Posted on 02/24/2015 4:49:11 PM PST by CutePuppy

During the crisis most of the losers and winners were easily identifiable (Bear Stearns, Washington Mutual vs JP Morgan; Countrywide Financial, Merrill Lynch vs Bank of America; Wachovia vs Wells Fargo etc.). Of course, government having another chunk of "extra" money to loan, could and — in the worst traditions of crony socialism — did disperse some of that money to their friends (which was well documented here on FR at the time), but using the natural government corruption to deny the need for TARP-like injection if liquidity to financial system so the consumers' and business deposit accounts can be backed and then trickled down to businesses and customers is ridiculous. The lenders of last resort did exactly what the lenders of the last resort were supposed to do, faced with the credit and liquidity crisis. 1. Do downward credit spirals really happen?

You betcha. Persistent depression / compression and deflation are two of the examples that basically self-perpetuate themself, aka the vicious cycle. 2. If yes, are the caused or cured by government?

Could be either. It depends on the government. For example, take Greece... (please!) People there just elected the government that told them what they wanted to hear (stop "austerity," restart higher government spending paid for by higher taxes on the rich and clamp-down on tax evasion / "cheaters," even though it's exacty what caused the current problems and is the wrong prescription for Greek economy. Germany, on the other hand, weathered the storm relatively unscathed and is the main engine of the EMU and EU economy.

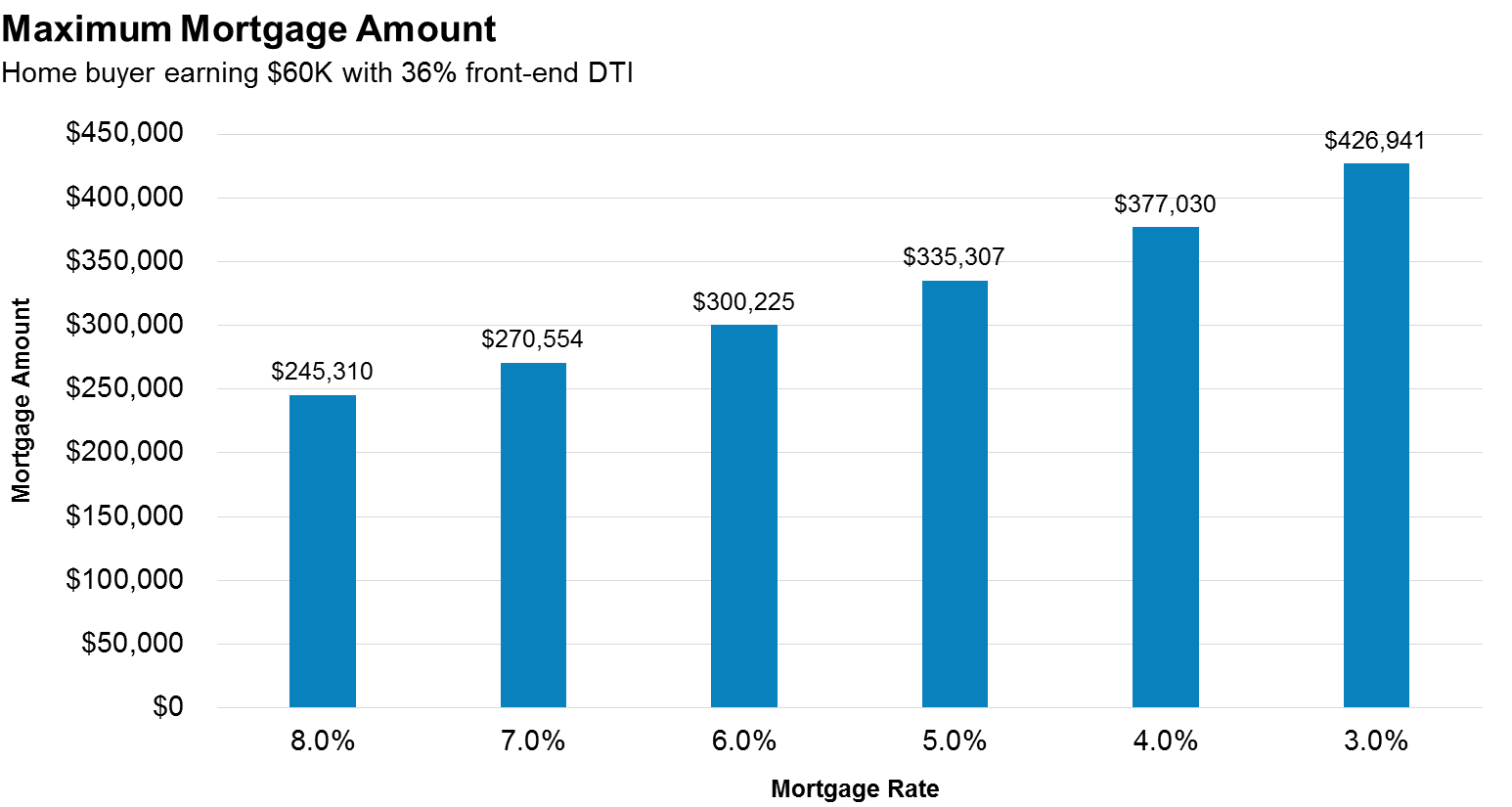

What’s a 36% DTI?

Good piece. Thanks for posting.

I mentioned (in the weekly market thread that expat_panama runs) last September that I attended the Zelman and Associates Housing Summit in Washington DC (6th year of going). It is the best gathering of builders, suppliers, bankers, regulators, etc. in the US housing market. The number 1 topic from all of the presenters was the lending environment. Everyone was talking about the lenders not reducing the overlays (the restrictions above what the regulators require) that banks were placing on borrowers of all kinds due to the uncertainty of the legal and regulatory environment. They got burned in the financial crisis because the government forced them to lend to people who couldn’t afford it in the name of “housing access” and then were sued for billions by the very same people who forced them to lend. They aren’t about to go through that again.

Debt to Income. It’s a ratio that used to be as high as 40% and is built on gross income.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.