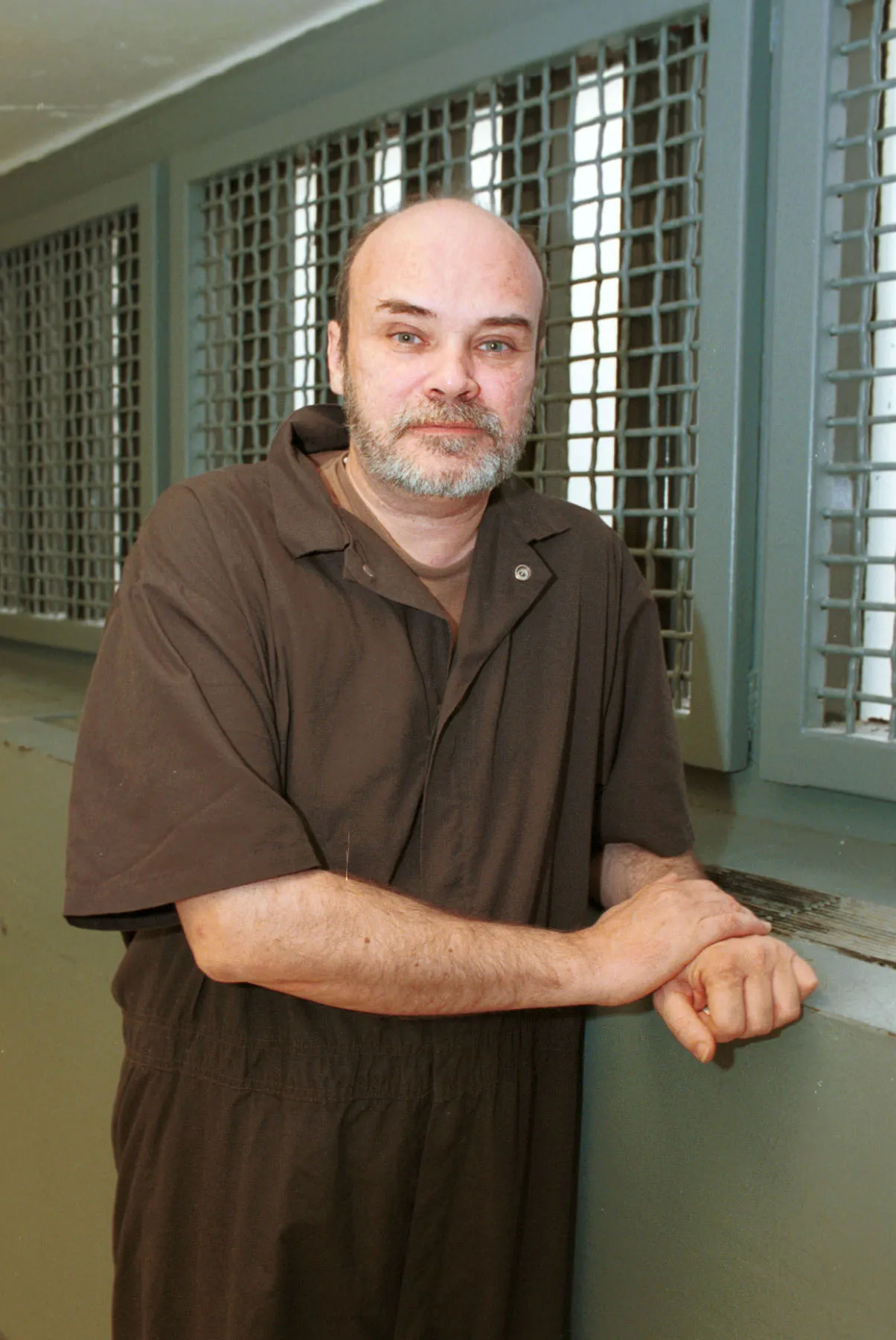

I only went bankrupt three times. The last time I hid my ponzi scheme skimmings so that those that got scammed would never see their assets back. As a side benefit, Uncle Sam gave me eleven years free room and boards. Even new outfits like this one!

Posted on 03/17/2025 7:18:41 AM PDT by delta7

American households have been unable to pay off their debts. The Federal Reserve Bank of New York recently reported that household debt has reached a new all-time high at $18.04 TRILLION.

