Skip to comments.

Can I retire on $500K?

Me

| 8/19/2019

| Me

Posted on 08/19/2019 9:03:32 AM PDT by freedumb2003

Can I retire on $500K?

Soon to be ex-wife and I had the last of all our blow-outs. 25 years married, no kids, own the house outright, $1.7 MM (maybe 2), zero debt, 60-something.

Reached out to Cordell Cordell the only law firm I know of that will take care of the man side of things.

soon to be ex-wife does not work.

TOPICS: Chit/Chat

KEYWORDS: retire; retirement

Navigation: use the links below to view more comments.

first previous 1-20 ... 41-60, 61-80, 81-100 ... 221-228 next last

To: freedumb2003

You have to run the divorce proceedings gauntlet to reach the other side.

You have the means to live life on your own terms if you manage properly and don’t blow your money on coke and hookers.

Going Jimmy Buffett is easy as long as you pace yourself.

If I were suddenly on my own, I would definitely sell the house and everything in it, trade in the cars for a Class B van RV and never look back. I could easily do that just on my retirement income alone.

Good luck with whatever choices you make.

61

posted on

08/19/2019 9:45:25 AM PDT

by

TADSLOS

(You know why you can enjoy a day at the Zoo? Because walls work.)

To: angelrod

The only advice I would give is do not take social security early!I really disagree with this advice. I started drawing at 62. I invest it, earning about 5% a year. I'm way ahead of where (almost twice) I'd be if I waited to 65 or 70.

Plus, since the world will end in 11 years, I'm in an infinitely better position.

62

posted on

08/19/2019 9:45:47 AM PDT

by

FatherofFive

(Islam is EVIL and needs to be eradicated)

To: freedumb2003

” I walk away with $500 clear....” Yup, you may be lucky to keep five hundred dollars. LOL! We did okay on $300K. But it’s gone now due to stoopidness but we’re okay. Enjoy your retirement.

63

posted on

08/19/2019 9:47:11 AM PDT

by

rktman

( #My2ndAmend! ----- Enlisted in the Navy in '67 to protect folks rights to strip my rights. WTH?)

To: angelrod

The only advice I would give is do not take social security early! It’s a big difference between taking it early, at full time etirement age or even taking it at 70 would give u 20-30% more than taking it early.That depends on how long you expect to live. Ask a financial planner to run the numbers on how long you have to live to recoup the foregone benefits in early retirement with taxes and inflation taken into account. There are no guarantees either way. If you don't need the cash flow from Social Security early retirement benefits, go ahead and delay … or consider taking the benefits and investing them appropriately. There's a lot to be said for cash in hand, especially since Social Security is unsustainable and means-testing of benefits and/or hidden changes in the benefit structure (e.g. changes in the COLA or discrete nudges to the income replacement rate) may well be in the future.

64

posted on

08/19/2019 9:48:05 AM PDT

by

sphinx

To: freedumb2003

Yes, if you eat catfood and saltines.

65

posted on

08/19/2019 9:48:58 AM PDT

by

Carriage Hill

(A society grows great when old men plant trees, in whose shade they know they will never sit.)

To: freedumb2003

Consider yourself blessed! I retired last year with next to nothing (long story) but have been able to “get by” until recently and I still have a mortgage. Just went back to work part-time in order to pay for Medicare supplemental insurance and also a year long penalty I have to pay for taking 401-k money our in wrong year. DO NOT take any money our or make big money 2 years before you retire or you will pay a penalty. Stayed on phone a while the other day trying to get out of it, but no go. If I’d taken the money out in the previous year there would have been no penalty. Don’t ever let anyone tell you Medicare is free...lol

66

posted on

08/19/2019 9:49:50 AM PDT

by

BamaBelle

(The storm has arrived!)

To: Mariner

And, she and her new boyfriend will be happy as clams living off her alimony. She probably knows not to derail the gravy train by getting remarried.

67

posted on

08/19/2019 9:50:22 AM PDT

by

rktman

( #My2ndAmend! ----- Enlisted in the Navy in '67 to protect folks rights to strip my rights. WTH?)

