Posted on 01/13/2006 1:17:20 PM PST by Travis McGee

The economy that Alan Greenspan is about to hand over is in a much less healthy state than is popularly assumed

DESPITE his rather appealing personal humility, the tributes lavished upon Alan Greenspan, the chairman of the Federal Reserve, become more exuberant by the day. Ahead of his retirement on January 31st, he has been widely and extravagantly acclaimed by economic commentators, politicians and investors. After all, during much of his 18½ years in office America enjoyed rapid growth with low inflation, and he successfully steered the economy around a series of financial hazards. In his final days of glory, it may therefore seem churlish to question his record. However, Mr Greenspan's departure could well mark a high point for America's economy, with a period of sluggish growth ahead. This is not so much because he is leaving, but because of what he is leaving behind: the biggest economic imbalances in American history.

One should not exaggerate Mr Greenspan's influence—both good and bad—over the economy. Like all central bankers he is constrained by huge uncertainties about how the economy works, and by the limits of what monetary policy can do (it can affect inflation, but it cannot increase the long-term rate of growth). He controls only short-term interest rates, not bond yields, taxes or regulation. Yet for all these constraints, Mr Greenspan has long been the world's most important economic policy maker—and during an exceptional period when globalisation and information technology have been transforming the world economy. His reign has coincided with the opening up to trade and global capital flows of China, India, the former Soviet Union and many other previously closed economies. And Mr Greenspan's policies have helped to support globalisation: the robust American demand and huge appetite for imports that he facilitated made it easier for these economies to emerge and embrace open markets. The benefits to poorer nations have been huge.

Advertisement So far as the American economy is concerned, however, the Fed's policies of the past decade look like having painful long-term costs. It is true that the economy has shown amazing resilience in the face of the bursting in 2000-01 of the biggest stockmarket bubble in history, of terrorist attacks and of a tripling of oil prices. Mr Greenspan's admirers attribute this to the Fed's enhanced credibility under his charge. Others point to flexible wages and prices, rapid immigration, a sounder banking system and globalisation as factors that have made the economy more resilient to shocks.

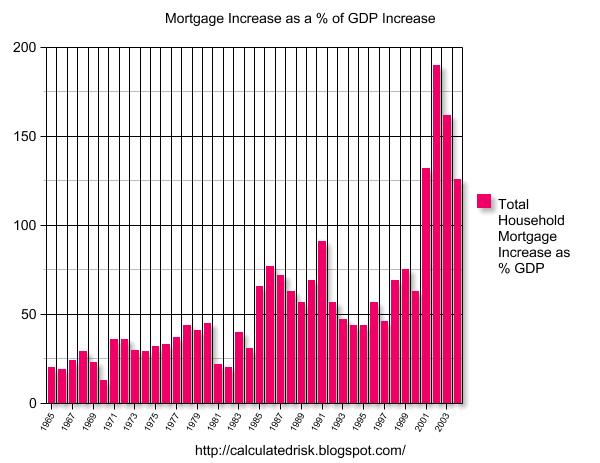

The economy's greater flexibility may indeed provide a shock-absorber. A spurt in productivity has also boosted growth. But the main reason why America's growth has remained strong in recent years has been a massive monetary stimulus. The Fed held real interest rates negative for several years, and even today real rates remain low. Thanks to globalisation, new technology and that vaunted flexibility, which have all helped to reduce the prices of many goods, cheap money has not spilled into traditional inflation, but into rising asset prices instead—first equities and now housing. The Economist has long criticised Mr Greenspan for not trying to restrain the stockmarket bubble in the late 1990s, and then, after it burst, for inflating a housing bubble by holding interest rates low for so long (see article). The problem is not the rising asset prices themselves but rather their effect on the economy. By borrowing against capital gains on their homes, households have been able to consume more than they earn. Robust consumer spending has boosted GDP growth, but at the cost of a negative personal saving rate, a growing burden of household debt and a huge current-account deficit.

Burning the furniture Ben Bernanke, Mr Greenspan's successor, likes to explain America's current-account deficit as the inevitable consequence of a saving glut in the rest of the world. Yet a large part of the blame lies with the Fed's own policies, which have allowed growth in domestic demand to outstrip supply for no less than ten years on the trot. Part of America's current prosperity is based not on genuine gains in income, nor on high productivity growth, but on borrowing from the future. The words of Ludwig von Mises, an Austrian economist of the early 20th century, nicely sum up the illusion: “It may sometimes be expedient for a man to heat the stove with his furniture. But he should not delude himself by believing that he has discovered a wonderful new method of heating his premises.”

As a result of weaker job creation than usual and sluggish real wage growth, American incomes have increased much more slowly than in previous recoveries. According to Morgan Stanley, over the past four years total private-sector labour compensation has risen by only 12% in real terms, compared with an average gain of 20% over the comparable period of the previous five expansions. Without strong gains in incomes, the growth in consumer spending has to a large extent been based on increases in house prices and credit. In recent months Mr Greenspan himself has given warnings that house prices may fall, and that this in turn could cause consumer spending to slow. In addition, he suggests that foreigners will eventually become less eager to finance the current-account deficit. Central banks in Asia and oil-producing countries have so far been happy to buy dollar assets in order to hold down their own currencies. However, there is a limit to their willingness to keep accumulating dollar reserves. Chinese officials last week offered hints that they are looking eventually to diversify China's foreign-exchange reserves. Over the next couple of years the dollar is likely to fall and bond yields rise as investors demand higher compensation for risk.

