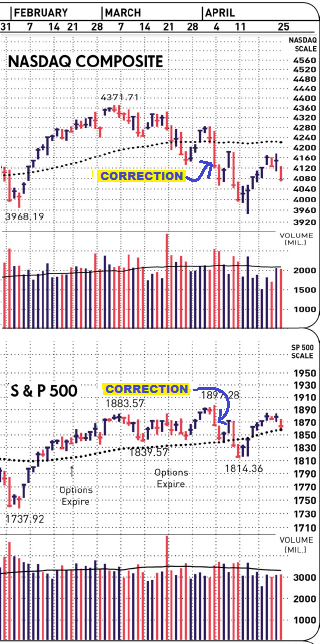

While we've all been asking 'which way' for the past few weeks all we've been getting is 'nowhere in particular'.

Article from MAPI this morning:

Uncertainty’s Chokehold on Growth Daniel J. Meckstroth, Ph.D. Tuesday, April 29, 2014

Uncertainty's Chokehold on Growth

Need to Know . . .

Public policy uncertainty creates an option value for waiting in order to gather more information about expenditures with irreversible costs

Uncertainty spikes before and during a recession and remains elevated for a couple of years as government policy changes multiply to fix the problems seen as the recession's root causes

The 2008-2009 recession was associated with a record level of uncertainty that intensified until the resolution of the fiscal cliff

Many studies have found that the growth rates of output, investment, and jobs decline with an increase in public policy uncertainty

Introduction

Public policy uncertainty plays a role in restraining business investment and therefore economic and employment growth. Product market growth, projected cash flow, and expected profits are naturally the most important drivers of business investment but uncertainty creates an option value on the financial returns for waiting in order to gather more information. Public policy uncertainty tends to be pro-cyclical and accentuates the downturn, impedes the recovery, and reinforces the boom times—just the opposite of what fiscal policy should do to dampen the business cycle. Minimizing policy changes in times of economic duress would reduce uncertainty and greatly improve the pace of recovery and expansion by removing a restraint to business investment and private sector employment growth.

Uncertainty Is Building

While death and taxes may be seen as the sole certainties of existence, defining uncertainty within the realm of economics requires a more structured approach. Economist Frank Knight said that an unfavorable event is a risk if its probabilities are quantifiable. For example, life insurance firms manage risk by using national mortality tables and data from past experiences to calculate the expected probability of policies paying off in a given year.

Economic uncertainty, however, can be described as an environment in which little or nothing is known about the likelihood of an event. Beyond natural disasters, causes include

changes in economic and financial policies; political battles; wars; acts of terrorism; and the impact of intrusive government policies and regulations.

Political brinkmanship and governmental dysfunction loom large in the recent past, with the 2011 showdown over the Treasury debt limit, sequestration, the 2013 federal government shutdown, and another delay in raising the Treasury debt limit in early 2014 creating significant uncertainty. Sizable changes in government discretionary spending and tax policy have also occurred.

Regulators are implementing some of the largest, most complicated, and far-reaching legislation in decades, with Dodd-Frank reforming the financial markets and the Affordable Care Act restructuring the health insurance system. It is no wonder that in a survey by the Business Roundtable in the fourth quarter of 2013, 39% of CEOs named regulatory costs as the #1 cost pressure affecting their businesses over the following six months. Regulatory costs were also the top concern in the survey one year earlier.

Measures of Uncertainty

Commentators report that the thick haze of economic uncertainty is having a detrimental impact on business activity. Researchers find a “strong rise in the frequency of discussions of policy-related uncertainty” over the last three decades of the Federal Reserve’s Beige Book releases, which are summaries of Fed economists’ dialogues with executives about business conditions.