Americans acquired an additional $93 billion in outstanding payments during Q4 of 2024, with half of this debt finding its way onto high interest credit cards. Credit card debt has also reached a record high at $1.21 trillion. I reported in January that credit card defaults his a 14-year high after skyrocketing by 50% in a one-year period.

Donald Trump said during his campaign that he would like to cap credit card interest fees at 10%, perhaps for a temporary period. There are now bipartisan calls for companies to lower fees, with Congresswomen like AOC and Anna Paulina Luna both championing a 10% credit card cap.

Prior to the pandemic, Americans paid $120 billion annually in credit card interest fees from 2018 to 2020, amounting to $1,000 annually per household. In 2022, consumers were paying $105 billion in interest as it has become the main cost behind having a credit card. Rates on credit cards have doubled in a mere decade from 12.9% in 2013 to 22.8% in 2023.

US Household Debt

The Federal Reserve Bank of New York’s February 2025 Survey of Consumer Expectations also found that Americans are highly concerned about missing payments, falling into delinquency, or losing their livelihoods. Consumers foresee inflation spreading across the board. In February 2026, the general public believes gas will rise by 3.7%, food by 5.1%, rentals by 6.7%, and medical costs by 7.2%.

Then, around 14.6% of Americans said they believed they would miss a minimum debt payment over the next three months. Americans have not expressed this much concern about missing payments since the early pandemic days of April 2020, when the mainstream media insisted the world was coming to an end.

Aggregate delinquency rates rose 0.1% over a one-quarter period. Mortgage balances increased by $11 billion, hitting $12.6 trillion by December 2024. When choosing between home or auto payments, consumers are prioritizing shelter. Auto loan balances also experienced an $11 billion increase, rising to $1.66 trillion in Q4 2024, but serious delinquencies on auto payments have risen substantially.

Student loan balances increased by $9 billion, and now sit at $1.62 trillion. Students who once thought their loan debt would be forgiven have been notified that their future social security payments will be garnished by the government if they fail to pay.

Most households are a few missed payments away from financial ruin. In fact, 47%, nearly half, of American households currently live paycheck to paycheck. Americans are in an extremely delicate financial situation right now, and this looming debt crisis will not disappear.

It was me.

My bad.

I just kept getting all these offers in the mail.

“what we need is a divine Jubilee year…”

Yesterday you were posting that that would only happen after the destruction of the US and you were cheering for our destruction.

Decades of wage suppression policies plus inflation and this is the result.

Most jobs do not pay nearly enough to support a family.

But I'm of the mindset that even if someone does like I'm doing, don't count yourself wealthy enough to retire unless your investments are more than enough to pay off the mortgage at any given moment should things between you and the bank go sour. Don't count that portion of your investments as what you'll live on in retirement.

Americans *would not* be $18,000,000,000,000 in debt if the US and then the world did not go off the Gold Standard in 1971. Nixon gets the blame but it was actually Johnson a few years earlier by eliminating the backing of federal reserve notes (money) by gold, that killed the gold standard.

Living via various debt instruments has become the normal order of business, to the detriment of real people the world over. Business & industry are similarly burdened.

Govt’s everywhere borrow and kick the can down the road, a road with a finite length.

People used to save their money for purchases or use lay-away, Christmas savings accounts. Now it’s charge, charge, charge.

There’s a whole class of people who routinely drive themselves into the financial ditch, then use the bankruptcy courts to dissipate their legally incurred debt.

Do we even need to rehash about the millions living off others via the gov’t free money system?

It’s pretty simple. Solvent people use and manage debt wisely. Those underwater use it as extra income...for a while.

You have the Gator following everywhere and obsessing. Let the poor girl get some rest lol

I only went bankrupt three times. The last time I hid my ponzi scheme skimmings so that those that got scammed would never see their assets back. As a side benefit, Uncle Sam gave me eleven years free room and boards. Even new outfits like this one!

Gemini, where did Martin Armstrong hide his assets?

Based on the information available, the matter of where Martin Armstrong “hid” money is complex and involves these points:

* Financial Fraud:

* Armstrong was involved in financial fraud, where he misused investor funds.

* Specifically, he sold “Princeton Notes” and promised to invest the proceeds in segregated accounts, but instead, he commingled the money.

* Hidden Assets:

* There were accusations and legal proceedings concerning his attempts to hide assets from regulators.

* One specific instance involved rare coins, that he claimed to have hidden in his mothers house.

* The case of the rare coins, shows that he did hide assets, in places that were not traditional financial institutions.

* Legal Proceedings:

* Legal proceedings aimed to recover and distribute the defrauded funds to investors.

Therefore, it’s not a simple case of a single location. It involved misuse of investment funds and attempts to conceal assets in various ways.

Gemini, How much money did Martin Armstrong lose?

Based on the information available, determining the precise amount of money Martin Armstrong lost is complex, as various sources cite different figures. However, here’s a summary of the key points:

* Losses from Risky Trading:

* It’s reported that Armstrong incurred substantial losses through risky trading, particularly involving bets on the Japanese yen. Sources indicate these losses reached “hundreds of millions of dollars.”

* Fraud and Restitution:

* Accusations and legal actions centered on allegations of defrauding Japanese investors. Reports indicate that the fraud involved over $700 million.

* There are also reports that investor losses approached or exceeded $1 billion.

* Also that Republic Securities paid approximately $569 million in restitution to victims.

* CFTC Action:

* The U.S. Commodity Futures Trading Commission (CFTC) obtained orders for over $27 million in remaining restitution.

Therefore, while a single, definitive figure is elusive, it’s clear that the financial losses associated with Martin Armstrong’s actions were very large, reaching into the hundreds of millions, and potentially exceeding $1 billion.

“You have the Gator following everywhere and obsessing. Let the poor girl get some rest lol”

Just curious. Why are you siding with a convicted scammer that is here only to find suckers stupid enough to send him money?

Trump’s fault. I just know it...

You have the Gator following everywhere and obsessing. Let the poor girl get some rest lol

————

Txgator’s head is exploding as Armstrong’s forecasts became reality, his podcasts and news blogs are now off the charts.

Posters like Gator usually get suspended for awhile ( he already has), or they go insane. No one listens to him, he is amusement.

“as Armstrong’s forecasts became reality”

So how is that forecast working out where you predicted a US civil war will start January 2025?

Armstrong Mar. 10, 2025: “This is the only fully functioning Artificial Intelligence Computer with more than a 40-year track record.”

And during that 40 year period of using Socrates Armstrong wen bankrupt three times, lost up to a $billion of clients’ funds and spent eleveneven years in the federal pen convicted of securities fraud.

“Txgator’s head is exploding as Armstrong’s forecasts became reality, his podcasts and news blogs are now off the charts.”

Your support seems to be dropping. Only one sad IATG from Kiryandyl till a couple of posts from citizen today.

I suspect he will not hang around long.

The five or six that you think are your supporters are actually trolling me fir something from ten years ago.

Now that they know what a slime character Armstrong is they have deserted your threads.

The five or six that you think are your supporters are actually trolling me for something from ten years ago.

————

You are guilty of the same, trying continuously to smear Martin Armstrong a legendary forecaster for an injustice by the New York “ justice “ system to him 25 years ago…..ask President Trump about the NY court system.

In any case, your smearing is not working, Martin Armstrong is now one of the most sought after guest speakers worldwide.

Your hate is on display, do remember, hate is destroying you. Carry on.

“You are guilty of the same, trying continuously to smear Martin Armstrong a legendary forecaster for an injustice by the New York “ justice “ system to him 25 years ago…..ask President Trump about the NY court system.”

ROTFLMAO! ARMSTRONG left a damning paper trail and pleaded guilty. The case was rock solid against him.

From in or about 1992 to in or about

1999, MARTIN A. ARMSTRONG received account

statements, first from Prudential and later from

Republic Securities, for each of the PGM accounts.

ARMSTRONG manufactured his own version of PGM account

statements for the investors, which he generally sent

to Cresvale-Tokyo to convert into a Japanese format

and forward to the Japanese investors. In the

account statements he prepared, ARMSTRONG misled the

investors by failing to disclose the actual trading

losses in their accounts, misrepresenting the net

asset value of their accounts, and in some instances

by providing account statements for accounts that he

never opened, having instead transferred the

investors’ money directly into a PEIL operating

account, or to another investor to repay that

investor’s Note. In addition, the account statements

ARMSTRONG manufactured and caused to be sent to the

investors falsely represented that he was entitled to

millions of dollars in management fees and

performance fees to which, as he well knew, he was not entitled in light of his dismal trading

performance and the shrinking value of the Investor

accounts.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.