Skip to comments.

New Study Finds CRA 'Clearly' Did Lead To Risky Lending [Daniel 4]

Investor's Business Daily ^

| 12/20/2012

| PAUL SPERRY

Posted on 08/04/2015 7:52:58 AM PDT by Jan_Sobieski

Democrats and the media insist the Community Reinvestment Act, the anti-redlining law beefed up by President Clinton, had nothing to do with the subprime mortgage crisis and recession. But a new study by the respected National Bureau of Economic Research finds, "Yes, it did. We find that adherence to that act led to riskier lending by banks."

Added NBER: "There is a clear pattern of increased defaults for loans made by these banks in quarters around the (CRA) exam. Moreover, the effects are larger for loans made within CRA tracts," or predominantly low-income and minority areas. To satisfy CRA examiners, "flexible" lending by large banks rose an average 5% and those loans defaulted about 15% more often, the 43-page study found.

The strongest link between CRA lending and defaults took place in the runup to the crisis — 2004 to 2006 — when banks rapidly sold CRA mortgages for securitization by Fannie Mae and Freddie Mac and Wall Street. CRA regulations are at the core of Fannie's and Freddie's so-called affordable housing mission. In the early 1990s, a Democrat Congress gave HUD the authority to set and enforce (through fines) CRA-grade loan quotas at Fannie and Freddie.

It passed a law requiring the government-backed agencies to "assist insured depository institutions to meet their obligations under the (CRA)." The goal was to help banks meet lending quotas by buying their CRA loans...

(Excerpt) Read more at news.investors.com ...

TOPICS: Business/Economy; Government; Miscellaneous; News/Current Events

KEYWORDS: cra; mortages; mortgages; recession; socialism; subprime

Navigation: use the links below to view more comments.

first 1-20, 21-25 next last

Daniel 4: 10 Thus were the visions of mine head in my bed; I saw * , and behold a tree in the midst of the earth, and the height thereof was great. 11 The tree grew , and was strong , and the height thereof reached unto heaven, and the sight thereof to the end of all the earth: 12 The leaves thereof were fair, and the fruit thereof much, and in it was meat for all: the beasts of the field had shadow under it, and the fowls of the heaven dwelt in the boughs thereof, and all flesh was fed of it.

The federally subsidized Community Reinvestment Act forced banks to make loans to unqualified borrowers. Under the auspices of "unfair housing practices", the Obama administration has inherited this mantle and works feverishly to continue building our new socialist utopia.

For centuries, the leftists have yearned to build this paradise, with other people's money of course. The great omniscient, omnipotent, all-loving (except babies) government tree that provides everyone free housing, free food, free car, free phone, free college, or any other government handout (as long as you vote for them) in order to implement their utopian progressive agenda.

Socialist utopias always fail. Eventually the Jacobins run out of other peoples money, or kill one too many good people, or are replaced by an even worse group. Regardless, the tree is always cut down. In 2008 we had a partial collapse of this system, but we have managed to print our way out. Little has changed since 2008. Nebuchadnezzar became the greatest sovereign the world has ever known. He erected a government tree that promised "cradle to grave" help for all...until the house of cards came crashing down...

Daniel 4: 22 It is thou, O king, that art grown and become strong: for thy greatness is grown, and reacheth unto heaven, and thy dominion to the end of the earth. 23 And whereas the king saw a watcher and an holy one coming down from heaven, and saying , Hew the tree down, and destroy it; yet leave the stump of the roots thereof in the earth, even with a band of iron and brass, in the tender grass of the field; and let it be wet with the dew of heaven, and let his portion be with the beasts of the field, till seven times pass over him;

To: Jan_Sobieski

What is the use? No matter how many people go ahead and spend their time actually researching something, the Marxists just say “no it’s not, you racist” and we keep on acting like it’s not.

There is no truth, only competing agendas.- soviet propaganda

2

posted on

08/04/2015 7:58:28 AM PDT

by

thorvaldr

To: Jan_Sobieski

3

posted on

08/04/2015 8:00:40 AM PDT

by

US Navy Vet

(Go Packers! Go Rockies! Go Boston Bruins! See, I'm "Diverse"!)

To: thorvaldr

Democrats and the media insist the Community Reinvestment Act, the anti-redlining law beefed up by President Clinton, had nothing to do with the subprime mortgage crisis and recession. But a new study by the respected National Bureau of Economic Research finds, “Yes, it did. We find that adherence to that act led to riskier lending by banks.”

Nothing is ever the Democrats fault. We can never criticize their policies or the results of their programs. We can never point out the bad results of their programs after they have been around for a number of years.

Since Democrats are liberal and always have the best of intentions with their policies, we are not supposed to talk about failures or alternatives.

Sarcasm.

To: thorvaldr

ironic isn’t it? In the information age, truth somehow is lost in the mix.

5

posted on

08/04/2015 8:03:11 AM PDT

by

refermech

To: US Navy Vet

Here is the thing...everyone is greedy (like Milton Freidman so eloquently stated) But in a free-market, few will act against self interest, unless coerced. CRA coerced, under great penalty, banks to make loans to unqualified people and subsidized them through Freddie and Fanny. To say the banks caused this is exactly what the socialists want us to believe. They say, this "free market" thing does not work!?!? It does, if you don't pass laws that destroy it!

6

posted on

08/04/2015 8:07:18 AM PDT

by

Jan_Sobieski

(Sanctification)

To: thorvaldr

I agree! But we have to keep telling the truth till the end. Even if we and our family (like Noah) are the only ones saved out of this lunacy.

7

posted on

08/04/2015 8:08:32 AM PDT

by

Jan_Sobieski

(Sanctification)

To: Jan_Sobieski

>>banks to make loans to unqualified people and subsidized them through Freddie and Fanny. There's no doubt the CRA had an impact upon opening Pandora's box - but what the RINOs fypically fail to admit is the fact that the "revolutionary" Subprime operation owned by their Shrubbery's Ambassador to the Netherlands (AKA the Godfather of Subprime) wasn't a bank, and the products it originated NEVER qualified for Freddy/Fannie "subsidization" (at least not as of April/May 2007 when the CIO told the company's associates they were still very interesting in qualifying for Freddy/Fannie, but still didn't).

"Oops"

"Oops"

8

posted on

08/04/2015 8:29:54 AM PDT

by

HLPhat

(This space is intentionally blank.)

To: HLPhat

Definitely bi-partisan. History repeats itself. Daniel 4 is being replayed...

9

posted on

08/04/2015 8:37:33 AM PDT

by

Jan_Sobieski

(Sanctification)

To: Jan_Sobieski

A more compelling penalty was that banks were going to be kept off the post-Gramm-Leach-Bliley “financial services” gravy train, if they didn’t score high enough on their CRA “exam.”

10

posted on

08/04/2015 8:41:44 AM PDT

by

Trailerpark Badass

(There should be a whole lot more going on than throwing bleach, said one woman.)

To: HLPhat

I *think* you are saying, and if so, I will agree in advance, that the 2007-2008 crisis was caused in two phases. Phase I is the CRA encouraging subprime and subdirt loans, coupled with the loosening of underwriting standards at FNM/FRE.

For many years, there was this term “conforming” as applied to loans. That term meant that the loan met strict (VERY strict) underwriting standards and had known, proven (very very low) historical default rates and was therefore a tasty investment item for institutions, domestic and international. EVEN THOUGH on the very front page of Fan and Fed prospectuses was in LARGE LETTERS “this is not an instrument of US Govt debt and is not US Govt guaranteed” that debt was UNIVERSALLY taken as govt guar’ed.

The second phase of the collapse was engendered by the originating banks and mortgage wholesalers, who saw they could write morts of worse and worse and worse quality, patch them together with mort insurance policies of higher and higher prices covering more and more hinkyness. And no matter how bad the stench from these items, they could be passed on to FNM/FRE. Either by welding a mort ins policy to them which the originator forced the borrower to buy, OR, by burying the most fetid items in bundles of less fetid items.

The lending environment became what Bill Black calls “criminogenic”, eg; encouraging criminal activity, in this case fraud. Because banking and mortgage co execs were paid based upon performance, if they wrote worse and worse morts, then they could boast their performance was booming, capture the pay for performance, and nobody was the wiser after these turd-loans were thrown into vast pools. Or, in many cases, their stock responded to massive growth trajectories [”doubling every quarter”] and they were paid in options or stock which further incented them to goose their performance by writing crapola loans. If you’ll remember, these companies were posting internet-stock-grade growth rates....and they were certainly retaining nothing for FNM/FRE put-backs. (eg; FNM/FRE forces the originator to take back crap loans if they go bad w/in 18 months) The idea was to write as many loans in 18 months as you had ink and borrowers of any kind at all.

To: Jan_Sobieski

Cuomo, Frank, Clinton, Brown, and all the Dems have mud on their hands and faces for the CRA..

12

posted on

08/04/2015 9:06:21 AM PDT

by

NormsRevenge

(SEMPER FI!! - Monthly Donors Rock!!)

To: thorvaldr

You are right, thorvaldr, systematic lying is impervious to the truth.

13

posted on

08/04/2015 9:09:57 AM PDT

by

samtheman

(Trump/Cruz '16)

To: Attention Surplus Disorder

>>And no matter how bad the stench from these items, they could be passed on to FNM/FRE.

But the products manufactured by [one time Subprime LEADER] Ameriquest/Argent Mortgage never qualified for FNM/FRE.

From what I was able to observe, they “revolutionized” the market by securitizing 100% of their A$$paper and flushing it into the global economic sewer system before anybody figured out the fraudulent flaws in “the model”.

Though it’s sort of an understatement to blame 2008 on “flaws in the model” — when the “flaws” were the result of the FAILURE to review little things like the FICO scores that were manufactured out of thin air for thousands of the originations...

The SEC could tell you about that — well, if they could find their own arse with both hands and a SQL statement telling them exactly where to find it (and those originations in Argent’s production Empower DB ), that is.

Got Systemic Corruption?

14

posted on

08/04/2015 9:12:44 AM PDT

by

HLPhat

(This space is intentionally blank.)

To: HLPhat

So you’re just saying that A’quest figured out another way (bypassing F/F) to bundle and securitize their crud....which was the main market function FNM/FRE performed before such advanced engineering took place. I guess that’s where much of the Lehman and Bear paper came from?

It sure was infinite back then, wasn’t it? Everybody sold garbage, with a repair kit included, and everybody made money at every step when there really wasn’t any money in the pot to begin with! Magical.

I worked very briefly at a mort bucket shop right at the peak, I heard stories of originators making $20K, $26K for the most ridiculous mortgages imaginable. Later, I moved into selling homes, including some foreclosures. There were folks who had bought crappy 1951 1350 sq foot homes for $449K with $1K/mo starter payments that went to $3.1K in a year, their GROSS income had never exceeded $1700/month. It was beyond stupid.

Got Systemic Corruption? <——exactly.

To: Attention Surplus Disorder

16

posted on

08/04/2015 9:49:05 AM PDT

by

HLPhat

(This space is intentionally blank.)

To: Jan_Sobieski

>>Definitely bi-partisan.

Yep. Best RATs and RINOs money could buy.

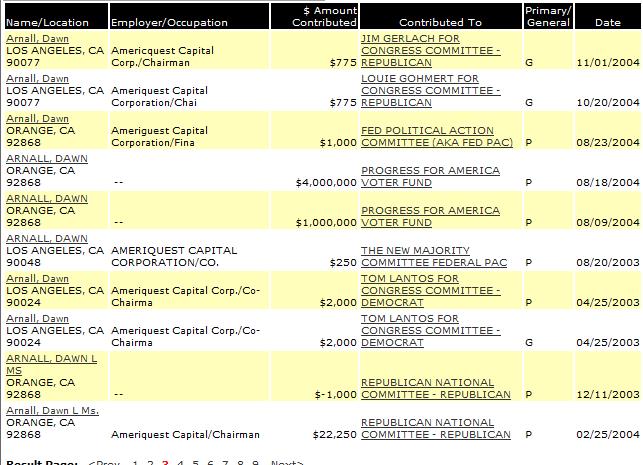

On the Right we can see the Shrubs and the Arnalls, and on the left, well — Just ask the present Secretary of Commerce how her Chicago family-owned Superior Bank went kapudt following its innovations in ACORN farming.

17

posted on

08/04/2015 9:53:10 AM PDT

by

HLPhat

(This space is intentionally blank.)

To: HLPhat

I’m not totally ignorant about how the banking system works, but as they say about a little knowledge.

I have a question. Been in the automobile business since ‘92. Taken thousands of credit applications. At one time a majority of my customers had their mortgages sold by the originating bank. And often resold. And resold again. This practice has pretty much, not totally, but pretty much been ended since the crash.

Why were the banks selling and were these loans “bundled”. And if bundled then they could be broken up and rebundled and sold again? The bank of record still owned the paper but bundled them as securities?

18

posted on

08/04/2015 10:30:31 AM PDT

by

saleman

(?)

To: saleman

Put on steroids by Cumo

To: saleman

>>And if bundled then they could be broken up and rebundled and sold again?

And again, and again, and...

Until...

http://www.google.com/search?q=mers%20cannot%20assign%20mortgage&rct=j

Ooops!

>>The bank of record still owned the paper but bundled them as securities?

Per the MERS fiasco - who is the “bank of record”?

In some cases the originator retained the servicing of the loan (and collected fees for doing so) but flushed the loan (and the investment exposure to it) down stream.

The originator and their “warehouse lender” can often ...

http://www.google.com/search?q=Argent+Deutsches+bank

... still be observed swimming in the chummed waters.

I’d expect the entire process is managed and sorted through by lawyers who interpret the structure of the securitized legal instruments involved — sort of like the bacteria in a colon.

20

posted on

08/04/2015 11:12:01 AM PDT

by

HLPhat

(This space is intentionally blank.)

Navigation: use the links below to view more comments.

first 1-20, 21-25 next last

Disclaimer:

Opinions posted on Free Republic are those of the individual

posters and do not necessarily represent the opinion of Free Republic or its

management. All materials posted herein are protected by copyright law and the

exemption for fair use of copyrighted works.

FreeRepublic.com is powered by software copyright 2000-2008 John Robinson