Blaming W for the sub prime mess shows a ridiculous lack of judgment. Not to mention, right wingers who collaborate with the Kenyan lizard king’s blame Bush meme make me sick.

Absolving Bush for his involvement in the sub-prime mess shows willful ignorance.

Had you bothered to do even a modicum of research, you'd know that Bush's housing initiatives were anything but puny. In fact, it was Bush, himself, who in 2002 called for Fannie and Freddie to increase their commitments to the housing market and it was he, who praised Franklin Raines for the job he did running Fannie.

|

Park Place South is, in microcosm, the story of a well-intentioned policy gone awry. Advocating homeownership is hardly novel; the Clinton administration did it, too. For Mr. Bush, it was part of his vision of an “ownership society,” in which Americans would rely less on the government for health care, retirement and shelter. It was also good politics, a way to court black and Hispanic voters. But for much of Mr. Bush’s tenure, government statistics show, incomes for most families remained relatively stagnant while housing prices skyrocketed. That put homeownership increasingly out of reach for first-time buyers like Mr. West. So Mr. Bush had to, in his words, “use the mighty muscle of the federal government” to meet his goal. He proposed affordable housing tax incentives. He insisted that Fannie Mae and Freddie Mac meet ambitious new goals for low-income lending. Concerned that down payments were a barrier, Mr. Bush persuaded Congress to spend up to $200 million a year to help first-time buyers with down payments and closing costs. And he pushed to allow first-time buyers to qualify for federally insured mortgages with no money down. Republican Congressional leaders and some housing advocates balked, arguing that homeowners with no stake in their investments would be more prone to walk away, as Mr. West did. Many economic experts, including some in the White House, now share that view. The president also leaned on mortgage brokers and lenders to devise their own innovations. “Corporate America,” he said, “has a responsibility to work to make America a compassionate place.” And corporate America, eyeing a lucrative market, delivered in ways Mr. Bush might not have expected, with a proliferation of too-good-to-be-true teaser rates and interest-only loans that were sold to investors in a loosely regulated environment. “This administration made decisions that allowed the free market to operate as a barroom brawl instead of a prize fight,” said L. William Seidman, who advised Republican presidents and led the savings and loan bailout in the 1990s. “To make the market work well, you have to have a lot of rules.” But Mr. Bush populated the financial system’s alphabet soup of oversight agencies with people who, like him, wanted fewer rules, not more. The president’s first chairman of the Securities and Exchange Commission promised a “kinder, gentler” agency. The second was pushed out amid industry complaints that he was too aggressive. Under its current leader, the agency failed to police the catastrophic decisions that toppled the investment bank Bear Stearns and contributed to the current crisis, according to a recent inspector general’s report. As for Mr. Bush’s banking regulators, they once brandished a chain saw over a 9,000-page pile of regulations as they promised to ease burdens on the industry. When states tried to use consumer protection laws to crack down on predatory lending, the comptroller of the currency blocked the effort, asserting that states had no authority over national banks. The administration won that fight at the Supreme Court. But Roy Cooper, North Carolina’s attorney general, said, “They took 50 sheriffs off the beat at a time when lending was becoming the Wild West.” The president did push rules aimed at forcing lenders to more clearly explain loan terms. But the White House shelved them in 2004, after industry-friendly members of Congress threatened to block confirmation of his new housing secretary. "In the 2004 election cycle, mortgage bankers and brokers poured nearly $847,000 into Mr. Bush’s re-election campaign, more than triple their contributions in 2000, according to the nonpartisan Center for Responsive Politics. The administration did not finalize the new rules until last month." Among the Republican Party’s top 10 donors in 2004 was Roland Arnall. He founded Ameriquest, then the nation’s largest lender in the subprime market, which focuses on less creditworthy borrowers. In July 2005, the company agreed to set aside $325 million to settle allegations in 30 states that it had preyed on borrowers with hidden fees and ballooning payments. It was an early signal that deceptive lending practices, which would later set off a wave of foreclosures, were widespread.

