I would respectfully disagree.

Posted on 12/09/2022 6:54:18 AM PST by LouAvul

For a year?

I think it depends. Even at 80 years of age, many of us, particularly women, will have 15 or more years to live. With this in mind:

If you are depending on the entirety of your investments to provide income in your old age, then yes, I would agree that you need to protect your investment with conservative no risk or very low risk investments. On the other hand, if you only need a portion of your investments, let's say 50%, to produce income, you could allow the other 50% to remain in higher risk investment categories. IMHO.

“There are other alternatives such as CD’s...”

I used to complain CDs only paid 11% or 12%...this was back in the day when Jimmy Carter’s prime rate was 21.5%. I wished I would have gotten CDs for 100 year terms now (yeah, I know they would have been called—but still).

Lotsa experts around. I’ll offer up a lifetime of truisms.

1) Loss is more mathematically powerful than gain. If you have $1 and lose 50% of it, you have 50 cents. If you then gain 50%, you are not back to where you started. You have 75 cents. It works in both directions. If you have $1 and gain 50%, you have $1.50. If you then lose 50%, yup, 75 cents. Don’t lose money. Any time you want to take a risk, be sure it is 2:1 more likely to rise than fall. This is rare.

2) Never confuse wisdom with a bull market. You will always be able to find people who are experts and can tell you what to do — and they will usually present a track record of gains, all achieved in years of up markets.

3) There are no gurus. None. Nobody is worth following.

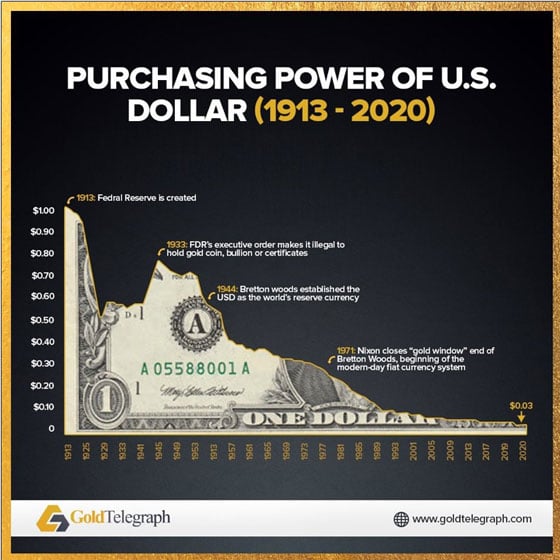

4) Never ever forget you are measuring success in a substance created from nothingness by central banks. Because it is a meaningless substance, there are no laws of economics. Supply and demand is not valid. Capitalism is not valid. Socialism is not valid. All the isms are measured by a substance created from nothing. How can there be meaning to that?

5) Value is physical. Not imaginary. Calories in crops are not imagined. Joules in oil are not imagined. The price of a share of Procter and Gamble . . . determined by the imagination of counterparties.

I would respectfully disagree.

There’s a thing called a Series I savings bond, NOT a Treasury bill, which adjusts every SIX months, and was paying 9.12 percent and is now paying somewhere north of 6. It has a 10K per year limit. It has a three year maturity but you can cash out after a year, but you’ll lose three months interest if you cash out before the three years is up.

Even if you cashed out after a year and gave up three months of interest you’d be beating the pants of any one-year CD you could get.

Is that what you got?

T bills onto have an actual rate. They are discount instruments. Buy at 95 mature at 100 at the end date. So it depends on the length o ivestment up to 1 year and the current offer price.

Yes, that is what I bought.

Currently 6.89%.

$10K max investment per person per year.

At the time I bought it, I thought it was better than putting another $10K in the stock market.

I remember those days.

Plus, they gave you a toaster oven or your choice of small household appliances when you opened an account at the bank.

I have a Panasonic clock radio from then that still works today.

One year t bills are a good way to go. Right now you can get 4.7% on them vs 4.8 on CDs.

The difference is that the interest on t- bills is free of state income tax, and any appreciation is taxed as a long term capital gains tax if held more than a year.

I’m going with t-bills.

“They adjust monthly based on the inflation rate. Maximum per person/year is $10K.”

I bought some too.

The interest rate adjusts every 6 months.

You also cannot cash them out the first year and there is a penalty if you cash them within the first 5 years.

The answer depends on what your objectives are. If you are first and foremost looking to preserve the principal amount invested, then T-bills are extremely safe in that regard. You will get the value at maturity, and the implicit rate of return. BUT - they will not protect your purchasing power if the rate of inflation is higher than the rate of return.

If you are attracted by the now-higher rate of return (due to inflation), where do you think rates will be at maturity when it is time to reinvest?

If you think rates will go up from here, taking the rate now and then reinvesting later at a higher rate is better than taking a longer duration now and a (presumably) lower rate. You're then "stuck" with a lower rate for longer.

If you think rates will be lower a year from now, then locking in a higher rate for a longer term would be the better choice.

Both of these choices are complicated by the fact that the "yield curve" is inverted - meaning that short-term rates are higher than long-term rates. This doesn't happen often but, when it does, it's viewed as an indicator of an impending recession (or worse).

If your choice is to take a 1-year CD vs. a 1-year T-bill, and the T-bill is currently at a higher yield that the CD, then take the T-bill. If the CD yield is higher, then go that way. Note that FDIC insurance covering your CD is for your principal amount - exclusive of the interest earned. So, theoretically, there's more risk in the CD over the same period. In reality, I've not seen mass bank failures and the FDIC having to cover deposits in a very long time.

“Their price has dropped 22% in the past year. Are they chewing up their capital to get that 11% dividend or have they just been hit like other stocks.”

Yes, you have to be real careful about what that dividend consists of. Often a big chunk of it is the money you put in. Closed end funds are notorious for that. I don’t know about ABR, which is a REIT - I don’t think they play those games.

For a year?

Definitely!

For 1981!

Regards,

Great investment advice

Some banks would give you a new shotgun for opening an account.

Sorry replied by phone before and had too many typos. T-Bills are discount instruments. They don’t pay interest but yield a return. At maturity they are worth 100%. So if you buy at .95 for a 6 month bill, you get 100 at maturity. Every day after issue the demand plus the number of days left to maturity will influence the price, closer to maturity closer to 100. There are other factors but it can be complex to explain in detail. Hope that helps.

Thank you.

.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.