Posted on 03/12/2023 8:58:20 AM PDT by E. Pluribus Unum

“I’m seeing a lot of new kids who have never learned or even been taught the lessons that came hard for so many who are now irrelevant.”

I think they have a saying for that... “Those who do not learn history are doomed to repeat it.’

That and the lesson that just because your college drinking buddy has an accounting degree and can balance his checkbook doesn’t mean he can be a good CFO.

I’ve seen too much of this over the years.

Do you know who Jim Rickards is? Are you familiar with “bail-in “?

You must have quite the resume to call Jim a moron.

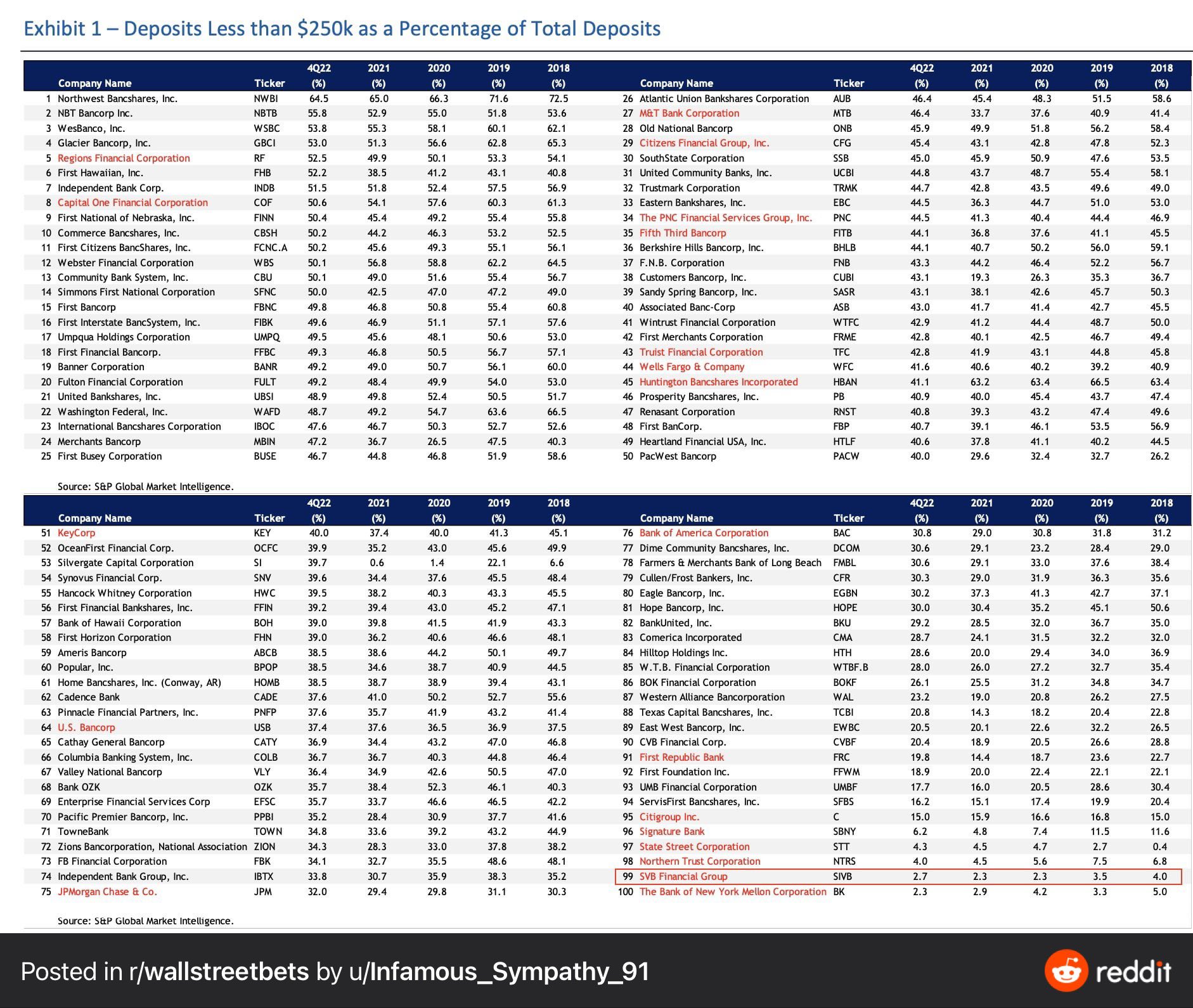

It really is eye opening to see this chart.

To look at it and realize just exactly how few accounts are covered by the fabled FDIC.

“Word to the Wise … Listening to ideas related to complex issues that are posted in a 280-character Twitter message is likely to make you mentally retarded.”

Word to the wise.. know who is making the Tweet before judging my IQ for sharing it.

There is talk that the State of California will beil them out and save California state depositors

Perot waws brought to us by narrow minded voters who preferred a democrat over a Republican.

In the last few decades so many political and business fads have occurred that Charles Mackay’s famous book “Extraordinary Popular Delusions and the Madness of Crowds” needs new volumes adde to it.

-PJ

Businesses are not stupid depositors - they have to keep millions in liquid cash somewhere to cover payroll and operations. Putting it in 50 different backs to try to stay under the FDIC limit is extremely counterproductive.

The problem is - retail banking is a utility function, and safety of deposits is paramount. Retail banking needs a hard and impenetrable firewall between its operations and the speculative ventures of investment banking. Which it had until 1999, when Phil Gramm and the Republicans insisted on repealing Glass-Steagall and letting the gamblers loose.

Every medium and large company is now forced into partnership with some speculator or another, and just has to hope the management can restrain its impulses far enough to keep its depositors relatively safe.

