100%

100%

Posted on 03/09/2014 8:14:23 AM PDT by shove_it

To Continue Gains, Stocks Are Liable to Rely More on the Economy Than Fed Support and Need Higher Corporate Profits

As the bull market turns five years old, stock investors have a lot to celebrate.

The Dow Jones Industrial Average has soared 151% since stocks bottomed March 9, 2009, following the financial crisis. That ranks it fifth in gains among the 32 bull markets since 1900.

It also is tied for fifth-longest-running, in trading days, with the one that ended in 2007, according to Ned Davis Research.

If the current stock advance lasts another 16 trading days, it will be the fourth-longest, surpassing the one that ended in 1987...

(Excerpt) Read more at online.wsj.com ...

WSJ is for whomever and whatever perpetuates the financial markets gaining wealth, legal or illegal.

100%

My IRA grew by 11 grand in the month of February. I’m thinking of switching it to all cash, any suggestions from savvy investors?

They don’t want to bite the hand that feeds them.

I just hope it stays up until my Mom’s estate is done. She unfortunately died in November and the estate should be done by Summer which means turning in the Mutuals, 401K, stocks, etc and splitting 3 ways with my Brother and Sister. I don’t think it is bad thinking you want to cash out at the highest possible amount.

yeah, simple another whore

Indeed no shortage of them.

I have been taking some profits over the past year.

In accordance with the strategy known as “asset allocation,” you might want to keep some money in equities, and the rest in bonds, cash, or equivalents. The general rule of thumb is that your age minus 10 is the percentage to keep in cash and bonds.

In other words, if you’re 40, then keep 30% in bonds, the rest in equities. If you’re 70, then the percentage is 60% cash and bonds.

The theory is that the older you are, the less time you have to recover from a market setback, while if you are younger, then you need the compounding power of equities to build wealth.

Of course, your mileage may vary, depending upon your risk tolerance and total portfolio value.

In my case, I’m 64 years old and have been a long-term buy-and-hold investor for nearly 40 years. I’ve been through Nixon, Ford, Carter, Reagan, Clinton, two Bushes, and Obama. During that time, equities have roughly quadrupled the amount of money that I originally invested.

That includes the Dot Com bubble burst and the 08-09 meltdown. I didn’t bail out in either case, and actually added to my equity positions.

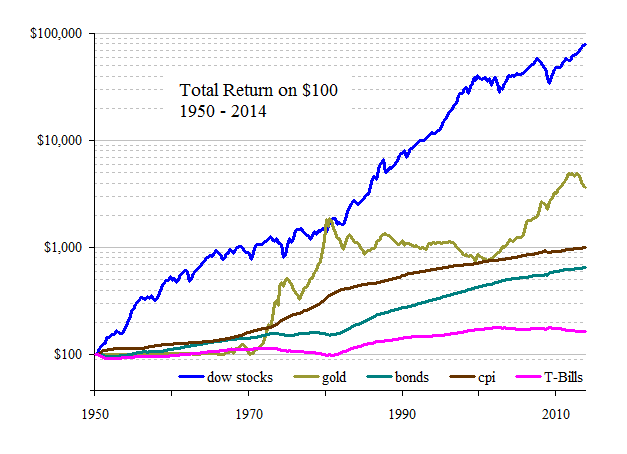

If you study the entire history of the markets for the past century and a half, it is evident that equities have been the best vehicle for creating wealth, compared to any other - bonds, commodities (including gold), land, etc.

There is no substitute for long-term disciplined investing. Obama one day will gone, and a business-friendly administration will be in office.

Never underestimate the wealth creating ability of the American Businessman and the creativity of Free Enterprise.

Good post - thanks.

It’s turning into a bubble caused by cheap money printed by the Federal Reserve. With inflation-adjusted interest rates negative on bank deposits, the average Joe is compelled to save for his new car, water heater replacement, etc., by purchasing stocks.

Amen!!!

U.S. business, especially the large corporations, will always find a way to make money no matter which party is in office. People are only hurting themselves by not investing in something. There are many ways to wealth - your own business, rental properties, the stock market, etc. But the key is to invest in something! I was raised by very conservative parents, and I have learned by example to live within my means and to invest for my future.

I strongly recommend The Bogleheads to folks wanting to know more about slow and steady investing for the future. Their website is an invaluable resource of information about asset allocation, selecting low cost index funds, etc. The Bogleheads has both an informative Forum and informative Wiki. Check them out!

Rule Number 1: Spend less than you make, and save/invest the balance.

Rule Number 2: See rule 1.

Unless and until you observe, without fail, the two rules listed above, no investment/wealth creating strategy of any kind will work.

Market timing is a lot of work. What I did for my IRA funds long before retiring was to just dump it all into a stock fund and fuhgeddaboutit. Long term profits average 7% yearly--

--but any individual year can vary so most people only go to cash when they want to be able to know what next month's balance will be.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.