To: FatherofFive

I agree with you on this one. I will not draw SS until I am 65 and/or done working full time, but strongly believe that a person should start taking SS BEFORE they start using up their own money/savings for retirement living expenses.

If a person dies before getting SS, but has been spending their own retirement savings for several years, they have spent money that could have passed to their kids and gotten ZERO from SS.

If a person starts taking SS and gets $2,200 per month, then supplements with their own savings money, in 5 years, they will have gotten $132,000 from SS (and saved $132,000 of their own money, everything being equal). What is the income differential by waiting 5 years? How long until you make up the $132,000?

May not be the best option for everyone, but certainly is something to think about.

68

posted on

08/19/2019 9:54:40 AM PDT

by

NEMDF

To: freedumb2003

Consider yourself blessed! I retired last year with next to nothing (long story) but have been able to “get by” until recently and I still have a mortgage. Just went back to work part-time in order to pay for Medicare supplemental insurance and also a year long penalty I have to pay for taking 401-k money out in wrong year. DO NOT take any money out or make big money 2 years before you retire or you will pay a penalty. Stayed on phone a while the other day trying to get out of it, but no go. If I’d taken the money out in the previous year there would have been no penalty. Don’t ever let anyone tell you Medicare is free...lol

I’m living on a fraction of what you will be, but I lead a very simple life with which I am content for the most part.

Enjoy your retirement! I sure have!

69

posted on

08/19/2019 9:54:58 AM PDT

by

BamaBelle

(The storm has arrived!)

To: freedumb2003

Look into Chile - Temuco, Chile to be exact. Cost of living is next to nothing. The population has a very high European descent ethnic population (probably north of 85%). Climate is decent and you won’t have hardly any of the drama that Mexico, Central America, Brazil or Argentina brings with riots, protests, and cartel violence.

It’s in the ring of fire so take that into account, but I’m headed there once I cash out (Lord willing).

Keep working though - you’d rake in big bucks with your computer experience.

DO NOT...and I repeat DO NOT get involved with women there if you care at all for your wallet and your finances. They will ruin you.

70

posted on

08/19/2019 9:55:28 AM PDT

by

Roman_War_Criminal

(Like Enoch, Noah, & Lot, the True Church will soon be removed & then destruction comes forth.)

To: freedumb2003

Can I retire on $500K?Of course! You can retire on $5.00, for that matter! No law against either!

71

posted on

08/19/2019 9:55:32 AM PDT

by

Lazamataz

(We can be called a racist and we'll just smile. Because we don't care.)

To: freedumb2003

First, I would not hire Cordell and Cordell. I would consider talking w/your wife and perhaps agreeing on mediation, which will be much, much cheaper. As you have no kids, there shouldn’t be much to argue about. If you really think you need a lawyer, hire a reputable, local attorney with an office next to the courthouse where the divorce proceedings will take place. Both of you can also hire one lawyer, who can give both of you an impartial, unbiased assessment of what each of you would get if the matter was contested.

Second, 500k plus 80k per year (or more with the pension and SS) is plenty of money for one guy to live off of. 500k per year invested correctly means you will get 20-25k per year on top of the 80k, without losing the principal.

Third...Do you have any healthcare issues? Health insurance rates need to be considered since you wont’ go on MediCare until age 65. Hope this helps.

72

posted on

08/19/2019 9:55:33 AM PDT

by

bort

To: Lazamataz

Of course! You can retire on $5.00, for that matter! No law against either! Cool!

Can I borrow $5.00?

To: freedumb2003

Sorry for double post...grrr

74

posted on

08/19/2019 9:57:04 AM PDT

by

BamaBelle

(The storm has arrived!)

To: freedumb2003

During the Great Recession I day dreamed about moving to Ecuador. I saw an HGTV International show about US expats that did exactly that. Keep in mind this was 10 years ago. back then you could buy an ocean front condo for less than 100K. There were ocean front houses for 150K.

The interesting part was that all the real estate people were exgringos. They had moved down there to be surf bums. Then they found out they could make a living selling houses to other expiates that needed guidance on exactly what they had gone through to make the transition.

