Sounds as if all the donations to the DNC by the bank and its customers is about to give them some serious returns.

Ah, more of the Deconstructing of America. Brought to you by the Marxist Socialists of AmeriKa.

I don’t wanna ‘backstop’ a damned thing, especially some overcharging SV tech company that put its money there to pay a bunch of pampered leftist employees. The ‘government’ does’nt ‘backstop’ anything. The American taxpayer does.

Lot of people believe that bulk of account money (maybe up to 50 to 60 percent) is still existing, but with legal action....it could be two to three years to get that money back. For companies to survive and continue paying employees...they’d need cash flow.

I would imagine some type of massive Biden push...to loan 50-percent of value out, until these people get the final pay-off will occur (figure in the $100-billion range).

For the little guy, figure they will get their $250k very shortly.

A lot of this money is tied into fed bonds....paying at a crappy rate unlike the recent bonds which were much better rate.

“But the majority of deposits at SVB were not insured...”

************

Taxpayers will cover them. Just watch what happens.

The government will bail out the depositors which will guarantee that we will have more of the same nonsense.

It appears the “powers that be” have been deliberately trying to pump up the value of the bank’s stock over the past couple of months, so they could bail out and leave the poor retail investors holding the bag. This happens often so always be wary if suddenly you see all financial reporters suddenly touting the value of a stock. They will encourage people to buy the stock and push the price up only to bail just before the bad news is revealed. I’ve seen it happen often. The classic “pump and dump”.

FDIC’s systemic risk exception tool

But although the FDIC will be responsible for administering such a program, the

maximum amount of outstanding debt that can be guaranteed is to be determined not

by the FDIC but by the Secretary of the Treasury in consultation with the President.

And, in a significant addition, the law also requires the program to have congressional

approval in the form of a joint resolution—a requirement that essentially means

Congress must pass the equivalent of a law before the program can go forward.59 So

although Dodd-Frank provides for a program similar to the DGP, the law’s requirement

for wider political consent through congressional approval (even though the approval

would have to be considered on an expedited basis) could limit regulators’ flexibility

during a future financial crisis.

Interesting if followed..............................

This is one of those very rare occasions where the lefties have a unique insight that we don’t, they have a popular pejorative, “corporations privatize profits and socialize losses”.