Another sign of the changing environment is the sixfold increase in the page count for the annual Code of Federal Regulations since 1950. A study commissioned by MAPI found that the average number of major federal regulations promulgated annually has risen drastically over the past three administrations, from 36 during 1993-2000, to 45 during 2001-2008, to 75 during 2009-2013. Figure 1 shows the unrelenting growth in the cumulative major and non-major regulations directed at the manufacturing sector. These regulations layer on top of each other, generating a negative economic impact greater than the sum of the individual laws.

Figure 1 – Regulation of Manufacturing Is Accelerating

Note: President Clinton issued Executive Order 12866 in Sept 1993, greatly reducing the scope of OIRA regulatory review

*The count of regulations in 2013 is shown through July 31 Source(s): OIRA dataset and NERA analysis

Economists have experimented with methods of measuring economic uncertainty. The Baker-Bloom-Davis method has been getting notable attention as of late. This composite index is composed of three weighted underlying components:

News coverage from 10 large newspapers, with searches for the words “uncertainty” or “uncertain” plus “economic” or “economy” in combination with any of the following terms: Congress, legislation, White House, regulation, federal reserve, and deficit. Counted articles include terms in all three categories: uncertainty, the economy, and policy.

The number of temporary provisions in the U.S. tax code. The rationale is that temporary tax measures create uncertainty for businesses and households because Congress often extends them only at the last minute, undermining the certainty of the tax code.

Data from the Survey of Professional Forecasters analyzing the degree to which economists agree or disagree. This report is used to discern the dispersion of forecasts among economic projections. Index values larger than 100 indicate an above-average level of uncertainty.

The history of the Baker-Bloom-Davis uncertainty index, displayed in Figure 2, reveals that the level of policy uncertainty is cyclical and volatile. Uncertainty spiked upward to an unprecedented level in the 2008-2009 recession and continued to rise during and after the economic recovery. It was not until the resolution of the fiscal cliff in the early hours of 2013 that uncertainty began to subside.

Figure 2 – U.S. Economic Policy Uncertainty

Source(s): Scott Baker, Nicholas Bloom, and Steven Davis at www.PolicyUncertainty.com

Uncertainty Is Pro-Cyclical

The level of uncertainty is volatile and cyclical, rising in recessions and falling in booms. The general level was elevated in the late 1980s and early 1990s and then settled into a lower level in the mid-1990s. Widespread euphoria during the dot-com boom in the second half of the 1990s drove down uncertainty because the economy was growing above potential, the unemployment rate was extremely low, and the expectation was that the United States had transformed into a “new economy” resilient to recessions.

The relatively mild 2001 recession fed the perception that the government, particularly the Federal Reserve, could prevent a major recession. By 2005 and through most of 2007, the nation had a false sense of predictability, largely because of the enormous amount of home equity wealth created in the housing market boom.

Research shows that uncertainty always rises in a recession and the worry and unpredictability make economic conditions worse. After spiking before and during a recession, uncertainty remains elevated for a couple of years as government policy changes multiply to fix the problems seen as the recession’s root causes.

The degree of economic uncertainty relates to the depth of the recession and strength of the recovery. Recessions with a high degree of uncertainty are often deeper than those where the uncertainty level rises less. The same correlation with the uncertainty level occurs in recoveries, with an elevated level associated with a weaker recovery.

The 2008-2009 recession and its aftermath ratcheted up uncertainty. During the recession, uncertainty escalated to a relatively high level, and following the end of the recession in June 2009, continued rising for another 43 months until the January 2013 resolution of the fiscal cliff. In the previous two recessions, uncertainty continued to rise for an average of only 17 months.

Uncertainty fell sharply after January 2013 and the improvement in sentiment probably explains the subsequent improvement in economic growth despite the headwinds of a 2% increase in payroll taxes and higher marginal rates at the top tax bracket.

How Uncertainty Affects the Economy

A high level of uncertainty causes consumers and firms to postpone expensive purchases for goods with long lives. Economic theory describes the concept in terms of the option value of waiting. A firm or person may amass cash rather than finance an investment if uncertainty makes the investment’s rate of return difficult to calculate.

