Posted on 08/11/2014 9:07:54 AM PDT by Kaslin

With all the controversy over the failed and costly Obamacare program, it’s understandable that other entitlements aren’t getting much attention.

But that doesn’t mean there aren’t serious problems with Medicaid, Medicare, and Social Security.

Indeed, the annual Social Security Trustees Report was released a few days ago and the updated numbers for the government-run retirement program are rather sobering.

Thanks in part to sloppy journalism, many people only vaguely realize that Social Security is actuarially unsound.

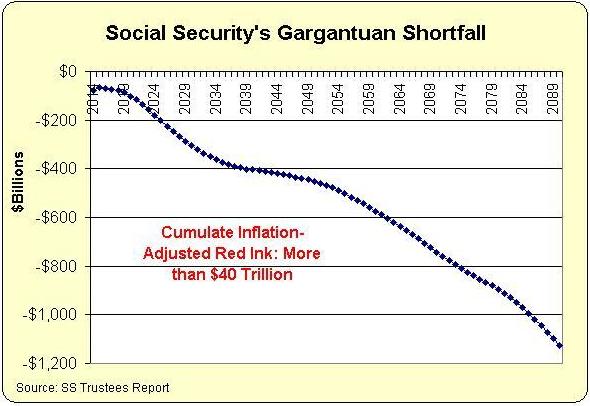

In reality, the level of projected red ink is shocking. If you look at the report’s annual projections and then adjust them for inflation (so we get an idea of the size of the problem based on the value of today’s dollars), we can put together a very depressing chart.

How depressing is this chart? Well, cumulative deficits over the next 75 years will total an astounding $40 trillion. And keep in mind these are inflation-adjusted numbers. In nominal dollars, total red ink will be far more than $150 trillion.

That’s a lot of money even by Washington standards.

Just as worrisome, the trend is in the wrong direction. Last year, the cumulative inflation-adjusted shortfall was $36 trillion. The year before, the total amount of red ink was $30 trillion. And so on.

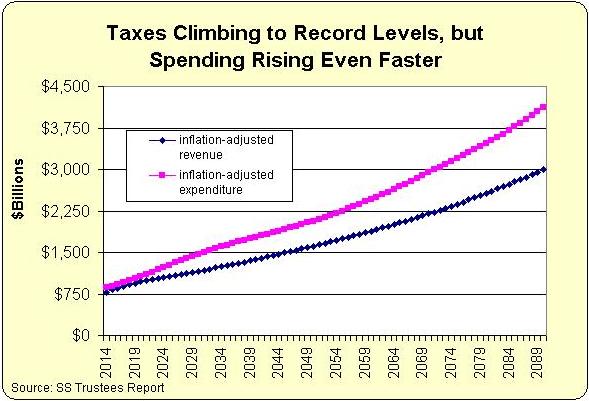

But regular readers know I’m not fixated on deficits and debt. I’m much more worried about the underlying problem of too much spending. So let’s look at the annual data showing how much payroll tax will be generated by Social Security and how much money will be paid out to beneficiaries.

As you can see, the problem is not inadequate tax revenue. Indeed, revenues will climb to record levels. The problem is that spending is projected to increase at an even faster rate.

Once again, don’t forget that these are inflation-adjusted numbers. In nominal dollars, the numbers are far bigger!

Why is the program becoming an ever-larger fiscal burden? The answer boils down to demographics. Simply stated, we will have more and more old people and fewer and fewer younger workers.

So if we do nothing, we’ll be Greece in 20 or 30 years.

That’s not a happy thought, so let’s close on a humorous note. Here’s a joke about how Social Security works, and you can enjoy some Social Security-themed cartoons here, here, and here.

P.S. I’m confident that few people will be surprised to learn that Obama’s supposed solution to this mess involves a huge tax increase.

P.P.S. The real solution is personal retirement accounts. I think Australia is the best role model, but Chile also is a big success.

P.P.S. The good news is that the American people are quite sympathetic to personal retirement accounts.

P.P.P.S. Statists try to scare people by claiming private investments are too risky, but one of my Cato colleagues showed that workers would be better off even if they retired after a stock market crash.

P.P.P.P.S. By the way, Social Security is a really bad deal for blacks and other minorities with lower-than-average life expectancies.

P.P.P.P.P.S. In the interests of fairness, I’ll admit the biggest weakness in the argument for personal accounts is that we might not be able to stop politicians from confiscating the money at some point in the future.

