Posted on 02/11/2023 9:05:50 PM PST by SeekAndFind

Ugliness awaits most boomers nearing retirement, not only have they been lied to, but they also have to deal with rigged markets, corruption, and incompetent advisors. Boomers make up the second-largest generation in American history, it consists of over 72 million individuals. Those that haven't already retired are getting ready to. A big problem is most have little in the way of savings.

Adding to this problem is that the generations following the baby boomer generation are even worse off and America's economic picture is less than rosy. It does not help that Americans have been encouraged over the years to spend and incur debt rather than save. This encouragement comes from politicians hooked on the idea consumer spending creates a strong economy.

This results in many people retiring with little savings and dependent on a government already deep in debt to care for them in their older years. Those of us that have studied the numbers come to shaking our heads in horror, simply put, something has to give and most likely promises will be broken, When words like unsustainable and insolvent have been muttered they simply get brushed aside by daily life.

For years those in power have hidden and sheltered Americans from the harsh truth that the numbers simply do not work but history shows politicians would rather kick the can down the road than deal with reality. To the many people that have been looking forward to a comfortable and leisurely life in their older years. The fact that things could be worse is not something that will cause most retirees to leap with joy.

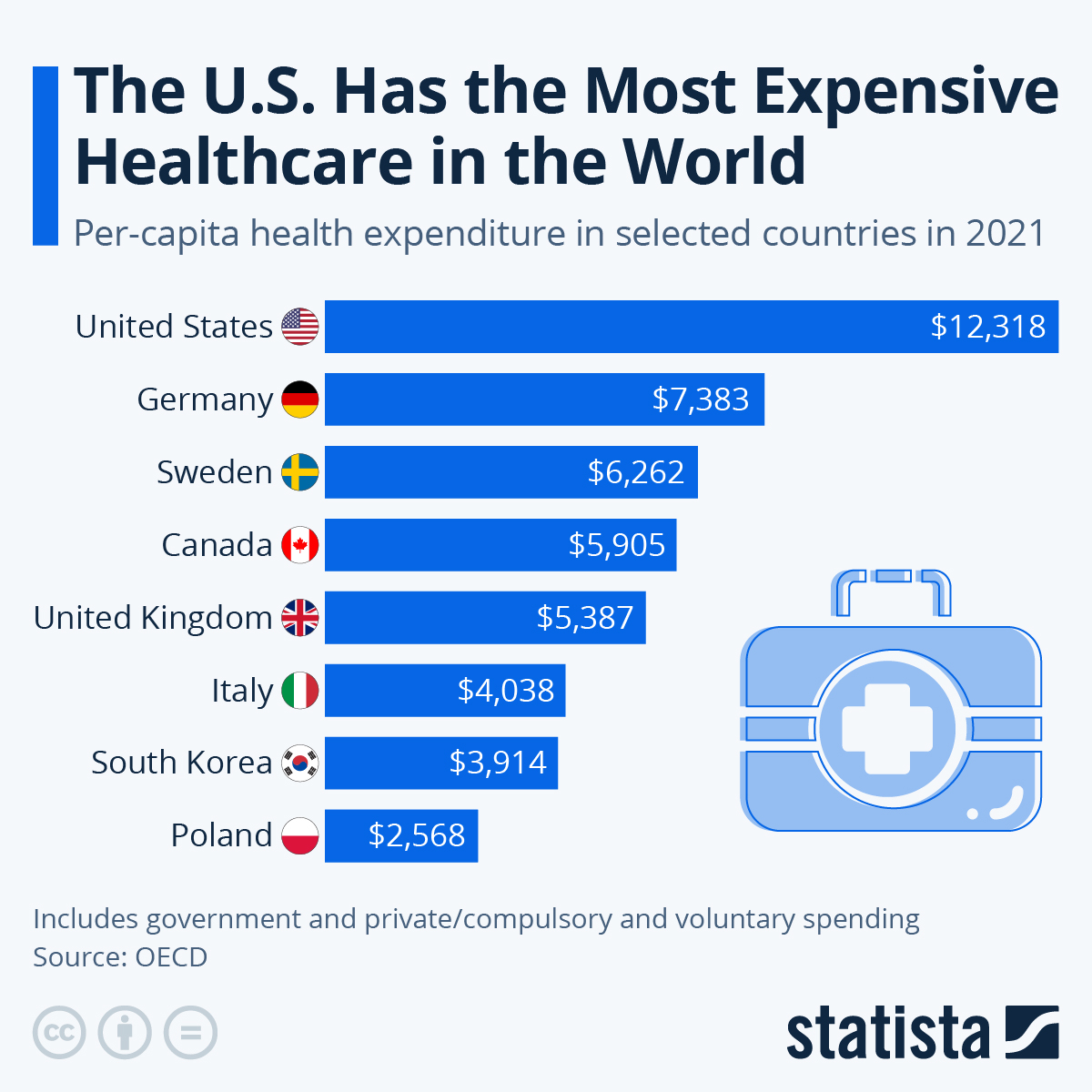

An example of what we face is evident in healthcare. this is a sector of the economy that Washington has pledged to fix and even claimed it has. The chart put out by Statista shows the U.S. has the most expensive healthcare system in the world.