In times of significant uncertainty, firms lower investment demand and consumers stall spending on big-ticket items as they seek new information, since miscalculations are costly to reverse. Waiting increases the chance of making a more knowledgeable decision, i.e., the option value of waiting can be large. The greater the uncertainty, the greater the value of keeping the option to invest open; investors are willing to sacrifice current returns during the delay.

According to three researchers, uncertainty can depress hiring, investment, and/or consumption when agents are risk-averse or subject to fixed costs or partial irreversibility of the investment decision, or if financial constraints tighten in response to higher uncertainty.

Figure 3 shows the severe decline in inflation-adjusted business investment and the recovery’s slow pace in the 2008-2009 recession cycle. Private nonresidential investment (equipment, structures, and intellectual property) declined 20% from peak to trough. By comparison, the previous seven economic cycles showed an average 5% reduction. For the previous two severe recessions—1974-75 and 1980-82—private nonresidential investment fell by an average of 10%.

Likewise, the recovery in business investment is substantially less robust and more prolonged. A full recovery in business investment spending did not occur until the third quarter of 2013. If the current cycle behaved like the average of the previous two severe recessions, nonresidential investment would have recovered by the second quarter of 2011.

Figure 3 – Post-Recession Recovery in Private Nonresidential Investment

Source(s): U.S. Bureau of Economic Analysis and MAPI

The slow pace of investment is difficult to explain without using the level of policy uncertainty as at least a partial explanation. Businesses are as profitable as they have ever been. Corporate profit margins, measured by the ratio of after-tax profits to output, is at double the average level since World War II. Corporate balance sheets are loaded with cash and debt ratios are low. Banks have been easing credit terms for some time but large companies have the option to bypass the banking industry and sell corporate debt directly in the financial market. Considering these positive factors, it’s very likely that uncertainty has significantly held back growth.

Empirical Findings

Many studies have found that the growth rates of output, investment, and jobs decline with an increase in macroeconomic uncertainty. Findings from recent empirical analysis include:

“One standard deviation increase in uncertainty is associated with a decline in output growth of between 0.4 and 1.25 percentage points depending on the measure of macroeconomic uncertainty” (Kose and Terrones, 2012).

“Rising uncertainty accounts for roughly a third of the fall in capital investment and hiring that occurred in 2008-2010” (Stein and Stone, 2012).

A strong and negative relationship exists between cash flow uncertainty and corporate investment in both tangible and intangible assets. More importantly, a strong and negative relationship also exists between cash flow uncertainty and corporate employment. If uncertainty returned to pre-recession levels, employment would increase by 3.4 million and investment in plants and equipment would increase 1.5% (Bhagat and Obreja, 2013).

“Political uncertainty constrains business investment, especially on R&D, and reduces hiring and slows GDP growth.” Analysis using an econometric model showed that the rise in political uncertainty since the recession’s onset decreased inflation-adjusted GDP by about $150 billion, reduced employment by 1.1 million, and drove up unemployment 0.7 percentage points (Zandi, 2013).

Effects on Capital Spending

A recent MAPI survey of senior financial executives from large multinational manufacturing corporations found that uncertainty will not have a discernable impact on 2014 business investment plans for 58% of respondents. Nevertheless, 42% said that federal policy certainty would increase 2014 capital spending growth: 16% of respondents believed that capital spending would increase 1-100 basis points, 4% said 101-200 basis points, 4% said 201-300 basis points, and 18% said more than 300 basis points (Figure 4).

Using the midpoint of the ranges (for >300 basis points, 350 was used) and weighting by the composition of the respondents, the weighted average impact of the growth rate of capital spending is 90 basis points—or 0.9%—in 2014. Although the survey is not statistically representative, the findings are reasonably close to those found in academic studies.

Figure 4 – How Much Policy Certainty Would Increase Capital Spending in 2014

Source(s): MAPI Business Outlook March 2014