Andrew H. Card Jr., Mr. Bush’s former chief of staff, said White House aides discussed Ameriquest’s troubles, though not what they might portend for the economy. Mr. Bush had just nominated Mr. Arnall as his ambassador to the Netherlands, and the White House was primarily concerned with making sure he would be confirmed. “Maybe I was asleep at the switch,” Mr. Card said in an interview. Brian Montgomery, the Federal Housing Administration commissioner, understood the significance. His agency insures home loans, traditionally for the same low-income minority borrowers Mr. Bush wanted to help. When he arrived in June 2005, he was shocked to find those customers had been lured away by the “fool’s gold” of subprime loans. The Ameriquest settlement, he said, reinforced his concern that the industry was exploiting borrowers. In December 2005, Mr. Montgomery drafted a memo and brought it to the White House. “I don’t think this is what the president had in mind here,” he recalled telling Ryan Streeter, then the president’s chief housing policy analyst. It was an opportunity to address the risky subprime lending practices head on. But that was never seriously discussed. More senior aides, like Karl Rove, Mr. Bush’s chief political strategist, were wary of overly regulating an industry that, Mr. Rove said in an interview, provided “a valuable service to people who could not otherwise get credit.” While he had some concerns about the industry’s practices, he said, “it did provide an opportunity for people, a lot of whom are still in their houses today.” The White House pursued a narrower plan offered by Mr. Montgomery that would have allowed the F.H.A. to loosen standards so it could lure back subprime borrowers by insuring similar, but safer, loans. It passed the House but died in the Senate, where Republican senators feared that the agency would merely be mimicking the private sector’s risky practices — a view Mr. Rove said he shared. ‘We Told You So’ Armando Falcon Jr. was preparing to take on a couple of giants. A soft-spoken Texan, Mr. Falcon ran the Office of Federal Housing Enterprise Oversight, a tiny government agency that oversaw Fannie Mae and Freddie Mac, two pillars of the American housing industry. In February 2003, he was finishing a blockbuster report that warned the pillars could crumble. Created by Congress, Fannie and Freddie — called G.S.E.’s, for government-sponsored entities — bought trillions of dollars’ worth of mortgages to hold or sell to investors as guaranteed securities. The companies were also Washington powerhouses, stuffing lawmakers’ campaign coffers and hiring bare-knuckled lobbyists. Mr. Falcon’s report outlined a worst-case situation in which Fannie and Freddie could default on debt, setting off “contagious illiquidity in the market” — in other words, a financial meltdown. He also raised red flags about the companies’ soaring use of derivatives, the complex financial instruments that economic experts now blame for spreading the housing collapse. Today, the White House cites that report — and its subsequent effort to better regulate Fannie and Freddie — as evidence that it foresaw the crisis and tried to avert it. Bush officials recently wrote up a talking points memo headlined “G.S.E.’s — We Told You So.” But the back story is more complicated. To begin with, on the day Mr. Falcon issued his report, the White House tried to fire him. (See: White House Philosophy Stoked Mortgage Bonfire) |

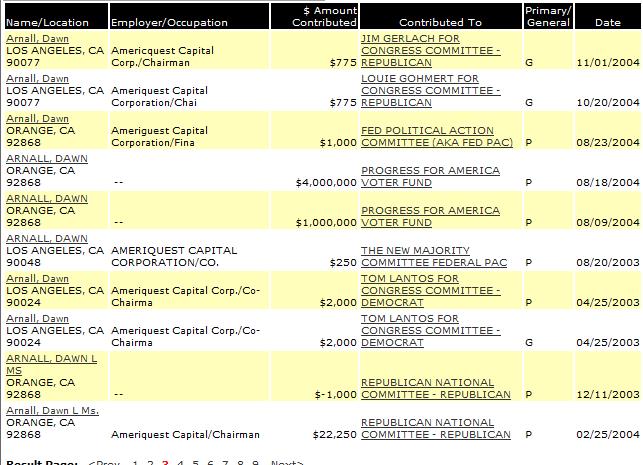

Who is the Progress for America Fund that received $5 million in campaign contributions from the sub-prime lender, Arnall?

From: Progress for America Voter Fund:

Progress for America (PFA) (a 501c4) and its affiliate Progress for America Voter Fund (PFA-VF) (a 527 committee) are national tax-exempt organizations. The PFA was, from the beginning, "closely associated" with the Bush administration, the Republican National Committee and "their consultants." [1]

PFA was established in 2001 to support George W. Bush's "agenda for America." The PFA Voter Fund, which was set up in 2004, raised $38 million in support of Bush's 2004 election bid.

Progress for America, a "friends of the party" organization "operated by Tony Feather, the former political director of Bush-Cheney 2000 and a close friend of White House political adviser Karl Rove, is described by some Republicans as a new group dedicated to corralling outlawed party soft money," Steve Weismann, Associate Director for Policy at The Campaign Finance Institute wrote January 28, 2003.

In addition, Bush received the following campaign contributions for the 2004 election cycle:

Goldman-Sachs: $4,000,000

Merryl-Lynch: $1,500,000

Morgan-Stanley: $1,500,000

UBS-AG: $1,400,000

Lehman Bros.: $1,000,000

Grand Total: $12,900,000

But, you assert that, despite receiving almost $18 million in contributions for the 2004 election, Bush was not in the pockets of the Wall Street bankers who were at the center of the sub-prime mess.