You will find more infographics at Statista

This matters if you consider it as a tax on the American people and realize that healthcare is a major expense for people as they age. This hits medicare directly in the heart meaning as cost soar for the program something will have to be done. That something generally comes in the form of cutting benefits and charging recipients more.

While there is more to life than money, few people choose to live in poverty. Unfortunately, even most Americans that have saved over their lifetime and done the right thing are in peril.

Over the years, the Fed has inflated the money supply and in doing so it also inflated asset prices, including stocks, bonds, and real estate. Much of this is the result of ballooning debt. Make no mistake about it, the government has fed at the debt trough and it has made our future less promising. Yes, we are roughly 33 trillion in debt, not counting the unfunded liabilities of social security, medicare, and Medicaid.

While This Is An older Chart, Little Has Changed. Reality Is Not Pretty

With the current trajectory of economic policies and inflation running above the return savers can earn from safe investments things will only get worse for retirees and those close to retirement age. Considering the amount of debt already amassed, the government is going to have a difficult time putting together generous new aid packages to come to the aid of those dependent upon its programs. This will result in conflict as both the young and the old are forced to fight over the few scraps it can provide.

All this has created a situation where if the money supply now contracts a huge number of defaults will occur and both businesses and investors will incur big losses. This threat to 401Ks and pension plans is real and would make many boomers collateral damage in any effort they make to correct the mess they have created. Those in or nearing retirement should make an extra effort to reduce risk and keep their savings safe.

They back-tested different portfolios over a 30 period starting with 1925, then starting in 1926 for 30 years, then 1927... and so on and on until 1965 (the 30 year period ending in 1995). The paper was published in 1998.

Each portfolio was analyzed with different withdrawal rates an asset allocations in order to find the optimal portfolio that would last for 30 years. Nobody questions the results of the study, only whether the 4% rule is the best way to manage one's retirement portfolio.

-PJ

My impression of 20 plus FR years is most are affluent, where most is defined as 51%, not 90.

I will answer that.

The Trinity study is very real, very good and one of the most influential papers in the field of retirement planning. Philip L. Cooley, Carl M. Hubbard and Daniel T. Walz authored an early paper, Retirement Savings: Choosing a Withdrawal Rate That Is Sustainable. (AAII Journal February 1998, Volume XX, No. 2). Because the authors were professors at Trinity University in San Antonio, Texas, it is often referred to as "the Trinity study." The authors studied actual historical stock and bond returns from 1926 through 1995 to determine sustainable withdrawal rates.

There is no WAG involved.

In 2011 Cooley, Hubbard and Walz updated their numbers. It was Published in the Journal of Financial Planning under the title "Portfolio success Rates: Where to Draw the Line.

I prefer the Updated Trinity Study because it has more data, and because it analyzes both inflation adjusted and non adjusted withdrawal rates.

One of the big steps Trump had taken to help with that was to make it so that hospitals and doctors would have to publish rates for many standard procedures. Price transparency would have, over time, led to lower prices.

Lots of stories like this out there:

https://www.foxnews.com/politics/trump-signs-executive-order-calling-for-upfront-disclosure-of-hospital-costs

Not sure if this EO is still operative, or if Biden has reversed it.

https://www.researchgate.net/publication/358832846_Can_BRICS_De-dollarize_the_Global_Financial_SystemAbstract

Existing scholarship has not systematically examined BRICS (Brazil-Russia-India-China-South Africa) as a rising power de-dollarization coalition, despite the group developing multiple de-dollarization initiatives to reduce currency risk and bypass US sanctions. To fill this gap, this study develops a 'Pathways to De-dollarization' framework and applies it to analyze the institutional and market mechanisms that BRICS countries have created at the BRICS, sub-BRICS, and BRICS Plus levels. This framework identifies the leaders and followers of the BRICS de-dollarization coalition, assesses its robustness, and discerns how BRICS mobilizes other stakeholders. The authors employ process tracing, content analysis, semi-structured interviews, archival research, and statistical analysis of quantitative market data to analyze BRICS activities during 2009-2021. They find that BRICS' coalitional de-dollarization initiatives have established critical infrastructure for a prospective alternative nondollar global financial system. This title is also available as Open Access on Cambridge Core.

Care to speculate on Biden's efforts to destroy our economy with the possible intent of enabling this to happen?

The reason I am asking is that I am wondering if these egghead professors have ever heard of the IRS and their:

Required minimum distributions (RMDs)If you’ve reached age 73, it’s time to start withdrawals—the IRS requires you to begin taking Required Minimum Distributions (RMDs) from your IRA and workplace retirement accounts every year. That’ll mean new income that’s taxable, with stiff IRS penalties for not taking it on time.

A retired person does not have control of their mandatory withdrawals. I believe the RMD is calculated by dividing your total investments by your life expectancy factor.

I'll take a deep breath now, as I did some quick figuring and hopefully, by the time I get there, my withdrawal might be close to your 4%. Now tell me the truth, did the 4% come from the IRS?

health? yea, sure!

what started with slight osteo moved around to colorectal cancer, then moved around to congenital heart disease, which has moved around to kidney dialysis and all that fun!

hey, it beats the alternative!!

And I can’t figure out what all of these people are doing to be able to afford such a lifestyle. Of course, in many cases they’re only pretending to afford it by overextending themselves and living on credit. With the economic shakeout beginning, I guess we’ll find out soon how many are only pretenders.

On the other hand, what fool is going to entrust his money to the BRICS?

Brazil - neo-Marxist and convicted felon President.

Russia - completely wiped out its oil and gas sovereign wealth fund fighting Ukraine, and the President is a former KGB Colonel.

India - pro-business Prime Minister in a Third World country with a per capita GDP of $2,500!

China - governed by the totalitarian Chinese Communist Party.

South Africa - President is openly Marxist.

No one is going to entrust their money to that Pirate ship!

That's a very good point.

Except that's what life is for the most part. What else could it be?

As a young man told Jordan Peterson, "I would like to quit my job and move to a Caribbean island and sip on margaritas all day lounging on the beach."

Peterson said to him, "after 3 days of that you're badly hung-over and sunburned as hell...then what are you going to do?"

What Peterson suggested was, as long as you have to work, wrangle yourself into a kind of work you enjoy. Then at least you won't be completely miserable.

I also read somewhere else that life is a boot camp...preparing our souls for eternity.

As an older man now, I can say that though I am still an idiot, I am a much wiser idiot than I was when I was a young man.

Bottom line: If we think we have been swindled and that life sucks, perhaps we have the wrong idea about life. Maybe the purpose of life isn't happiness, pleasure, and security. Perhaps it is "growth of character and the accumulation of wisdom."

The happiest campers seem to be the ones who are busiest. They are busy repairing their worn out campers and trucks, grilling, working on lap-tops (presumably in the gig economy), or hiking up on the trails with their friendly (old) dogs.

The wealthier campers don't seem to smile a lot and are considerably less friendly...particularly the wives.;-)

I am retired now.

What I learned from my working years is that:

...it’s not so much about what you are having to do,

it’s about who you are having to do it with.

That’s true...unless you are an introvert.;-)

Nothing in life is free Owen. It’s just about understanding who pays.

That warm feeling you get when someone gets a “vax”? You may think that feeling was free.... but someone paid for it.

this is how I feel....we’ve been “swindled....go to school, marry, raise children well, and work, work, work, and don’t forget to volunteer and invest in good growth mutual funds and you’ll be set....or not....”

It may be best to go back to the old days where one worked till they died or they moved in with a younger family member to be supported by them in exchange for doing some work they were able to do around the house.

Bkmk

But yet most of these same people you say are not stupid still vote absentee for democrats to this day.

The euro was invented to reflect the reality that the governments of the states of Western Europe had voluntarily formed the “Greater Germany” of Hitler’s dreams and they needed to unify the economies (which for the most part they did; only a few outliers, such as Germany’s opponent Britan, didn’t convert to the new “national currency of the EU, signaling years ago that they weren’t very committed to German dominance of the new country formed). Because the euro included many countries in worse shape than Germany, it was unlikely that it would replace the US$ as the de facto currency of global trade - and it hasn’t.

They should have thought for themselves.

I'm 64 and admittedly, didn't get serious about saving for retirement until about 20 years ago.

It's never too late to right a wrong, though. People who get caught up in selfish endeavors (buying what they want when they want) should pay that price and not assume I'm going to bail them out.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.