When house-price rises flatten off, and therefore the room for further equity withdrawal dries up, consumer spending will stumble. Given that consumer spending and residential construction have accounted for 90% of GDP growth in recent years, it is hard to see how this can occur without a sharp slowdown in the economy.

Handovers to a new Fed chairman are always tricky moments. They have often been followed by some sort of financial turmoil, such as the 1987 stockmarket crash, only two months after Mr Greenspan took over. This handover takes place with the economy in an unusually vulnerable state, thanks to its imbalances. The interest rates that Mr Bernanke will inherit will be close to neutral, neither restraining nor stimulating the economy. But America's domestic demand needs to grow more slowly in order to bring the saving rate and the current-account deficit back to sustainable levels. If demand fails to slow, he will need to push rates higher. This will be risky, given households' heavy debts. After 13 increases in interest rates, the tide of easy money is now flowing out, and many American households are going to be shockingly exposed. In the words of Warren Buffett, “It's only when the tide goes out that you can see who's swimming naked.”

How should Mr Bernanke respond to falling house prices and a sharp economic slowdown when they come? While he is even more opposed than Mr Greenspan to the idea of restraining asset-price bubbles, he seems just as keen to slash interest rates when bubbles burst to prevent a downturn. He is likely to continue the current asymmetric policy of never raising interest rates to curb rising asset prices, but always cutting rates after prices fall. This is dangerous as it encourages excessive risk taking and allows the imbalances to grow ever larger, making the eventual correction even worse. If the imbalances are to unwind, America needs to accept a period in which domestic demand grows more slowly than output.

The big question is whether the rest of the world will slow too. The good news is that growth is becoming more broadly based, as demand in the euro area and Japan has been picking up, and fears about an imminent hard landing in China have faded. America kept the world going during troubled times. But now it is time for others to take the lead.

The same book is still being published today. I first remember it showing up in the mid 80s. Garbage.

Probably the guy who wrote it is making a profit, though!

First Plank: Abolition of property in land and the application of all rents of land to public purposes. (Zoning - Model ordinances proposed by Secretary of Commerce Herbert Hoover widely adopted. Supreme Court ruled "zoning" to be "constitutional" in 1921. Private owners of property required to get permission from government relative to the use of their property. Federally owned lands are leased for grazing, mining, timber usages, the fees being paid into the U.S. Treasury.)

Second Plank: A heavy progressive or graduated incometax. (Corporate Tax Act of 1909. The 16th Amendment, allegedly ratified in 1913. The Revenue Act of 1913, section 2, Income Tax. These laws have been purposely misapplied against American citizens to this day.)

Third Plank: Abolition of all rights of inheritance. (Partially accomplished by enactment of various state and federal "estate tax" laws taxing the "privilege" of transfering property after death and gift before death.)

Fourth Plank: CONFISCATION OF THE PROPERTY OF ALL EMIGRANTS AND REBELS. (The confiscation of property and persecution of those critical - "rebels" - of government policies and actions, frequently accomplished by prosecuting them in a courtroom drama on charges of violations of non-existing administrative or regulatory laws.)

Fifth Plank: Centralization of credit in the hands of the State, by means of a national bank with State capital and an exclusive monopoly. (The Federal Reserve Bank, 1913- -the system of privately-owned Federal Reserve banks which maintain a monopoly on the valueless debt "money" in circulation.)

Sixth Plank: Centralization of the means of communications and transportation in the hands of the State. (Federal Radio Commission, 1927; Federal Communications Commission, 1934; Air Commerce Act of 1926; Civil Aeronautics Act of 1938; Federal Aviation Agency, 1958; becoming part of the Department of Transportation in 1966; Federal Highway Act of 1916 (federal funds made available to States for highway construction); Interstate Highway System, 1944 (funding began 1956); Interstate Commerce Commission given authority by Congress to regulate trucking and carriers on inland waterways, 1935-40; Department of Transportation, 1966.)

Seventh Plank: Extension of factories and instruments of production owned by the State, the bringing into cultivation of waste lands, and the improvement of the soil generally in accordance with a common plan. (Depart-ment of Agriculture, 1862; Agriculture Adjustment Act of 1933 -- farmers will receive government aid if and only if they relinquish control of farming activities; Tennessee Valley Authority, 1933 with the Hoover Dam completed in 1936.)

Eighth Plank: Equal liability of all to labor. Establishment of industrial armies especially for agriculture. (First labor unions, known as federations, appeared in 1820. National Labor Union established 1866. American Federation of Labor established 1886. Interstate Commerce Act of 1887 placed railways under federal regulation. Department of Labor, 1913. Labor-management negotiations sanctioned under Railway Labor Act of 1926. Civil Works Administration, 1933. National Labor Relations Act of 1935, stated purpose to free inter-state commerce from disruptive strikes by eliminating the cause of the strike. Works Progress Administration 1935. Fair Labor Standards Act of 1938, mandated 40-hour work week and time-and-a-half for overtime, set "minimum wage" scale. Civil Rights Act of 1964, effectively the equal liability of all to labor.)

