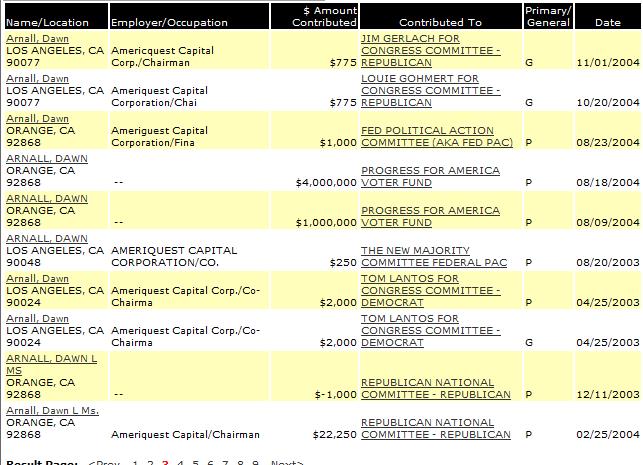

Best Rats and RINOs money could buy...

Posted on 08/27/2010 7:06:17 AM PDT by cycle of discernment

"Brad" commnets:

Below is a brief history of why the housing bubble burst.

» 1977: Democrat Jimmy Carter signs the Community Reinvestment Act, guaranteeing home loans to low-income families.

» 1999: Democrat Bill Clinton puts the CRA on steroids by pushing Fannie Mae and Freddie Mac to increase the number of subprime loans.

» September 1999: The New York Times publishes an article headlined "Fannie Mae Eases Credit to Aid Mortgage Lending," which warned of the coming crisis due to lax lending policies of the Clinton administration.

» 2003: The White House calls Fannie and Freddie a "systemic risk" and the Republican Bush administration pushes Congress to enact new regulations.

» 2003: Rep. Barney Frank, D-Mass., says Fannie and Freddie are "not in a crisis," bashes Republicans for crying wolf and calls F&F "financially sound." Democrats block Republican-sponsored regulation legislation.

» 2005: Federal Reserve Chairman Alan Greenspan voices warning over F&F accounting, saying, "We are placing the total financial system of the future at a substantial risk."

» 2005: Sen. Charles Schumer, D-N.Y., says he thinks F&F "over the years have done an incredibly good job and are an intrinsic part of making America the best-housed people in the world."

» 2006: Sen. John McCain, R-Ariz., again calls for reform of the regulatory structure that governs F&F.

» 2006: Democrats again block reform legislation.

» 2008: The housing market collapses; Democrats blame the Republicans.

(Excerpt) Read more at washingtonpost.com ...

BINGO, Nailed It, Post-of-the-day, and Bumpworthy!

Also note tagline.

It would make sense if Fannie was picking up the risk for the bad loans.

By the time the Bush administration rolled around, it was already too late. A major domino in the chain of events that helped precipitate the crisis — the repeal of the Glass-Steagall Act of 1933 — had already fallen in the late 1990s. In fact, it was the Republican Congress that passed the repeal of Glass-Steagall in 1999.

Simple. We were in the middle of two wars. The Republican administration had to buy off the Democrats in order to fund the wars. The Democrats held the country hostage for their own political gain.

And because the GOP is equally complicit. Seems to me that between Carter passing the CRA and the mortgage crisis of 2007-08, there were a few Republican presidents and Congresses that did little, if anything, to turn things around. Let’s not bury our heads in the sand and try to claim that the GOP is entirely without fault.

Suppose I could afford to make monthly mortgage payments of around $2,800 on a home ten years ago. If the mortgage term is 15 years and the rate is 8%, I could afford a mortgage of about $280,000 or so.

If you can afford the same monthly payments today but the term is 30 years and the rate is 5%, then you can afford about a $500,000 mortgage with the same monthly payment.

Did the price of the home go up by $220,000 because of normal economic factors of supply and demand? No. The price went up by $220,000 because the terms of your financing made it that way. This $220,000 figure showed up in the my pocket when the house was sold to you -- and then there was the "ripple effect" of realtor commissions, secondary economic benefits, positive impact on GDP figures, etc. And it was all just an illusion.

Excellent points. But I'd also like to add that Greenspan kept rates so low because he was trying to counter the effect from his previously inverting the yield curve (keeping interest rates too high).

ping

Thank you. I did a quick google and found lots of information.

That's because the Bank already got their money at a fixed rate when the loan was closed. Your analogy is akin to allowing the grocer to come to your house a week after you bought a chicken and demanding an extra 50 cents a pound because that's what he paid for it 3 days after you bought it.

My broader point really is that for a long time the GOP has done little to stem the tide of Democrat/socialist policies and protect us, finanially and otherwise. The GOP allowed Democrats to out-maneuver them many times over. The Bush administration repeatedly handed Democrats rhetorical victories. Elected Republicans tried to avoid the financial collapse - too little too late. Once Clinton put "the CRA on steroids" - elected Republicans knew full well what would happen. Even the NYT's in '99 lamented Clinton's policy.

and the dems always successfully painted the GOP as “mean” for wanting to put back in safeguarding regulations.

True, and the GOP surrendered repeatedly, because of this fear. Was it worth it? Shouldn't they have grown a spine and fought for us anyway?

You might not agree but I think elected Republicans could have done more (from '99 on) to avoid the collapse, or at least lessen its impact. imvho

I’m not sure I understand exactly what you’re saying. If I sign a mortgage on a property for $250,000 with a bank, then the bank has a $250,000 asset on its books earning a specific rate of return. If that rate of return is fixed for 30 years, then it’s fixed for 30 years. Unless they sell the loan to a third party, they hold it for as long as it takes me to pay it off.

Note for clarification: The value of that asset will decline from $250,000 to $0 as the loan principal is paid off.

I believe you originally posted that the Bank never has the opportunity to increase the interest rate when 'rates' go up. I responded to that. You sign a contract at a fixed rate of interest in a traditional mortgage.

Maybe I misunderstood you. Do you think the Bank should be able to change that contractual arrangement for some reason?

Bookmark

No, that's not what I'm suggesting.

I'm simply pointing out that if I sign a 30-year fixed-rate mortgage at a rate of 10% and the prevailing long-term mortgage rates decline to 5%, I always have the option of refinancing the loan at the lower rate. But if I sign a 30-year fixed-rate mortgage at a rate of 5% and the prevailing long-term mortgage rates increase to 10%, the bank cannot refinance the loan at the higher rate.

In other words, the "fixed" part of a fixed-rate mortgage only applies to the bank, since the borrower can always refinance the mortgage without paying a penalty.

Correct. The Bank can not force you to renegotiate your contract.

In other words, the "fixed" part of a fixed-rate mortgage only applies to the bank, since the borrower can always refinance the mortgage without paying a penalty.

In which case the Bank gets all of it's money plus the interest that's been paid during the course of the loan. The Bank isn't harmed in the least. In fact they've made a tidy little profit as the interest is front loaded into mortgage loans.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.