The likely solution is to just borrow a few more trillion into existence to cover endangered deposits across the industry - but as one commentator said of the COVID stimulus "Hey, we're a rich country. We can afford it." /s

Simply put it's because they have other concerns. Which adds an unquantified amount to risk. That "unquantified" part is fine for horse races but not for bankers. Here we are reminded of the fate of Eugene Lawson, Ayn Rand's "Banker with a heart". It wasn't pretty for his depositors either.

I note that Yellen has announced the Feds aren't bailing the bank out. It means that they are, they're just going to call it something else.

Quit asking sensible questions! LOL!

“Federal Deposit Insurance Corporation (FDIC), which only covers accounts up to $250,000” . . . is too general a statement.

That statement in the article, gives people the wrong impression that each bank account is covered up to $250,000.

Reference, see:

https://www.fdic.gov/resources/deposit-insurance/financial-products-insured/

Scroll down to “Single Account” at the FDIC website link and click on the right arrow. In the resulting info, scroll down to where you will see a notation:

“Coverage Limit: All single accounts owned by the same person at the same bank are added together and insured up to $250,000.”

"Stakeholder" is a weasel-word used by stealth Communists to insinuate ownership rights over things that do not belong to them.

I suggest you read on. In my experience there are many ways multi-million and multi-National corporations have of mitigating their risks without having to rely on the FDIC coverage. Rule number one: diversify (and that includes your banking relationship).

The fact that this apparently fundamental rule is forgotten shows how much we as a society have come to expect Uncle Sam to bail us out.

Yes.

How quickly that has been completely forgotten.

Why are some banks with higher percentages shown in red? It would seem they are less at risk than many below them. What am I missing?

As much as I would like to blame the SVB failure on a bunch of queers, trannies, and Greta Thunberg clones, the truth is, that stuff probably played a minor role in this - and probably not the way suggested by Breitbart.

Let me speculate. The lesbian chick who was the head of Risk, was (link below) “While Silicon Valley Bank careened toward its spectacular collapse, the bank’s head of risk management for Europe, Africa and the Middle East (Jay, the lesbian chick) devoted a chunk of her time to various LGBTQ+ programs. “

Sooo, Lesbian Jay, wasn’t even the head of risk for AMERICA. I GUESS that the root problem is that the Board and the Officers are hiring from a pool of conformist followers, like Lesbian Jay, not hiring people who can think for themselves.

Following that, from https://www.zerohedge.com/markets/fatal-distraction-senior-svb-risk-manager-oversaw-woke-lgbt-programs :

Meanwhile, SVB went without a chief risk officer (CRO) from April 2022 to January 2023, the Daily Mail reports, as the bank apparently had little urgency to replace Laura Izurieta before finally tapping Kim Olson earlier this year.

On the other hand, a few months before that long CRO vacancy began, SVB boasted, “We have a Chief Diversity, Equity and Inclusion Officer, an executive-led DEI Steering Committee and Employee Resource Groups with executive sponsors focused on these objectives.”

Another thing is, Treasury Bonds are not necessarily Green investments.

I would also guess that Senior Management knew long ago that their low interest bonds should have been dumped, and maybe other low interest stuff. But who knows what role that possible officer’s bonus programs would have been affected.

I think maybe these Banks, and much of white elitist management, are subject to the same factors as the British once were, when various Lords were automatically presumed to be intellectually fit to lead troops into battle. It was a class thing, and I think our management in this country is doing the same thing and hiring from the same pool of silly tw@ts who have the college creds, and very little common sense, or ability to think outside the box.

Look at Lesbian Jay’s pic on the zerohedge link, and tell me if you think she has the same intellectual capacity or common sense of say, Cowboy Bob, who got his degree from the University of Oklahoma, and worked on a ranch to pay his way thru college?

Being Woke is just an aside from the ultimate problem — THE MASSIVE SPENDING AND MONEY PRINTING OF UNCLE SAM UNDER JOE BIDEN AND THE DEMOCRAT CONTROLLED CONGRESS!!

Looking at it clinically, I would not call SVB a fraudulent business. Ok, they indulged in woke nonsense but the bottom line is, they were a victim or of their own initial success and poor risk management of excess liquidity.

And Congress and the free spending Biden administration are ULTIMATELY the culprit here.

It’s all an extension of Fed policy to curb inflation, reversing a 13-year zero-rate policy. And why did inflation occur? Isn’t it because of the massive increase in government spending, which resulted in huge printing of money ?

This of course pushed up rates in the middle and right side of the yield curve, devaluing existing bond holdings locked into older rate patterns. Investors noticed and then depositors too. The high-flying institution that specialized in providing liquidity in industries that have lost their luster suddenly found itself very vulnerable.

In addition, the SVB and probably other banks were exposed with a portfolio of collateralized mortgage obligations and mortgage-backed securities. But with rates rising, those are coming under stress too as high leverage in housing and real estate become untenable amidst falling valuations. Borrowers are finding themselves under water and that in turn adds to stress on lenders.

And where did SVB, and the entire banking industry, get the funds to bulk up their portfolios with such debt holdings? You guessed it: STIMULUS PAYMENTS!’

Hundreds of Billions flooded in and it had to be parked somewhere making some return. At the time it seemed like a good deal, until Fed policy changed.

Immense government spending which produced debt that was quickly monetized and eventually caused inflation, prompting the Fed to reverse course with the largest/fastest rate increases in history. And guess what? IT’s STILL GOING ON!

This destabilized (or restabilized) production structures away from the right side of the yield curve toward the left, shifting capital in search of return to the consumer-goods sector. Labor has begun to follow, thus creating a surplus of resources in information tech and a shortage in retails.

It was always naïve to think that this shift would take place without touching the banking institutions that shoveled leverage in the direction of industries that thrived during lockdowns but are cutting back massively

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.