Ninth Plank: Combination of agriculture with manufacturing industries, gradual abolition of the distinction between town and country, by a more equitable distribution of population over the country. (Food processing companies, with the co-operation of the Farmers Home Administration foreclosures, are buying up farms and creating "conglomerates.")

Tenth Plank: Free education for all children in public schools. Abolition of children's factory labor in its present form. Combination of education with industrial production. (Gradual shift from private education to publicly funded began in the Northern States, early 1800's. 1887: federal money (unconstitutionally) began funding specialized education. Smith-Lever Act of 1914, vocational education; Smith-Hughes Act of 1917 and other relief acts of the 1930's. Federal school lunch program of 1935; National School Lunch Act of 1946. National Defense Education Act of 1958, a reaction to Russia's Sputnik satellite demonstration, provided grants to education's specialties. Federal school aid law passed, 1965, greatly enlarged federal role in education, "head-start" programs, textbooks, library books.

He has made tons of money. He seems to be recession proof.

Yeah for a while I though we won the cold war, little did I know

There's always money to be made predicting the end of the world as we know it.

Yep. Cookbooks also.

Hmmmm...."Recipes to Save You During the Coming Recession"

I like it.

Refining the Title a bit:

Elvis's and JFK's Recipes to Save You During the Coming Recession"

There, that's better.

Excellent. Apocalypse for Dummies.

Okay, now you've really touched all the bases, Tex. I'm okay, you're okay, JFK's okay.

What a meaningless statement. The vast majority of US workers are essentially REQUIRED by the government to invest via 401K if they have any hope of retiring. My 401k does not permit investment in gold (which is up 30% in a year) and doesn't even have bonds, only bond funds. Absurd? Yes. Reality? Yes. If I lost all my money I would be terrbily harmed, I would essentially have no hope of ever retiring.

I love it!

There are 103 different toxic carcinogens in second hand smoke (depending on who's numbers...), plus 5 billion illegal immigrants in Butte Montana alone and 350 communists in the State Department, and ...

One difference that I see is that bouts of inflation followed by bouts of deflation will often get you right back where you started from. Thus depending on which point on the graph you picked your money could be worth more, or less, or a lot less. If you averaged it all out it might be close to flat.

The situation more recently is inflation, all the time. Deflation is explicitly not permitted. The new head of the Fed famously said we can prevent deflation because of this invention called the "printing press" and that we would "throw money out of helicopters" if we needed to.

So things are different now from the 19th century. For most businesses a low stable inflation rate works better than wildly varying rates of inflation / deflation. But it also does erode the value of money over time.

I think both you and the person you're arguing with are both right to some extent.

|

That's because non-bankers see mortgages as liabilities and homes as assets. Fine. Let's add up total home equity, subtract total mortgages, and while we're at it we can also figure in all other privately held assets and debts and then we can look at total family net worth. We can also adjust for inflation and crank it all out to constant 1993 dollars. That shows us that over the past quarter century the total net worth in America has almost doubled.

I realize that most people hate it when someone brings out the good with the bad, especially when they find out that most people are actually better off; OK, I hate to shine sunlight on anyone's soggy parade, but facts are facts. Maybe as a consolation I can share the fact that every six seconds an American dies. How about that! Just think, if it took you three minutes to read this then somewhere there's a whole room full of 30 newly dead Americans!! Well, maybe you've figured out that 33 were born too giving us a net gain.

That's why this environment schtick is so great -- for complainers that is. With 300 million Americans each putting out 50 gallons of raw sewage per day, then every DAY the US is pooping out A LAKE OF PURE SEWAGE a quarter of a mile across and over 500 feet deep!!!!

Yum!

What Mulder said was that Americans "were doing just fine without the Federal Reserve, as prices were stable for 150 years". That's crazy. Your statement was correct, that double digit inflation one year followed by double digit deflation the next year will "get you right back where you started from" --only because we all start out the same way: naked, starving, and crying.

Phasing in the FRB in the 20th century turned night into day. Personal disposable income took off, employment soared, and when you really look at the trends you also notice something much more important-- we dropped the wild swings and life became so much more steady. My dad grew up in pre-FRB times and the stories of boom/starvation in the mid-west in the early 1900's were painful just to listen to. IMHO, only a fool or the criminally insane would ever want to risk bringing back that way of life.

Lots of other things changed between 1900 in the midwest and post 1913 America. I think it's wrong to attribute to much to the Fed, either negative or positive. A lot of the boom / bust was tied to agriculture, which didn't benefit from electricity much, and therefore immigration. Certainly the "National Bank" period when there was no central bank was filled with problems. But then the Great Depression took place 20 years AFTER the Fed. Again, economies are big complex systems that defy simple cause and effect explanations. This is why economics is called 'the dismal science'.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.

{kind=link}

{kind=link}