Posted on 11/10/2025 6:56:25 AM PST by Red Badger

President Trump likes to test policy proposals on social media.

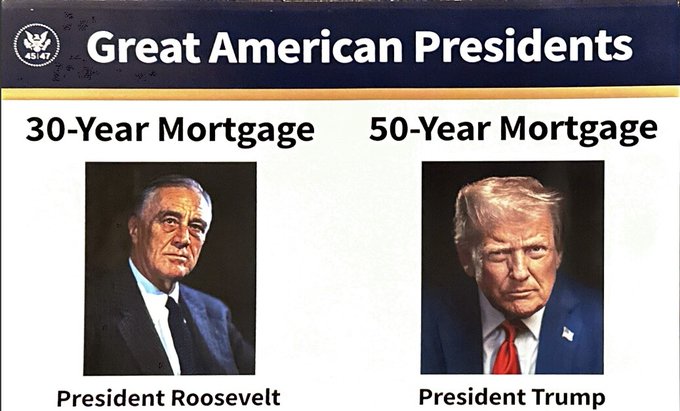

This was his newest one, shared by Bill Pulte, the U.S. Director of Federal Housing and the chairman of Fannie Mae and Freddie Mac 👇

Thanks to President Trump, we are indeed working on The 50 year Mortgage - a complete game changer. https://t.co/HZDPzO0qJG— Pulte (@pulte) November 8, 2025

A 50-year mortgage would result in a slightly lower monthly payment, stretched out over 5 decades, with hundreds of thousands of extra dollars in interest.

The reactions were not kind.

But they were funny!

MANY TWEETS AT LINK>........................

I think it's safe to say that this proposal might end up in the "no-go" category.

(Excerpt) Read more at notthebee.com ...

Exactly.

Too many people are getting hung up on the idea “few mortgages are actually held to maturity; people upgrade, refi, etc”.

Sure - but man, it’s like very few people here understand how amortization tables work.

Push those tables out to *50* years - and you have to understand the “standard benchmarks” no longer work and they’re NOT linear.

Generally, the 5 year mark is considered a break-even point. On a 50? It’s *MORE THAN* 10 years — because again, the amortization is NOT LINEAR.

There is a very small sliver of buyers - the ones who will put 20-30% or more down, buying in ridiculously low-rate environment we’ll probably never see again, where a “forever mortgage” might well be a good deal.

That will NOT be the overwhelming majority of such buyers.

What such folks will find is that they’re stuck in those 50 years and you’ll find a LOT more borrowers underwater.

Interest on a mortgage is front-loaded. That’s simply how they work. Without checking your math - but I suspect it’s close to true; you’re talking about a ridiculous amount of time to hit an equity mark where you realistically *CAN* upgrade. It certainly will not be the standard “5 year rule”. Hell, it’s generally not that for sub-10%/FHA loans *now*.

...And people talking about “Oh, extra payments!” are contradicting themselves or missing the point: SOmeone who needs to stretch out to 50 years to afford the monthly probably CANNOT pay extra - if they could? They wouldn’t finance over 50 years.

A 50-year mortgage would result in a slightly lower monthly payment...

Bears bolding, underscoring, and repeating.

I bought my first house when I was 20-something, it was a 30 year mortgage at 10 1/2 percent. I put, I think 20% down, which was all our wedding gift money, and some money from my parents, as I recall.

It was at the top of the market. I thought it was too high, but I was pressured into buying by assurances from my wife’s family that you “never lose money in real estate.”

I sold it about 7 years later for about what I bought it for. After commissions, fees, and paying off the bank, I walked away with half of my original down payment.

I rented for years, and what was nice about that was I didn’t have the equity tied up, repairs were taken care of with a phone call, and I could move anytime I wanted to without incurring the transactions costs.

I liked it, but got sick of dealing with landlords that would snap up the properties and immediately raise the rent.

So eventually I bought a small (not too small) prefab 3 bed 2 bath house. I think the interest rate was about 6 1/2% a year, which in my 20s I thought I’d never see again. I refinanced when it was about 2 3/4% and paid the thing down with any extra money I would have.

After I got married (again), we bought a house at the bottom of the market for about 50K under appraised value. The bank screwed me by forcing me into a 30 year mortgage, at about 1/2% above the 15 year rate because I owned a second house.

I later sold the other house, although I hated giving up the low rate, and put the proceeds on the new house, cutting the mortgage about in half. Over the next 5 years every extra penny I could scrounge went into the mortgage, and I paid it off in about 5 years.

I screwed the bank out of 25 years of interest.

I now put the equivalent of the mortgage payment into a “house fund” used only for house repairs and improvements.

My only issue now is my stupid real estate taxes. You’d think I’d own the thing clear by now.

“But you do you, reddit fag.”

I see you have clarified your earlier post so no one will interpret it as referring to the death of the borrower.

” We need to increase wages and bring housing costs down.”

I’m all for making more money, and having lower costs. That said, I’m also for personal responsibility.

If a person want to make more money, they have to provide more value to their employer. There’s plenty of folks out here making a lot of money, and able to buy houses at today’s market. They provide value to their employers.

“We” can’t expect higher wages just to appear suddenly, overnight, “we” have to earn them.

Housing costs are in line with the market, if they weren’t, they would come down. That’s just how it works.

Again, personal responsibility. Control spending, is how you keep your costs down.

Nail/hair salons, tattoo parlors, lottery tickets, fast food, music/cable tv, drugs/booze, are all choices people make. I’m proof you can live without all of them.

We shall simply disagree on this, then. I read your statement above as "I rent, kind of sort of." Totally your choice. We pay zero interest on zero debt on our homes, and even bought out my BIL's when he got into some cash flow difficulties, all duly registered with proper county officials. Different philosophies of life.

“My only issue now is my stupid real estate taxes. You’d think I’d own the thing clear by now.”

“affordable housing” is Democrat Newspeak for ‘Future ghetto’..............

What if housing prices declined

$410,000

$390,000

$370,000

$350,000

....

People would stop buying and building houses. I believe the stock folks call it catching a falling knife. Rents would rise and buying no longer is seen as a viable option.

People might even default on their mortgages. Many mortgagors are immigrants and they don’t have to stay in the USA to face debt collectors.

“but I suspect it’s close to true; you’re talking about a ridiculous amount of time to hit an equity mark where you realistically *CAN* upgrade. “

Please explain what you mean by “upgrade” and why it would take a ridiculous amount of time to do so.

My original post said nothing about the death of the borrower, moron.

You will never own your home and your property taxes will continue to go up and up. Property taxes are one of the biggest con-jobs ever.

“We pay zero interest on zero debt on our homes, “

I have a mortgage at 3.1%. Essentially the bank has loaned me that money which is invested in stocks.

The 2.5% qualified dividends almost pays the interest.

The stocks are appreciating at over 10% per year giving me a net profit.

“My original post said nothing about the death of the borrower, moron.”

I didn’t say it did.

“ One of the things I see is people expecting t afford a home on a single income. That has NEVER been the model.” That was the model when I was growing up in the 50’s.

“You will never own your home “

Silly tripe.

It’s bs? Stop paying your property taxes and find out who really owns your property. Report back.

“Property taxes are one of the biggest con-jobs ever.”

Your elected officials provide you with the budget details.

If you disagree with how they spend your money vote them out.

Wow! This makes Tesla’s Tiny houses much better.

You can still get a 10 year, 15 year, 20 year, or 30 year mortgage.

And you can still make extra payments if you want to pay it off sooner.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.