The SSTF is part of the $17 trillion national debt. They are held under Intra-governmental Holdings as distinguished from the publicly held portion of the debt. There is no "surplus,s" but rather interest-bearing , non-market T-bills that must be redeemed by the General Fund to make up the shortfalls. The current amount is about $2.8 trillion.

SS is a pay as you go system. Today's workers pay for today's retirees. SS has been running a shortfall since 2010, i.e., revenue received is less than benefits paid out. In order to make up the shortfall, SS cashes in some of the T-bills in the SSTF. The General Fund must come up with money. Since we borrow 40 cents of every dollar spent, we borrow money to redeem the SS T-bills,

Social Security has passed a tipping point. For years it generated more revenue than it consumed, holding down the overall federal deficit and allowing Congress to spend more freely for other things. But those days are gone. Rather than lessening the federal deficit, Social Security has at last — as long predicted — become a drag on the government’s overall finances.

And Medicare is in far worse shape. 40% of all Medicare funding comes from the General Fund. Currently, $233 billion came from the General Fund. Medicare has been running in the red since 2008.

![]()

This graph shows that the average man and woman (average defined in the study as average income over their working lives and living to the average life expectancy) who start receiving benefits in 2010 get over 3 times more in benefits than they pay in to the system! Of importance, the study accounts for inflation by calculating all past taxes and future payments in 2010 dollars to provide an accurate comparison.

If the notion that Medicare recipients are simply "getting back what they paid in" is false then where is the money coming from? Simply, the excess received is being borrowed from younger generations and the cost is more than we can bear.

If we cut out the half of Detroit that’s ‘disabled’ - also known as the ‘new welfare’ the system will do fine.

And if not, just give everyone their money back (with interest) that they put into SS and scrap it.

Yes, WITH interest.

I plan to retire in 2031 at 70.

I am not planning on social security at all.

It is supposed to be my money. But I already consider it just another tax, and I’ll never see it again.

Yes, we’ve been lied to.

I’ve finally succumbed to ObamaMalise: I’ll most likely be dead by the time the SHTF, so I really don’t give a damn anymore. Our country as we knew it when we were born is now on an unstoppable track for complete “Progressive” social fascism. And the sheeple? Well, they’re sheeple, and they’ll blissfully and ignorantly ride the fascist merry-go-round all fat dumb and happy until the unmitigated money manufacturing brings the ride to a screeching halt.

I'm well aware of everything you say. But, still, should our government ever become more fiscally responsible, SS is not our biggest problem. For a decade and longer the current year SS deficit will build from around $100 billion to $200 billion, not much in $4 trillion budgets. And the government still owes SS $4.7 trillion as part of the national debt. - Simply raising the SS retirement age is a start.

Nothing is funding the $1 trillion and growing annual payout in poverty programs other than current year, non-SS revenue and new government debt (40%+ of all spending).

SS is not the real problem, but irresponsible spending and borrowing. If that's not remedied, then every dollar in the federal budget is at risk along with the US economy and the living standards of most Americans.

There is no logic, only politics, in constantly singling out SS as the great, looming financial disaster. Decades of reckless spending and kicking the fiscal responsibility can down the road is the real problem.

Actually, your SS shortfalls are less than the ones in the original article posted here.

How about we end the entire damned thing. There’s ZERO constitutional authority for the Feds to run this scheme.

Only good thing about it is my wife didn’t want me hanging around the house anyway so she’s happy to have me working till I’m 70 - LOL

The number is $2.7 trillion, not $4.6 trillion. And it is only a surplus to SS, not for the USG. The $2.7 trillion is a debt owed to SS by the USG. The $2.7 trillion is part of our $17 trillion national debt.

I'm well aware of everything you say. But, still, should our government ever become more fiscally responsible, SS is not our biggest problem. For a decade and longer the current year SS deficit will build from around $100 billion to $200 billion, not much in $4 trillion budgets.

From the 2014 Trustee Report

To summarize overall Social Security finances, the Trustees have traditionally emphasized the financial status of the theoretical combined trust funds for DI and for Old Age and Survivors Insurance (OASI). The combined trust funds, and expenditures that can be financed in the context of the combined trust funds, are theoretical constructs because there is no legal authority to finance one program’s expenditures with the other program’s taxes or reserves. Social Security’s total expenditures have exceeded non-interest income of its combined trust funds since 2010 and the Trustees estimate that Social Security cost will exceed non-interest income throughout the 75-year projection period. The Trustees project that this annual cash-flow deficit will average about $77 billion between 2014 and 2018 before rising steeply as income growth slows to its sustainable trend rate after the economic recovery is complete while the number of beneficiaries continues to grow at a substantially faster rate than the number of covered workers.