There was no MLS listing there. Also, Ecuador nationals are not that into vacationing at the beach like us northerners.

Anyway, my business got better and the real estate market down there took off. Prices are up big time from 10 years back.

The one thing I learned was to get an extended stay visa you had to either buy property OR put $25K into one of their banks.

To: freedumb2003

I am not there, so I can’t speak from experience, but it will depend on the lifestyle you want.

Social Security is going to be so much a month for you when you retire, and 500k.

4% rule says taking 4% of your savings should get you 30 years...

4% of 500k is 20k.

So, if your social security income (when you retire) plus 20K a year more is enough for you to feel comfortable in retirement, then you are okay. If not, then you have to build up that nest egg some more, or find some other sources of income in retirement.

That’s just general “rule of thumb” stuff.

Obviously as others have suggested, you can certainly live comfortably on a lot less money by changing where you live... There are countries with a lot of ex pats living in them in communities who are living very comfortably on amounts of money that would be considered very low in US.

Good luck....

To: Larry Lucido

"Of course! You can retire on $5.00, for that matter! No law against either!"

Cool! Can I borrow $5.00?What, you want my entire retirement savings???!?

77

posted on

08/19/2019 9:58:45 AM PDT

by

Lazamataz

(We can be called a racist and we'll just smile. Because we don't care.)

To: freedumb2003

This is an extremely pertinent question for me right now!

78

posted on

08/19/2019 9:59:49 AM PDT

by

DungeonMaster

(Prov 24: Do not fret because of evildoers. Do not associate with those given to change.)

To: buwaya

“but certainly in Malaga or Sevilla, etc.”

If you can stand that heat...

I’d worry more about the endless migrant boats washing up on shores and the constant political unrest there than finances to be honest.

My mom is from Bilbao, I’ve seen my fair share of Spanish crazy.

79

posted on

08/19/2019 10:00:46 AM PDT

by

Roman_War_Criminal

(Like Enoch, Noah, & Lot, the True Church will soon be removed & then destruction comes forth.)

To: CodeToad; freedumb2003

"Reliable retirement investment is 5%"Risk free returns (10 year T-Bill) is at 1.5%. A 5% return is only attainable with a pretty heavy exposure to equities which carry a lot of downside risk.

The current risk-free return of 1.5% is entirely eaten up ENTIRELY by annual inflation, so your REAL annual return is ZERO.

Your success in retirement if you are heavily invested in equities depends to a huge extent on the performance of the stock market during your first two or three years of retirement. If you retire into a bear market and lose a lot of principal, you will never earn it back. If you retire into a bull market and your savings grow, you will be in clover. So, if you are counting on the stock market to fund your retirement, much is out of your control. Some people will retire into a bull market and enjoy a prosperous retirement; others will retire into a bear market and have to pinch pennies throughout retirement.

Maybe you are familiar with "Monte Carlo Simulations." These are mathematical simulations of events with known (or estimated) probabilities. I highly recommend the use of the "Portfolio Visualizer Monte Carlo Simulation" to simulate how your portfolio will do in retirement. "This Monte Carlo simulation tool provides a means to test long term expected portfolio growth and portfolio survival based on withdrawals, e.g., testing whether the portfolio can sustain the planned withdrawals required for retirement."

It includes a parameter they call "Sequence of Returns Risk" which lets you specify how bad the first X years of your retirement will be financially. You specify the "Worst X Years First" where you are saying those first years will be your worst returns in your retirement.

It includes many asset classes grouped into U.S. Equities, International Equities, Fixed Income, and Other and you can select a portfolio risk level. You can also model different rates of inflation.

If you have limited financial skills or no understanding of simulations and financial modeling, perhaps you could enlist a friend or financial advisor to set up the model and run it for you.

The other extremely important thing to do is create a detailed spreadsheet of all your sources of income, expenses, and expected financial returns on your investment. The single biggest expense that bites people in retirement is health care. You live your life out being reasonably healthy with few major problems and expect that to continue in retirement. But it doesn't work that way. Health can deteriorate seriously and quickly as we age and those expenses can be huge.

