Posted on 11/02/2025 6:19:47 AM PST by marktwain

In the recent discourse around the potential removal of suppressors and short barrel rifles from the provisions of the National Firearms Act (NFA) and its tax and registration requirements, a point made repeatedly was that if the tax was repealed but the registration stayed, the latter would be illegal as it was only ever justified by the former.

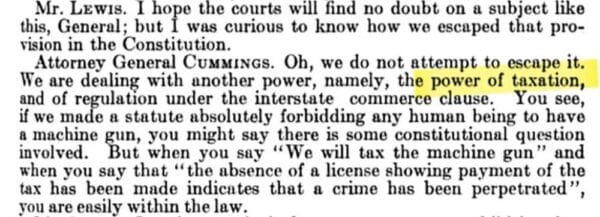

This is indeed correct, as from its inception, the NFA was justified as a tax, with the registration being incidental to that tax and only existing ostensibly to ensure the tax was properly paid for each NFA item sold. Then-Attorney General Cummings was clear about this in his testimony to Congress during the debates over the bill in 1934:<

Courts have consistently upheld the NFA, and its registration provision, on the grounds that it was a tax. Some who tried to challenge the law even argued that the tax was a pretext, with the real aim being to unconstitutionally restrict the arms included in the NFA. The Supreme Court rejected this argument in 1937, just a few years after the NFA was first enacted in Sonzinsky v. United States, 300 U.S. 506, 512-514 (1937):

“Petitioner. . .insists that the present levy is not a true tax, but a penalty imposed for the purpose of suppressing traffic in a certain noxious type of firearms, the local regulation of which is reserved to the states because not granted to the national government. . . But a tax is not any the less a tax because it has a regulatory effect. . . Here the annual tax of $200 is productive of some revenue.

(Excerpt) Read more at ammoland.com ...

|

Click here: to donate by Credit Card Or here: to donate by PayPal Or by mail to: Free Republic, LLC - PO Box 9771 - Fresno, CA 93794 Thank you very much and God bless you. |

Of home-made.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.