Redemption of trust fund asset reserves from the General Fund of the Treasury will provide the resources needed to offset Social Security’s annual aggregate cash-flow deficits. Since the cash-flow deficit will be less than interest earnings through 2019, reserves of the combined trust funds will continue to grow but not by enough to prevent the ratio of reserves to one year’s projected cost (the combined trust fund ratio) from declining. (This ratio peaked in 2008, declined through 2013, and is expected to decline steadily in future years.) After 2019, Treasury will redeem trust fund asset reserves to the extent that program cost exceeds tax revenue and interest earnings until depletion of combined trust fund reserves in 2033, the same year projected in last year’s Trustees Report. Thereafter, tax income would be sufficient to pay about three-quarters of scheduled benefits through the end of the projection period in 2088.

Social Security’s Disability Insurance (DI) program satisfies neither the Trustees’ long-range test of close actuarial balance nor their short-range test of financial adequacy and faces the most immediate financing shortfall of any of the separate trust funds. DI Trust Fund reserves expressed as a percent of annual cost (the trust fund ratio) declined to 62 percent at the beginning of 2014, and the Trustees project trust fund depletion late in 2016, the same year projected in the last Trustees Report. DI costs have exceeded non-interest income since 2005 and the trust fund ratio has declined in every year since peaking in 2003. While legislation is needed to address all of Social Security’s financial imbalances, the need has become most urgent with respect to the program’s disability insurance component. Lawmakers need to act soon to avoid automatic reductions in payments to DI beneficiaries in late 2016.

Since the primary source of income for OASDI and HI is the payroll tax, it is informative to express the programs’ incomes and costs as percentages of taxable payroll—that is, of the base of worker earnings taxed to support each program (Chart B). Both the OASDI and HI annual cost rates rise over the long run from their 2013 levels (13.97 and 3.55 percent). Projected Social Security cost grows to 17.14 percent of taxable payroll by 2037, declines to 16.89 percent in 2050, and then rises gradually to 18.19 percent in 2088. The projected Medicare HI cost rate rises to 5.11 percent of taxable payroll in 2050, and thereafter increases to 5.56 percent in 2088. HI taxable payroll is almost 25 percent larger than that of OASDI because the HI payroll tax is imposed on all earnings while OASDI taxes apply only to earnings up to an annual maximum ($117,000 in 2014).

In 2014, the projected difference between Social Security’s expenditures and dedicated tax income is $80 billion. For HI, the projected difference between expenditures and dedicated tax and premium income is $25 billion. 3 The projected general revenue demands of SMI are $248 billion. Thus, the total General Fund requirements for Social Security and Medicare in 2014 are $352 billion, or 2.0 percent of GDP. Redemption of trust fund bonds, interest paid on those bonds, and transfers from the General Fund provide no new net income to the Treasury, which must finance these payments through some combination of increased taxation, reductions in other government spending, or additional borrowing from the public.

Nothing is funding the $1 trillion and growing annual payout in poverty programs other than current year, non-SS revenue and new government debt (40%+ of all spending).

We are borrowing money to pay SS and Medicare benefits. Yes, there are about $1 trillion in means-tested welfare payments, but you can't discount the impact of the entitlement programs, which are the biggest driver of our debt. 40% of all Medicare costs are paid from the General Fund. What many people may not realize is that by law, only 25% of Medicare Parts B and D (SMI) costs are paid by premium revenue. The other 75% comes from the GF and that will increase significantly as the baby boomers turn 65. If not reformed, Medicare alone could consume the entire federal budget

SS is not the real problem, but irresponsible spending and borrowing. If that's not remedied, then every dollar in the federal budget is at risk along with the US economy and the living standards of most Americans.

Medicare is a far worse problem than SS. Much of our spending and borrowing is related to the entitlement programs and debt servicing costs. If we have a change back to historic interest rate levels, we will have some very immediate problems, i.e., there will be a financial crisis.

There will have to be immediate action to address the SS DI Trust Fund, which runs out of IOUs in 2016 forcing a cut in benefits.

There is no logic, only politics, in constantly singling out SS as the great, looming financial disaster. Decades of reckless spending and kicking the fiscal responsibility can down the road is the real problem.

SS is part of the problem. In 1950 there were 16 workers to support every retiree; today it is about 3; and by 2030, there will be just two. You can only tax people so much to pay for retiree benefits.

Reforming the entitlement programs has been kicked down the road, because it is unpopular to talk about either reducing benefits or increasing taxes or some combination of both. Unless it is done, we will face some very painful decisions in the future, which is not far off.

It was a chart created by CBO in 2011. Projections can be off as we have learned many times. The Trustees Report is the best place to look.

This is what abortion will do to a nation’s economy.

.

I'm not discounting any budget item. They will all be in jeopardy some day if our government does not reign in spending and stop piling up more and more debt.

And, yes, it is an irritant to me to constantly see SS singled out as the looming financial time bomb. Few will mention poverty programs because there are so many politicians quick to demagogue any suggestion that those need to be cut, or eligibility made more strict.

And another major expense - Interest on the debt - is another one they talk little about. But with the continually growing debt, and if interest rates should return to more normal levels, interest on the debt could move to a trillion per year bidget expense within five to ten years. Of course, it's the mission of the Fed these days to prevent that from happening. But if our credit worthiness declines too much, who knows what might happen.

kabar, here is a related question. You are around DC and familiar with most government operatrions, so could you provide some clarification on this.

The government has been issuing debt instruments for years to finance government operations. In the past few years, the Fed has engaged in “quantitative easing” and is said to be buying up mortgages and other financial instruments held by financial institutions. And the Fed also buys normal government issued debt at times, as I understand it.

1. Is quantitative easing a Fed action where they purchase financial holdings only from financial institutions? Does QE have anything to do with financing the government’s operating deficits?

2. When the Fed buys government issued debt, I assume that reduces the amount that must be sold to individuals and foreign governments to finance our government’s operations?

It’s just not always clear what the Fed is doing and how it realtes to financing the budget deficits.

Thanks,

The so-called mandatory items are causing reductions in defense and the rest of government operations. We spend more on SS than we do defense. If interest rates rise, out debt servicing costs could also exceed these expenditures.

And, yes, it is an irritant to me to constantly see SS singled out as the looming financial time bomb. Few will mention poverty programs because there are so many politicians quick to demagogue any suggestion that those need to be cut, or eligibility made more strict.

The poverty programs will eventually have to be cut. SS will not be cut because of the political consequences. It is still in many ways the third rail of politics. There are 58 million SS recipients including 15 million under the age of 65. Our population of those over 65 will double in the next 20 years with 10,000 baby boomers turning 65 every day for the next 20 years. There will be 78 million over 65 in 2030, or one in five people.

Compared to Medicare, SS is the easier to solve, but it is the most sensitive. One third of the people receiving SS have it as their only income and for two thirds of the recipients, it makes up more than half of their income. Many Americans have not saved for their retirement. They face grim futures.

And another major expense - Interest on the debt - is another one they talk little about. But with the continually growing debt, and if interest rates should return to more normal levels, interest on the debt could move to a trillion per year bidget expense within five to ten years. Of course, it's the mission of the Fed these days to prevent that from happening. But if our credit worthiness declines too much, who knows what might happen.

If the bubble pops, the Fed won't be able to do anything. They are phasing out QE after buying over $4 trillion worth of T-bills. It will be interesting to see how they can div set themselves of all those T-bills. Hello Weimar Republic.

Here is an accurate, but funny explanation

2. When the Fed buys government issued debt, I assume that reduces the amount that must be sold to individuals and foreign governments to finance our government’s operations?

Correct.

And, where in the Constitution does it say that the federal government can take money from young people and give it to seniors?

And, where in the Constitution does it say that the federal government can take money from young people and give it to seniors?

That’s why everyone who is not stoned calls her Crazy Pelosi.

Current inflation rates are so falsely understated that soon a social security check will be like a penny is now, not worth the trouble of bending over to pick it up. People have long said that it is not possible to live on social security but in reality it WAS possible not so long ago. Anyone who had the foresight to make sure he was debt free on retirement and owned a home and a vehicle unencumbered could live with some dignity on nothing more than social security. A married couple who both were eligible for anywhere near the maximum and had no debts could do well enough but increasing food, energy and medical expenses are now so high that most people cannot earn enough money working to survive. Many of those who ARE working are earning less than some who are drawing social security. I don’t draw the maximum, nor does my wife but when I was a small boy whole families were living for a year on less than our combined monthly social security check, that is the truth of inflation in America.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.