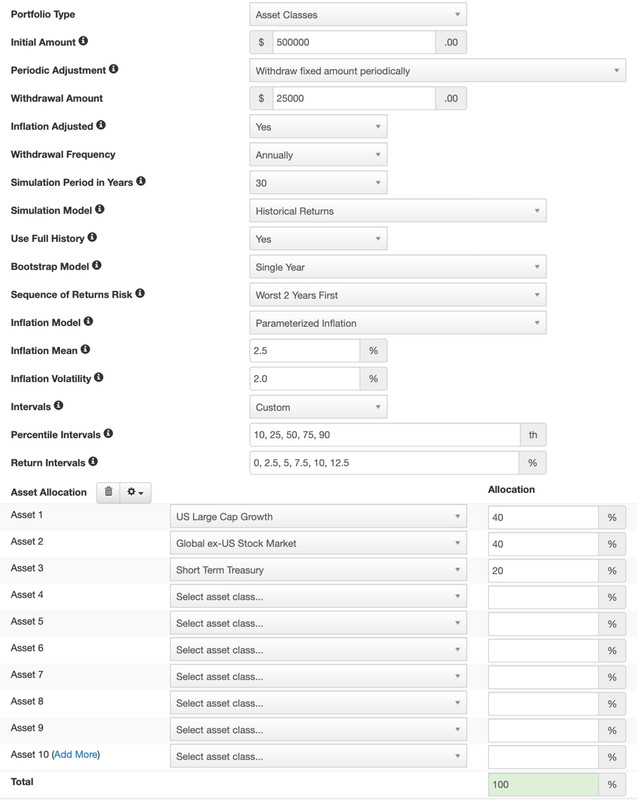

Here's a screen cap of the setup of Portfolio Visualizer Monte Carlo Simulation. I set up your $500,000 savings split 40% in US equities, 40% in International equities, and 20% fixed income. I specified we are going into a two-year bear market.

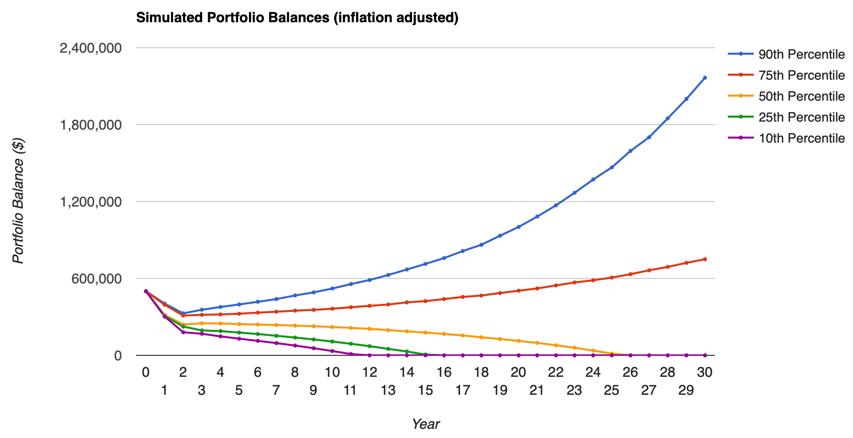

Here are the results. At the median case and withdrawing $25,000 per year, your savings are exhausted at year 26. Note that this model does not provide the flexibility to withdraw a large amount at a given year to deal with emergencies such as health care.

Until you develop a more concrete plan and model it mathematically as I've suggested above, there is really no way to say if you can make it on $500k. This is not something you want to do on the back of an envelope. A detailed spreadsheet model of your next 30 years will help provide guidance on where you can afford to live and how well you'll do in retirement.

If your $500k is invested with a company like Fidelity, you can get good, free retirement planning from them as well as recommended stock portfolios that match your risk tolerance. You might find that your investment company can run the Monte Carlo Simulations for you. My company does that, but I prefer doing it myself with the "Portfolio Visualizer" tool I linked to above.

