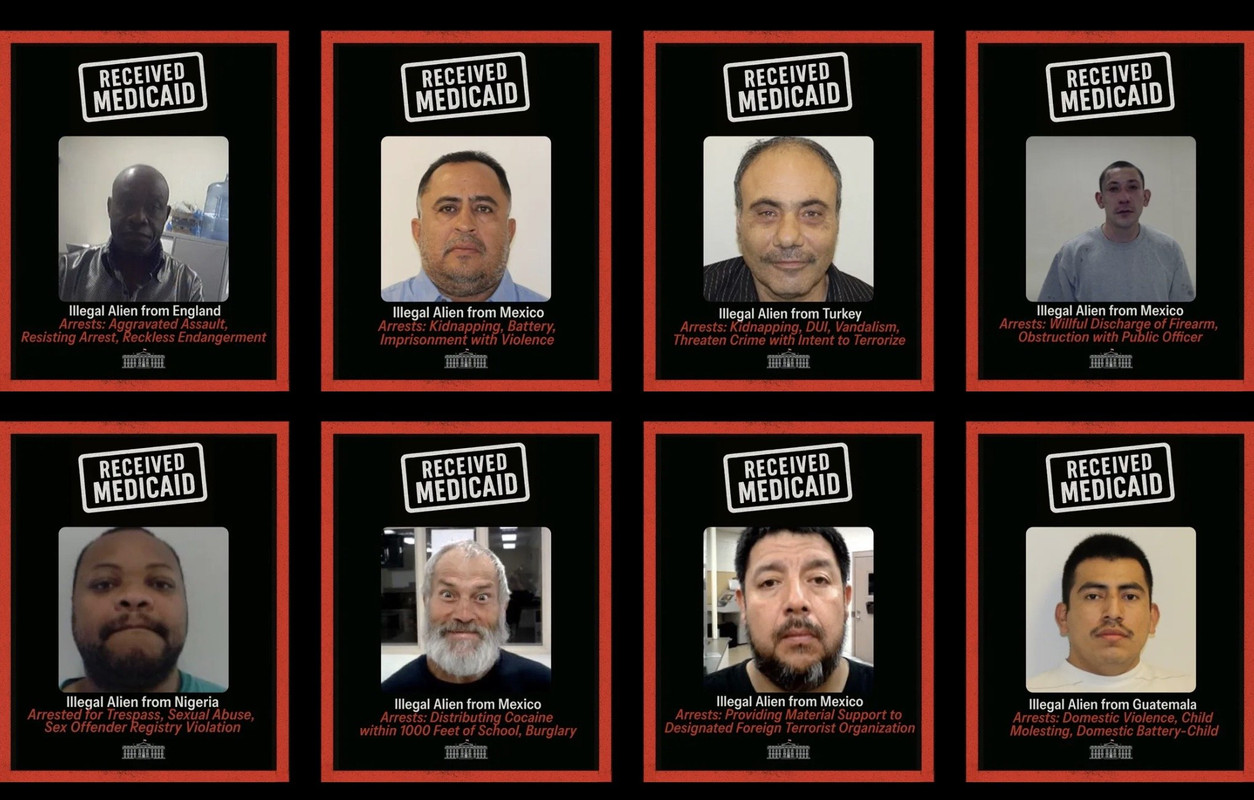

Lots of fraud in medicaid, with plenty of illegals accessing the system:

"The Trump administration has intensified enforcement against criminal illegal aliens receiving taxpayer-funded Medicaid benefits, arresting hundreds of unauthorized individuals since taking office, including those with serious criminal records who exploited taxpayer-funded Medicaid illegally or through loopholes."

More here:

https://www.thegatewaypundit.com/2025/11/president-trump-launches-explosive-new-website-expose-illegal/

11

posted on

11/04/2025 8:54:03 AM PST

by

Bon of Babble

(You Say You Want a Revolution?)

To: castlebrew

“Student loans (especially) should be entirely privately-sourced.”

Feel free to try to make that happen.

“Force the schools to underwrite the loans from their endowments.”

Many private schools have such large endowments they could eliminate tuition.

State universities don’t generally have huge endowments.

To: castlebrew

“None of these programs are in Article I, Section 8, nor in any Amendment.”

One could argue that the PPACA was “necessary and proper” to respond to the problems of expensive drugs caused by the power of “securing [by patent] for limited times to...inventors the exclusive right to their...discoveries.”

San Francisco is a leading drug development center. Can you name its Congresswoman who rammed the PPACA through?

The enumerated powers themselves such as creating patents don’t have to be exercised in a “necessary and proper” fashion, such as requiring patented drugs to be individually affordable.

Yup, you are losing freedom, your money and the country you probably love over a bunch of chemicals!

ARTICLE IV. SECTION 3. paragraph 2:

“The Congress shall have power to dispose of and make all needful rules and regulations respecting the territory or other property belonging to the United States...”

To: Jonty30

“75% of healthcare costs are in the last 6 months of one’s life”

Many of the drugs you see advertised on TV cost about as much as a car, every year.

“pre-existing conditions” ~= conditions treated with expensive drugs treated with expensive drugs on a multi-year basis

Disclaimer:

Opinions posted on Free Republic are those of the individual

posters and do not necessarily represent the opinion of Free Republic or its

management. All materials posted herein are protected by copyright law and the

exemption for fair use of copyrighted works.

FreeRepublic.com is powered by software copyright 2000-2008 John Robinson