Posted on 08/29/2022 5:23:07 AM PDT by Red Badger

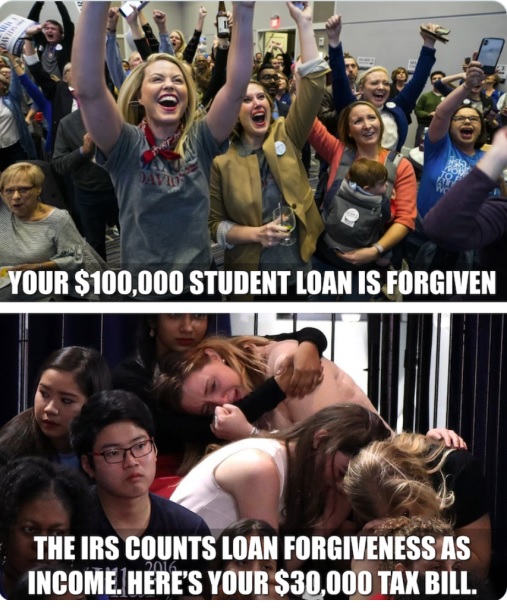

Borrowers in thirteen states who have student debt canceled under the Biden administration's plan may still be taxed hundreds of dollars next year on their forgiven loans.

President Joe Biden announced major reforms to student debt last week, including how borrowers making less than $125,000 a year (or up to $250,000 as a family) may have up to $20,000 in loans canceled for Pell Grant recipients and up to $10,000 forgiven if they did not receive a Pell Grant.

Thirteen states, including New York and Virginia, treat forgiven debt as income, which means it is subject to state taxes. This means borrowers who have their student loans forgiven may end up owing hundreds of dollars, according to an analysis published Thursday by the Tax Foundation, a nonprofit policy organization.

The Tax Foundation's Vice President of State Projects Jared Walczak said that the maximum likely tax liability would double for those who have $20,000 in debt forgiven. For two states — New York and Wisconsin — Walczak's analysis did not include the rare case in which the maximum tax amount would change for someone who may qualify for loan forgiveness based on 2020 earnings only to enter the top-income bracket this year.

=========================================================

State Maximum tax if $10,000 in debt is discharged Maximum tax if $20,000 in debt is discharged

Arkansas $550 $1,100

Hawaii $1,100 $2,000

Idaho $600 $1,200

Kentucky $500 $1,000

Massachusetts $500 $1,000

Minnesota $985 $1,970

Mississippi $500 $1,000

New York $685 $1,370

Pennsylvania $307 $614

South Carolina $700 $1,400

Virginia $575 $1,150

West Virginia $650 $1,300

Wisconsin $530 $1,060

=========================================================

According to the White House, more than 60% of borrowers are Pell Grant recipients, which means they will have to pay the higher tax rate.

The federal government normally treats the discharge of indebtedness as taxable income, but under last year's American Rescue Plan Act, forgiven student loans will not count as federal taxable income until 2025.

Walczak noted that his analysis "should never be construed as tax advice," as states have yet to issue direct guidance on how to treat student debt relief.

It’s only fair they get hit with income taxes, considering forgiven debt is considered income in most instances I can think of.

Great graphic.

Speaking of stupid: “more than 60% of borrowers are Pell Grant recipients, which means they will have to pay the higher tax rate.”

Journalists. It’s the same tax rate on double the amount. Dummy.

Yep, and Biden can’t forgive state debts! LOLOLOLOLOLOL!..........................

And those that have jobs will suddenly find themselves in a higher tax bracket......................

I’m surprised the Federal Government doesn’t tax them. It taxes Social Security, now.

Now that’s worth a big smile this morning...SUPER!

....Under § 9675 of the American Rescue Plan Act (ARPA), the forgiveness of student loan debt between 2021 and 2025 does not count toward federal taxable income...

how sweet it is, even informants pay taxes on income the govt gives them..

😉😁...........................................

The rules for student loan cancellation aren't in place yet, if it even gets implemented. The federal gubment may tax the debt cancellation, or it may not.