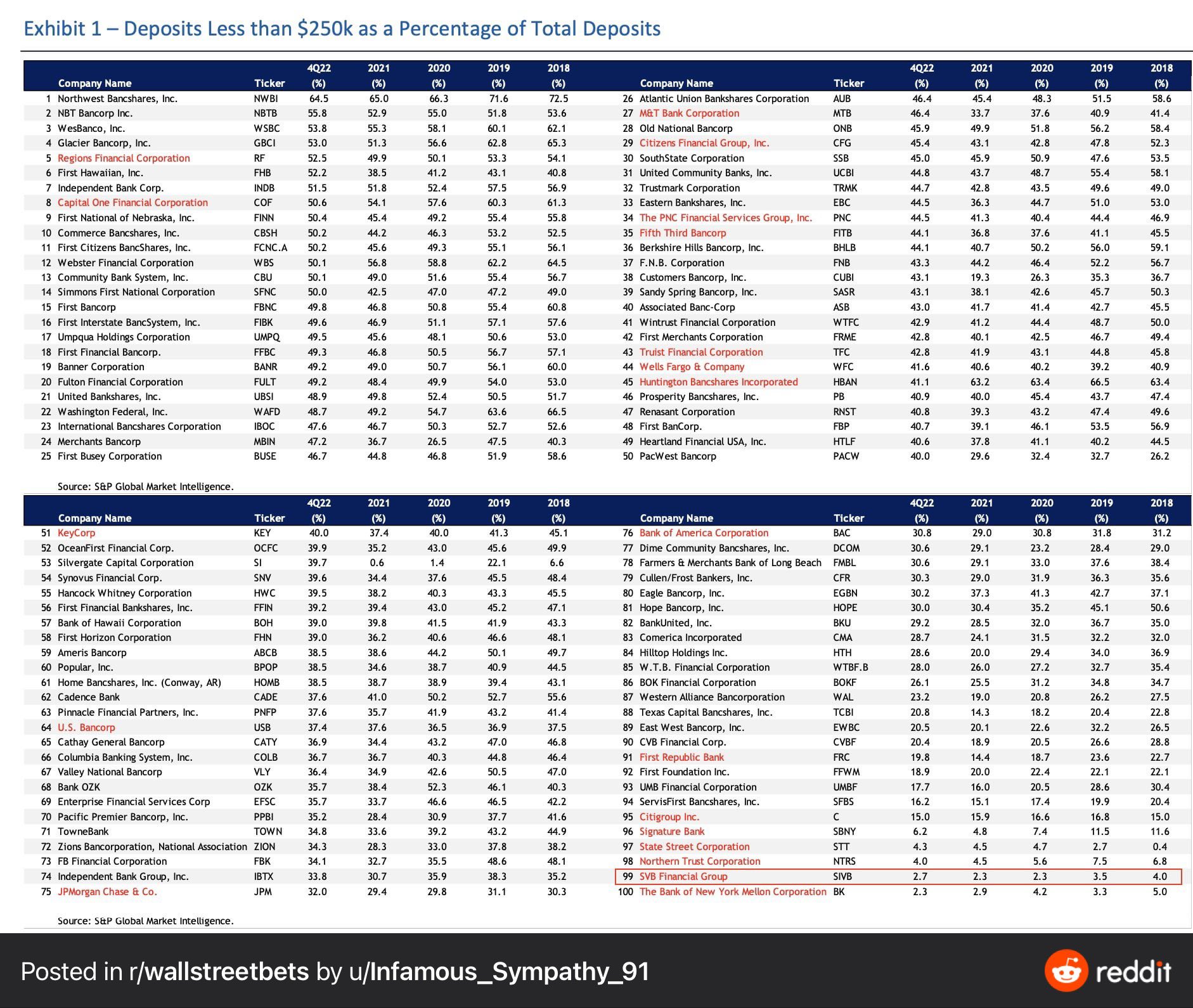

At the end of last year, SVB had more than $175 billion in deposits — and $209 billion in total assets. Unless that filing was a fraud, the bank is illiquid but not insolvent. Assuming competence on the part of federal banking authorities, It is quite possible that no one but the bank stock owners will lose any money. I am predicting that all depositors will recover over 90% of their money.

So, it’ll be the old “we’ll take your bank funds to make up for the idiocy of other folks?

You’ve gotta love liberals (when they are being led to the guillotine).

I hear it was a favorite bank by liberals...

Otherwise known as quantitative easing.

We all feel for her tearful situation.😭

Her estimated new worth two years ago was 2.5 Billion Dollars.

If she loses a portion she will be back to picking up returnable bottles and cans for deposit money. And selling used wheel covers at her old stand.

Lookner coming up

Now on Rumble video

Silicon Valley Bank Collapse: Government Action Today? - LIVE Breaking News Coverage

https://rumble.com/v2ctw5w-silicon-valley-bank-collapse-government-action-today-live-breaking-news-cov.html

The problem with SVB is not that they dealt with their clients fraudulently, but that their risk management was awful.

But Congress and the free spending Biden administration are ULTIMATELY the culprit here.

It’s all an extension of Fed policy to curb inflation, reversing a 13-year zero-rate policy. And why did inflation occur? Isn’t it because of the massive increase in government spending, which resulted in huge printing of money ?

This of course pushed up rates in the middle and right side of the yield curve, devaluing existing bond holdings locked into older rate patterns. Investors noticed and then depositors too. The high-flying institution that specialized in providing liquidity in industries that have lost their luster suddenly found itself very vulnerable.

In addition, the SVB and probably other banks were exposed with a portfolio of collateralized mortgage obligations and mortgage-backed securities. But with rates rising, those are coming under stress too as high leverage in housing and real estate become untenable amidst falling valuations. Borrowers are finding themselves under water and that in turn adds to stress on lenders.

And where did SVB, and the entire banking industry, get the funds to bulk up their portfolios with such debt holdings? You guessed it: STIMULUS PAYMENTS!’

Hundreds of Billions flooded in and it had to be parked somewhere making some return. At the time it seemed like a good deal, until Fed policy changed.

Immense government spending which produced debt that was quickly monetized and eventually caused inflation, prompting the Fed to reverse course with the largest/fastest rate increases in history. And guess what? IT’s STILL GOING ON!

This destabilized (or restabilized) production structures away from the right side of the yield curve toward the left, shifting capital in search of return to the consumer-goods sector. Labor has begun to follow, thus creating a surplus of resources in information tech and a shortage in retails.

It was always naïve to think that this shift would take place without touching the banking institutions that shoveled leverage in the direction of industries that thrived during lockdowns but are cutting back massively.