Risk free returns (10 year T-Bill) is at 1.5%. A 5% return is only attainable with a pretty heavy exposure to equities which carry a lot of downside risk.

The current risk-free return of 1.5% is entirely eaten up ENTIRELY by annual inflation, so your REAL annual return is ZERO.

Your success in retirement if you are heavily invested in equities depends to a huge extent on the performance of the stock market during your first two or three years of retirement. If you retire into a bear market and lose a lot of principal, you will never earn it back. If you retire into a bull market and your savings grow, you will be in clover. So, if you are counting on the stock market to fund your retirement, much is out of your control. Some people will retire into a bull market and enjoy a prosperous retirement; others will retire into a bear market and have to pinch pennies throughout retirement.

Maybe you are familiar with "Monte Carlo Simulations." These are mathematical simulations of events with known (or estimated) probabilities. I highly recommend the use of the "Portfolio Visualizer Monte Carlo Simulation" to simulate how your portfolio will do in retirement. "This Monte Carlo simulation tool provides a means to test long term expected portfolio growth and portfolio survival based on withdrawals, e.g., testing whether the portfolio can sustain the planned withdrawals required for retirement."

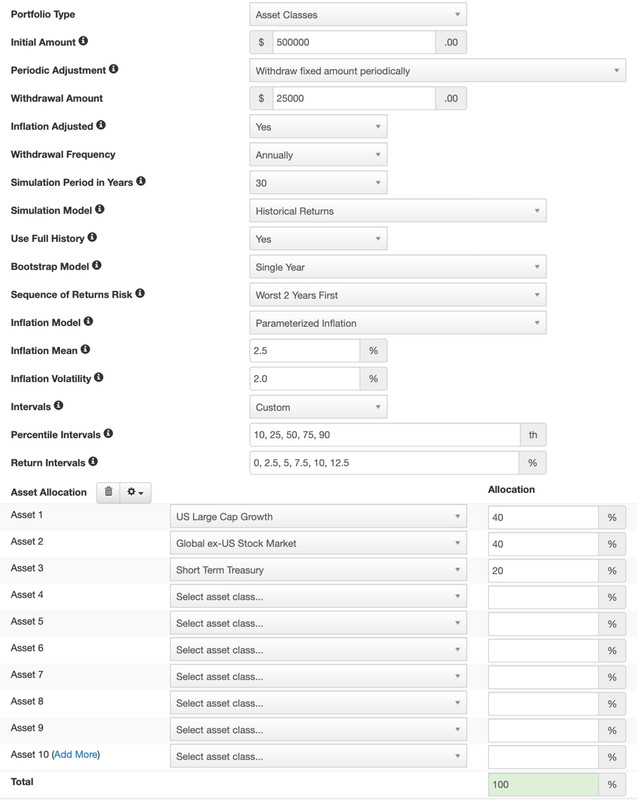

It includes a parameter they call "Sequence of Returns Risk" which lets you specify how bad the first X years of your retirement will be financially. You specify the "Worst X Years First" where you are saying those first years will be your worst returns in your retirement.

It includes many asset classes grouped into U.S. Equities, International Equities, Fixed Income, and Other and you can select a portfolio risk level. You can also model different rates of inflation.

If you have limited financial skills or no understanding of simulations and financial modeling, perhaps you could enlist a friend or financial advisor to set up the model and run it for you.

The other extremely important thing to do is create a detailed spreadsheet of all your sources of income, expenses, and expected financial returns on your investment. The single biggest expense that bites people in retirement is health care. You live your life out being reasonably healthy with few major problems and expect that to continue in retirement. But it doesn't work that way. Health can deteriorate seriously and quickly as we age and those expenses can be huge.

Here's a screen cap of the setup of Portfolio Visualizer Monte Carlo Simulation. I set up your $500,000 savings split 40% in US equities, 40% in International equities, and 20% fixed income. I specified we are going into a two-year bear market.

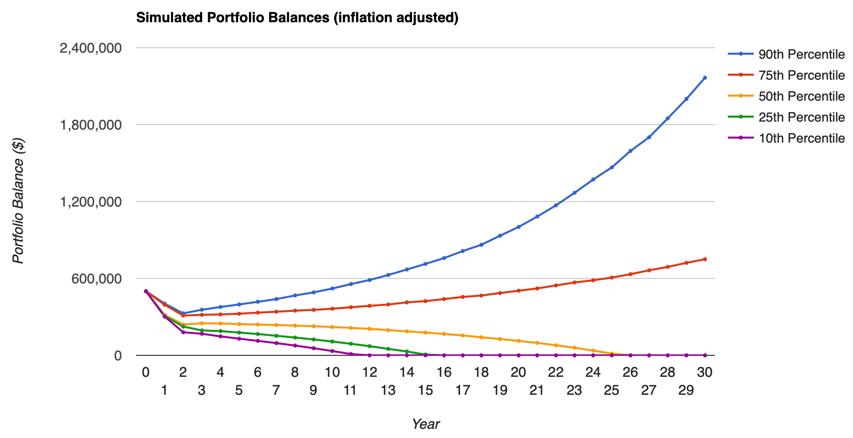

Here are the results. At the median case and withdrawing $25,000 per year, your savings are exhausted at year 26. Note that this model does not provide the flexibility to withdraw a large amount at a given year to deal with emergencies such as health care.

