Posted on 04/12/2024 1:16:11 PM PDT by lasereye

Homebuyers are feeling whiplashed by surging mortgage rates, and the outlook just turned grim.

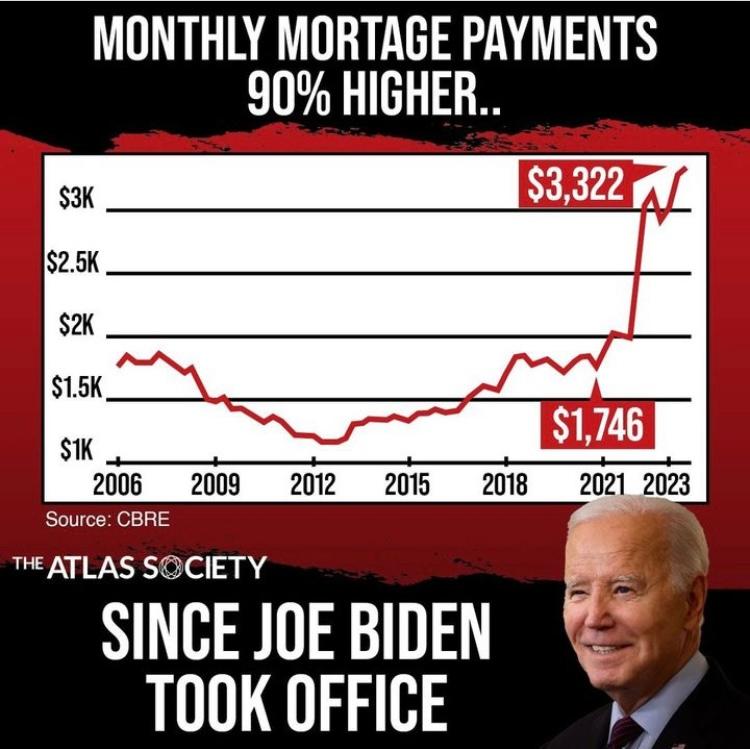

The average rate on the 30-year mortgage increased to 7.37% on Thursday, a steep climb from 7.11% at the beginning of the week, according to Mortgage News Daily. The quarter-point increase comes as rattled investors respond to a hotter-than-expected inflation reading.

At the same time, a separate measure tracking weekly average rates rose to 6.88%, up from 6.82% the week prior, Freddie Mac found.

Elevated rates have left would-be buyers in a pinch, causing both repeat and first-time buyers to step away from any purchase plans. For many, any shift in rates means losing more of their purchasing power.

With inflation still running hot this past month, the results haven’t been favorable for mortgage borrowers, housing industry experts said.

“March inflation figures were very bad, which also means bad news for interest rates,” said Lawrence Yun, chief economist at the National Association of Realtors.

As rates crested the 7% threshold, the share of refinance applications surprisingly spiked.

The volume of applications to refinance a home loan jumped 10% for the week ending April 5 and was 4% higher than the same week one year ago. The surge in applications was driven by Veterans Affairs (VA) refinance applicants, the Mortgage Bankers Association (MBA) reported.

One reason why homeowners could have been in a haste to refinance was the threat of rising rates. In January, refinance demand shot up by 30% compared to a year ago when rates averaged 6.62% per Freddie Mac.

As rates again hover in the high-6% range, homeowners are showing how attuned they are to small shifts. Leading the refinance surge were government loan applicants in hopes of snagging a lower rate.

(Excerpt) Read more at finance.yahoo.com ...

I’m going to sneak out then sneak back into the US as a Mexican and squat in a house somewhere.

Free money, free house…

I guess in 2012 under Obama every article used the term “unexpectedly”——now the term is “Hotter than expected”....

Bidenomics at work -

'The Bottom Down and the Middle in'

People who played the “unexpectedly” game have all died from cirrhosis some years ago.

Notice the little rats at Yahoo use the deceptive “Hotter than expected” instead of “Higher than expected”. They think they are clever and no one sees through this kind of BS.

If all the folks that believe the dollar is going to vaporize under the debt had any conviction-they’d be shorting US bonds and mortgages would be at 10%.

They seem to think dollar death 98.645 is new and novel with the 30yr seeing the govt borrowing at 4.5% but don’t have enough conviction to do anything about it-beyond endless doomsday barking at the moon.

Unexpected!

Things are desperately out of whack. A little house down the road on 30 acres, 2600 sf, clapboard, looks like crap, nearly $600k is the asking price. Not 8 years ago I sold 3,600 sf on 5 acres Houston suburbs, prime condition, large climate controlled shop for less than this asking price. Eight years ago. We are in insane times and we will not recover for a very long time if at all.

As the old quote goes:

“How did you go bankrupt?”

“Slowly at first, and then all of a sudden.”

We’re in the “slowly at first” phase.

“Oil surges to highest level since October on escalating Middle East tensions”

“Nvidia is in a bubble, stocks will disappoint for a decade, and a recession will strike this year, markets guru warns”

https://finance.yahoo.com/news/nvidia-bubble-stocks-disappoint-decade-170002409.html

“Auto insurance premiums are skyrocketing.”

Still pretty low, my first mortgage was 8 something with a 10% 2nd.

I have a couple of friends that are mortgage brokers. They are having to take on second jobs because their business is down so much. This BS has a hidden ripple effect. Mortgage companies, moving companies, relocation companies and on and on. In the last month I have seen just 2 moving vans.

Factor in Real Inflation with consumables, and we are in a wheelbarrow economy.

Would you move from something you can now afford to something you can’t? I wouldn’t, even to make an equity increase. You likely would still have the same mortgage face amount with a higher interest rate. AND you can’t move down without paying cap gains tax.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.