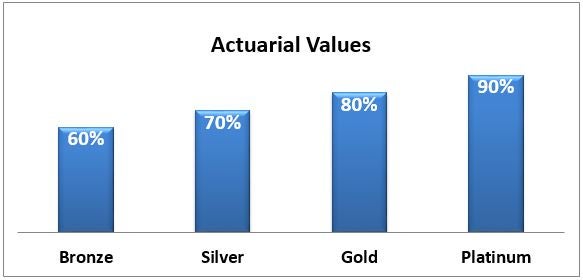

That is not a PP&ACA compliant plan. Coinsurance (patient responsibility) can not be greater than 40%.

Silver tends to vary by state.

Posted on 01/02/2014 3:06:08 PM PST by kristinn

Hospital staff in Northern Virginia are turning away sick people on a frigid Thursday morning because they can't determine whether their Obamacare insurance plans are in effect.

Patients in a close-in DC suburb who think they've signed up for new insurance plans are struggling to show their December enrollments are in force, and health care administrators aren't taking their word for it.

In place of quick service and painless billing, these Virginians are now facing the threat of sticker-shock that comes with bills they can't afford.

'They had no idea if my insurance was active or not!' a coughing Maria Galvez told MailOnline outside the Inova Healthplex facility in the town of Springfield.

She was leaving the building without getting a needed chest x-ray.

'The people in there told me that since I didn't have an insurance card, I would be billed for the whole cost of the x-ray,' Galvez said, her young daughter in tow. 'It's not fair – you know, I signed up last week like I was supposed to.'

The x-ray's cost, she was told, would likely be more than $500.

Galvez said she enrolled in a Carefirst Blue Cross bronze plan at a cost of about $450 per month through healthcare.gov, three days before Christmas.

'No one has sent me a bill,' she said.

Health and Human Services Secretary Kathleen Sebelius testified in a December 11 congressional hearing that the federal government can't say how many new enrollees have written checks for their first month's premiums.

'Some may have paid, some may have not,' she conceded.

It's unlikely that a valid insurance card would have changed Galvez' fortunes, however.

(Excerpt) Read more at dailymail.co.uk ...

I went to my retina specialist today for a follow-up visit. They told me they were requiring all bills to be paid in full, even if you had insurance, because they couldn’t figure out who had coverage or how the deductibles would work.

I’m fine because I have insurance and a health savings account which will pay my deductible — it is tied to my insurance so they would have gotten the payment, now the HSA will send me a check instead.

But I feel bad for the people going into the office today, facing a $500 charge, and having to leave without treatment.

I've been able to get bills settled at 70% or even 60% on the dollar once we offer to pay cash up front. If they can bill insurance for the majority of it, sometimes it will even be less than that.

A few of our MDs have even had the courage to sign their names to anti-ObamaCare letters in our local newspaper.

We make a special point to seek them out when I have a need they can fill. Almost always, they give us a better deal when we congratulate them on the letter.

I'd say it's only part of the story. It explains part of why all payers as a group pay more to cover. It does not explain why insurers pay not a bit less (some quantity discount is OK by me) but a whole lot less than someone who is not in an insurance group.

In Covered CA the x-ray is not subject to the deductible but has a $65.00 co-pay but the E-R visit is subject to the deductible with a $250 co-pay after the deductible. The $500 was probably ER and x-ray.

I have seen stories that people paying cash get big discounts.

If they go in and negotiate in advance, sure. If you go in and get care in a health emergency, after signing to cover costs, you may get a decent deal, but you might get grossly overcharged as long as you have some money. You’ve signed an agreement to pay... without the costs having been disclosed. It’s potentially a blank check.

I have a friend in the insurance business. He said that if you were some Arab wanting voluntary surgery, you could get one of your people to offer to pay, say, 125% of what Medicare pays, and you might strike a deal. But, if you just sign a responsibility form in an emergency, they’ve got you and your assets by the short hairs.

I honestly don’t think I’m going to see much difference. Same doctors, clinic, hospital, pharmacy and even insurance company...

May be a few nuisance questions to deal with...Already refused (last month) one of the Obamacare-inspired health questionnaires - said I was not going to answer any questions read from a script but would answer most of the same questions if personally formulated by the provider. They dropped the whole issue and confined questions to the disorder I was presenting for.

That’s good. The questionnaires do sound like a pain. As I said...good luck and please do keep us posted.

That is not a PP&ACA compliant plan. Coinsurance (patient responsibility) can not be greater than 40%.

Silver tends to vary by state.

How long until someone dies from this and the effing MSM refuses to cover it?

I already heard one Dim Congresscritter offer the explanation that, "Republican have always liked these high deductible plans, so what are they complaining about?

Well. You’ve asked and I must be honest. We had a policy they offered kind of “no questions asked..” Just didn’t feel like being denied etc.. (heard the stories form others we had in the group) So, we went with it figuring a year later we’d shop. It cost a boat load.. Or two boat loads.. Just under $1800 a month. So to the point. We saved a few hundered a month.. The reason I’m soo wordy here is I could have done the savings on my own shopping after the years end. Then came the new policy.. Bc/Bs has been good to us. They will continue if allowed I’m sure.

That has been my experience with CareFirst too. Always pay the negotiated rate for deductibles. CareFirst actually told me to NOT pay any deductibles until they determined which one (payee) gets what amount of the deductible.

Of course, under any health insurance product, she was going to pay a lot more than the cost of the x-ray, either through high premiums, or high deductibles.

People don’t realize health insurance is just spreading out the cost of catastrophic care. Which means if you have treatment that everybody would get, it is built into the cost of the insurance.

So when the democrats kept throwing things in as “free preventative treatments”, what they were really doing is trying to force everybody to get those treatments, since the insurance company was going to price that into every policy.

So if you buy insurance, you are going to pay the total cost of every “preventative” treatment you can get in a year, PLUS your part of the risk cost for catastrophic care.

And because preventative care is always “free” under every plan, even the cheap high-deductible insurance is really costly.

If you really wanted cheap insurance, you’d buy JUST the catastrophic coverage, put aside $10,000 to cover regular office visits and small issues, and do everything in your power to stay healthy and take care of your own minor illnesses (or find cheap practitioner-type service as a screening tool).

But you can’t do this anymore. Because Obama doesn’t think that is smart. Even though it is the smartest way to handle the health care industry — it would lead to better competition and more self-control in use of the services.

Oh, I know , you know , I agree.! The poster just sounded like our situation.. Clearly an FYI. It’s rare I’d say anything ( because in a thread, my point/thought is made) GOD Save the Freep!

yeah, its based on the date they get the claim, not date of service. if you pre-pay the OB gyn first, but the hospital gets the claim in first, we pay the dr and you owe the hospital, so it’s the patient responsibility to get a refund from the dr and pay the hospital.

You are correct. The terms for the two largest drivers of medical inflation are called "charity care" and "cost shifting".

Obamacare fail.

And also all the LIV "conservatives" who stayed home in 2012 and helped Obama foist this T.U.R.D. over on us.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.