The federal government does not impose income tax on Go Fund Me accounts either. If I were a democrat and in business, I would rather have clients pay me through Go Fund Me than PayPal.

I could be mistaken but taxing Social Security benefits was put thru during the Clinton Administration.

Isn’t funny that social security which is a tax that everyone pays is taxed again when you start receiving benefits and for most people when they really need it.

Won’t happen.

In other words the government lied about it's promises to seniors. They lie about EVERYTHING.

I’m not surprised.

The SS tax paid from wages does NOT cover all of the benefits received in retirement. Presumably, they are taxing the ‘interest.’ But then, I am not a tax specialist, I don’t play one on tv, nor do I recall any other discussion of the issue.

And I have not spent the night at any Holiday Inn in many a year.

Banks weren't getting paid by deadbeats who NEVER intended to pay back for their "Inclusion, Female Studies, CRT/SJW Degrees", so the OWNED politicians are getting their payback for them from Taxpayers......same old "for the benefit of Donors" B.S. that extorts tax dollars for the benefit of supporters......VOTE BUYING racket for 70+ years, already.

Read that article again - the IRS does tax that forgiven debt - and it will - but not until 2025. The Federal tax obligation has been DEFERRED, but not forgiven. For those suckers who live in States with an income tax, the big “gift” will have additional taxes payable next year and it will be at a higher tax rate for both State and Federal income tax. The Feds call forgiven debt a gift and count it all as income. It will mean hundreds of dollars in a state tax obligation, and thousands in a Federal IRS obligation. How do I know? I had $40K forgiven in 2010 based on 100% disability. The IRS called it a gift and levied a $10K income tax obligation on me. I made payments for more than 10 years to pay that off out of the pitiable Social Security Disability I received.

SEC. 9675. MODIFICATION OF TREATMENT OF STUDENT LOAN FORGIVENESS.

(a) In General.—Section 108(f) of the Internal Revenue Code of 1986

is amended by striking paragraph (5) and inserting the following:

``(5) Special rule for discharges in 2021 through 2025.—

Gross income does not include any amount which (but for this

subsection) would be includible in gross income by reason of the

discharge (in whole or in part) after December 31, 2020, and

before January 1, 2026, of—

``(A) any loan provided expressly for postsecondary

educational expenses, regardless of whether provided

through the educational institution or directly to the

borrower, if such loan was made, insured, or guaranteed

by—

[[Page 135 STAT. 186]]

``(i) the United States, or an instrumentality

or agency thereof,

``(ii) a State, territory, or possession of

the United States, or the District of Columbia, or

any political subdivision thereof, or

``(iii) an eligible educational institution

(as defined in section 25A),

``(B) any private education loan (as defined in

section 140(a)(7) of the Truth in Lending Act),

``(C) any loan made by any educational organization

described in section 170(b)(1)(A)(ii) if such loan is

made—

``(i) pursuant to an agreement with any entity

described in subparagraph (A) or any private

education lender (as defined in section 140(a) of

the Truth in Lending Act) under which the funds

from which the loan was made were provided to such

educational organization, or

``(ii) pursuant to a program of such

educational organization which is designed to

encourage its students to serve in occupations

with unmet needs or in areas with unmet needs and

under which the services provided by the students

(or former students) are for or under the

direction of a governmental unit or an

organization described in section 501(c)(3) and

exempt from tax under section 501(a), or

``(D) any loan made by an educational organization

described in section 170(b)(1)(A)(ii) or by an

organization exempt from tax under section 501(a) to

refinance a loan to an individual to assist the

individual in attending any such educational

organization but only if the refinancing loan is

pursuant to a program of the refinancing organization

which is designed as described in subparagraph (C)(ii).

The preceding sentence shall not apply to the discharge of a

loan made by an organization described in subparagraph (C) or

made by a private education lender (as defined in section

140(a)(7) of the Truth in Lending Act) if the discharge is on

account of services performed for either such organization or

for such private education lender.’’.

(b) <> Effective Date.—The amendment made by

this section shall apply to discharges of loans after December 31, 2020.

https://www.congress.gov/bill/117th-congress/house-bill/1319/text

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.