Until you develop a more concrete plan and model it mathematically as I've suggested above, there is really no way to say if you can make it on $500k. This is not something you want to do on the back of an envelope. A detailed spreadsheet model of your next 30 years will help provide guidance on where you can afford to live and how well you'll do in retirement.

If your $500k is invested with a company like Fidelity, you can get good, free retirement planning from them as well as recommended stock portfolios that match your risk tolerance. You might find that your investment company can run the Monte Carlo Simulations for you. My company does that, but I prefer doing it myself with the "Portfolio Visualizer" tool I linked to above.

The last thing is do not underestimate the ability of inflation to eat away at your savings. A mere 2% inflation rate will, over 30 years, wipe out 80% of your spending power (if you got 0% on your investment). If you put your $500,000 into a 10 year T-Bill, spent none of it, and inflation was the same as your T-Bill rate, you would have $500,000 of purchasing power (in today's dollars) left. But, if inflation ran 1.0% higher than your T-Bill rate, you would have $362,000 left in today's purchasing power.

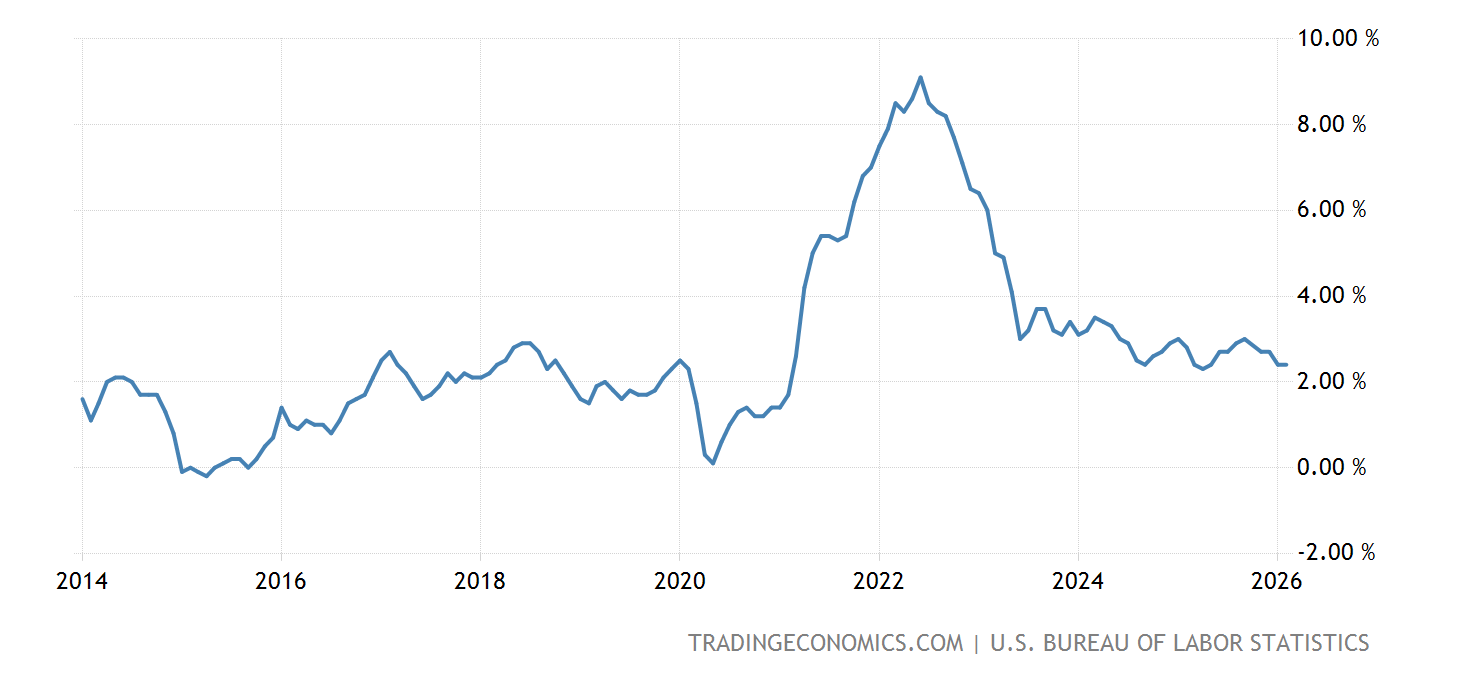

The chart below shows United States inflation the past five years: