Posted on 12/12/2014 6:25:55 AM PST by coloradan

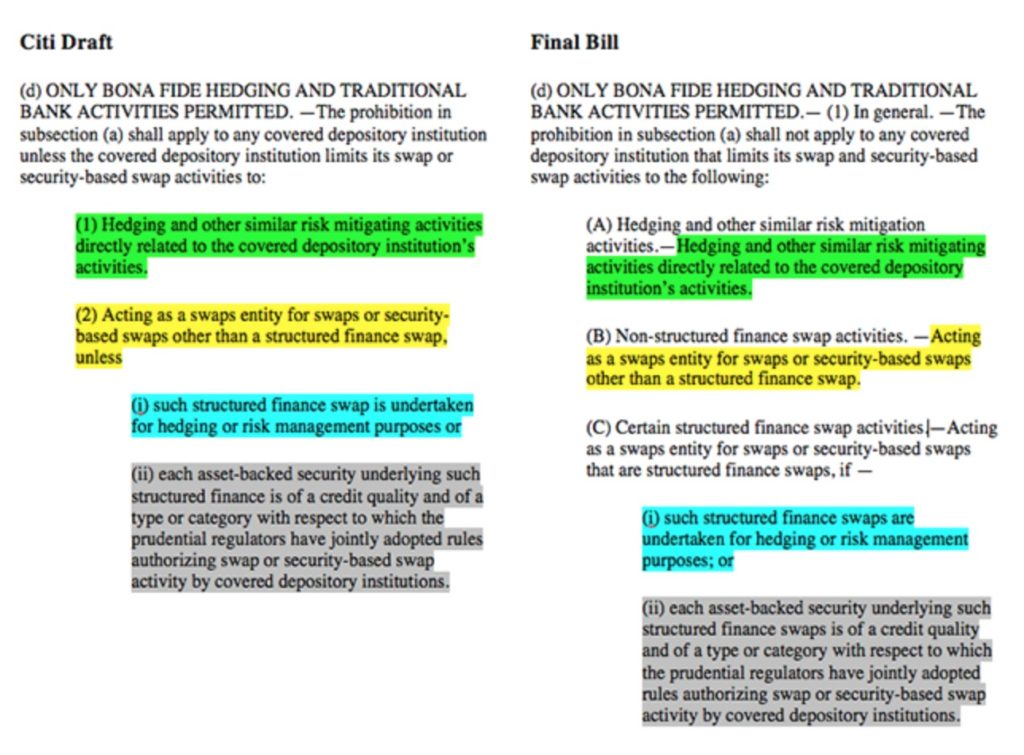

Courtesy of the Cronybus(sic) last minute passage, government was provided a quid-pro-quo $1.1 trillion spending allowance with Wall Street's blessing in exchange for assuring banks that taxpayers would be on the hook for yet another bailout, as a result of the swaps push-out provision, after incorporating explicit Citigroup language that allows financial institutions to trade certain financial derivatives from subsidiaries that are insured by the Federal Deposit Insurance Corp, explicitly putting taxpayers on the hook for losses caused by these contracts. Recall:

(more at link)

(Excerpt) Read more at zerohedge.com ...

It looks like that the banks that trade the derivatives are off the hook making a disagreement between the originator and the buyer fall back on the originator rather than the middleman, “the bank”.

It just makes the task of the plaintiff’s lawyers taks harder because he can’t go after the deep pocketed middleman to collect his fee

(A: Bankers own both sides of government and use it to fleece the general public for their own enrichment, something loggers and electricians, etc., have not been able to do. This has traditionally been cured with lamp posts, which have gone unused for a little too long at this point.)

Well, I guess it’s time the Native American reclaimed the land us greedy palefaces stole from them...

Ohio - of interest ping

I’ve read elsewhere that the total amount of derivatives out there is anywhere between $600 trillion to $1 quadrillion.

Good to know we are on the hook for only $300 trillion of it!

LOL!

So what?

The Bears are worth $1.7 billion and the Saints are worth $1.11 billion.

If I place a $10 bet on Monday's game, the notional value is $2.81 billion but all I can lose, or win, is $10.

Should I worry?

I am just saying that, banks using derivatives and swaps as addressed in the text, is definitely NOT "speculation". If there is $300 trillion in notional derivatives/ swaps in the market, no doubt there likely is a very large amount that IS structured in a speculative way. I am not taking up for that, and certainly not for a bailout of any of it. But allowing derivatives and swaps to be used for true hedging and risk reduction strategies is a very good thing.

Swaps and derivatives are not innately evil when put to the correct use. The problem was that they were used for speculation and gambling. Honestly do away with "too big to fail" and re-institute market discipline to the large banks and the landscape will change quickly. Permitting gambling on the taxpayer dime is just flat evil. But we should not throw the baby out with the bathwater. The result would be either an elimination of banking services or an increased cost to the consumer. There are plenty of other absurd regulations that are doing that already.

A better example is the opposite. There’s a $10 bet on the table, but millions of people are betting on the outcome of the bet, (”I’ll bet you a thousand dollars that Joe is going to win the $10.” and he takes out a thousand dollar insurance policy just in case he loses. The insurer takes out another policy with someone else, just in case they have to pay. Etc.) Such that millions of dollars are going to change hands depending on the outcome of the play. However, not a single player can pay all his obligations unless all the other players do as well. If one of them blows up, like, insurer #3 goes bankrupt, then player #2 isn’t covered, in which case #1 can’t collect as well. What the language appears to do is place all these thousands of dollars of insurance and counter-insurance on the taxpayer. I’m not good with that, it is not within the scope of Constitutional government.

The person betting a trillion dollars on a hedge, which he can’t possibly pay, but he nevertheless seeks to collect the premiums from, most certainly is speculating. If the bet wins, he pockets the premium. If this bill passes, if he loses, the taxpayers pay out on his contract.

I’m surprised the charade has lasted this long. Prepare now while you still can.....

OK, it is clear you don’t want to understand the real situation more clearly. I’m done with you. Have a good day.

“$300 trillion notional backed by about 350 million Americans is just under $1 million for every man, woman and child in the country.”

No problem, after hyperinflation kicks in that will be about 1 hours paycheck for those still employed.

The biggest to big to fail bank is the Federal Reserve.

After an audit they should be broken up and it’s legitimate functions taken over by the Treasury Department.

Want to know who has the power? Just Google the number of stories about the FR vs. the Treasury Dept.

Ok, ignoring my own posts, please refute the argument as presented by Zerohedge. Why is it wrong?

http://www.occ.gov/topics/capital-markets/financial-markets/trading/derivatives/dq114.pdf

Lots of good info at that link.

As I explained, ALL of the derivative market is DEFINITELY NOT SPECULATIVE, but a very legitimate means of REDUCING RISK, not assuming more risk. Most often, this involves a hedge to protect against interest rate risk where a bank is exposed to an increase or decrease in interest rates for a class of assets or liabilities that they have on their books that got there in the normal course of lending money and/or taking deposits. THAT, in my view, is what the legislation is saying as posted in the article. There is not one thing under the sun wrong with that. To the contrary, it is a good and acceptable business practice and is the polar opposite to speculative derivative and swap trading. What often happens is that another entity needs to hedge in the opposite direction, so the transaction reduces risk two the entities on each side of the swap or derivative. A swap in that case is mutually beneficial: they BOTH get something positive out of the transaction.

Again, derivatives used to move a lender’s credit risk off its balance sheet is not a good thing. The reason: there is no way for the entity assuming the credit risk to lay it off, like a bookie does, other than by passing it along to another entity at a fee spread. Somebody ALWAYS takes the loan loss, which is never good. As with AIG, they assumed more credit risk than they could handle. Then, when the economy fell apart, loans started going bad right and left and AIG and others could not cover the credit losses that they effectively guaranteed for other banks. That part of the derivative market, in my opinion, should have been killed and AIG should have been allowed to fail.

However, NOT ALL DERIVATIVE OR SWAP TRANSACTIONS ARE CREATED EQUAL. Some uses are effectively gambling (credit guarantee derivatives) and some uses are very good business practices. It is the same logic as why we don’t outlaw cars because someone gets killed in a wreck. The problem comes when the taxpayer has been covering the risk from SPECULATIVE transactions, which is stealing from the taxpayer. I have no problem limiting speculative transactions, which is what traditional bank regulation has done.

Using derivatives and swaps for banks and insurance companies to hedge and reduce interest rate risk absolutely should be permissible, as the excerpt posted indicates in my reading.

Zerohedge makes the case that what matters is not net exposure, but gross exposure, because if some of the parties blow up, others are then on the hook for the full face amount of the hedges, because they would then be impossible to net out. If John lends Bob $1,000,000, but takes out an insurance policy with Sue for $1,000,000 against risk of loss, John’s net is basically zero. But if Sue goes bankrupt, John becomes unhedged and becomes on the hook for the full million.

First, I think you are arguing against my position again, not Zerohedge’s. Second, I think you might be might be misunderstanding my position. I never said that all swaps or derivatives were bad (and, should be prohibited). I support voluntary contracts between consenting adults. However, I don’t think taxpayers should be on the hook for any of them. I will concede that not *all* such things are speculative, but if there are $300 trillion, or rather, $1 quadrillion, notional, of such contracts out there, by far the overwhelming majority *must* be speculative, because there isn’t enough underlying economic productivity to support that much notional in legitimate hedging activity. I agree with you that AIG should have been allowed to fail, and for that matter Fannie and Freddie too. I am concerned that the present bill, if passed, will set up the situation for a much larger repeat of the TARP in 2008.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.