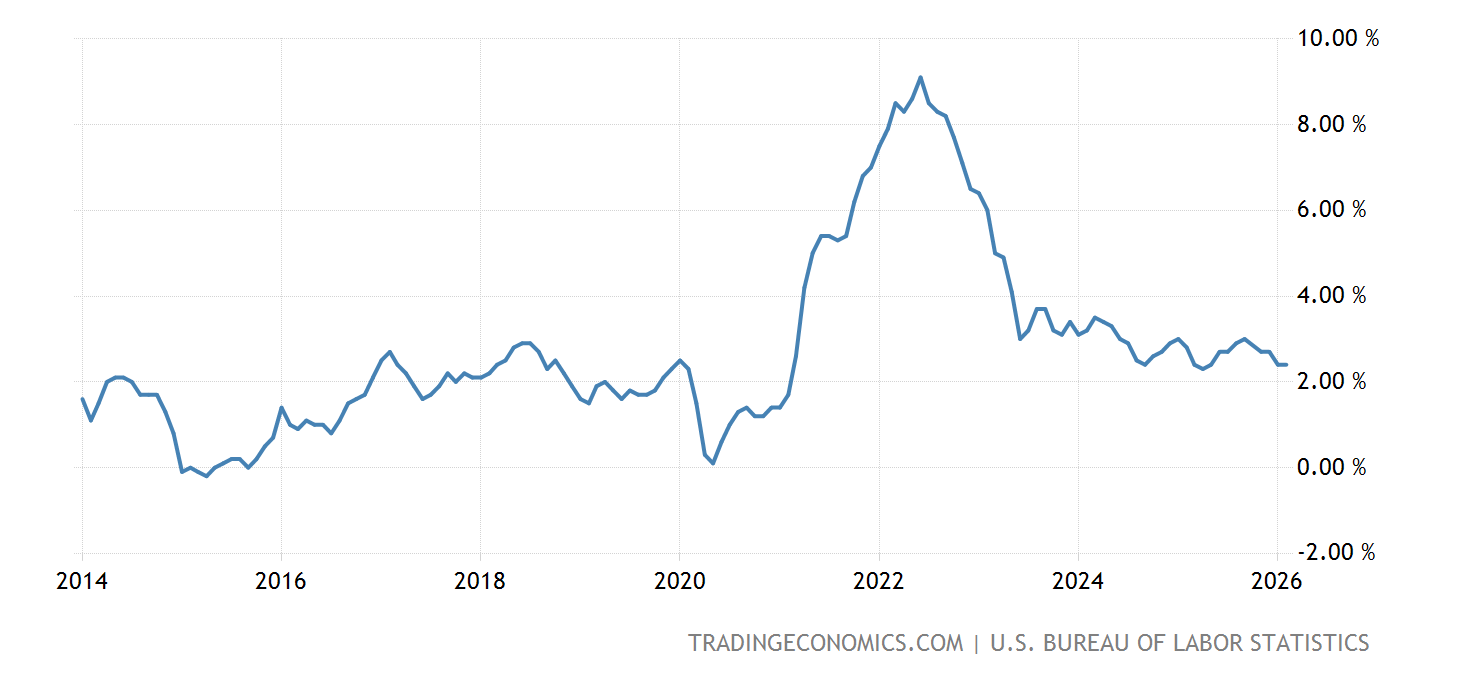

The last thing is do not underestimate the ability of inflation to eat away at your savings. A mere 2% inflation rate will, over 30 years, wipe out 80% of your spending power (if you got 0% on your investment). If you put your $500,000 into a 10 year T-Bill, spent none of it, and inflation was the same as your T-Bill rate, you would have $500,000 of purchasing power (in today's dollars) left. But, if inflation ran 1.0% higher than your T-Bill rate, you would have $362,000 left in today's purchasing power.

The chart below shows United States inflation the past five years:

Navigation: use the links below to view more comments.

first previous 1-20 ... 41-60, 61-80, 81-100 ... 221-228 next last

Disclaimer:

Opinions posted on Free Republic are those of the individual

posters and do not necessarily represent the opinion of Free Republic or its

management. All materials posted herein are protected by copyright law and the

exemption for fair use of copyrighted works.

FreeRepublic.com is powered by software copyright 2000-2008 John Robinson