Posted on 09/18/2013 5:30:22 AM PDT by Kaslin

Move over Detroit. The fiscal crisis in Chicago is far bigger.

Via email, Ted Dabrowski at the Illinois Policy Center writes ...

While all eyes are focused on a solution for Illinois’ state-run pension systems, Chicago’s own debt crisis is looming.

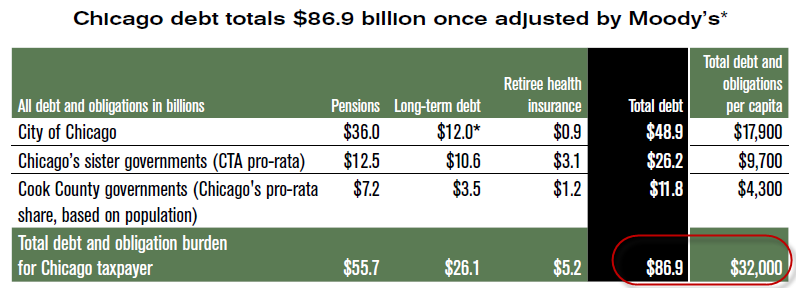

Chicago taxpayers are on the hook for more than $63 billion in pension, health insurance and other debt. That’s the total debt of the city and its sister governments, as well as Chicagoans' share of Cook County debt.

In total, each Chicago household is on the hook for more than $61,000.

Chicago’s pension crisis isn’t new, but Detroit’s bankruptcy has brought national attention to Chicago’s growing crisis. Just a day after Detroit filed for bankruptcy, Moody’s Investors Service downgraded Chicago’s debt by a rare three notches. Chicago is now just four notches away from junk-bond status — and any further downgrades mean the city could face problems borrowing money.

Without pension reform, Chicago Mayor Rahm Emanuel will be forced to raise taxes or dramatically cut government services.

Emanuel knows he can’t raise taxes. Chicago has lost more than 200,000 residents in the last decade and the city’s population is lower now than it was in the 1920s.

To make matters worse, Chicago’s services are already faltering. Chicago Public Schools closed nearly 50 schools this year, forcing children and families to travel across gang lines. Nearly 3,000 school employees have been laid off. And the city’s crime rate is among the worst in the nation.

Higher taxes, taxpayer flight and an inability to provide core services contributed to Detroit's demise — and it’s a trend that Chicago must reverse.

Fixing Chicago's pension crisis will require help from Springfield. Lawmakers need to follow the lead of the private sector and move all workers to 401(k)-style plans for all work going forward — an idea that Emanuel supports as an option for the city's new hires.

Ted Dabrowski

Vice President of Policy

The Hidden Bill

You can view the entire report at The hidden bill: Chicago taxpayers and the looming crisis.

A closer look at the "Hidden Bill" shows the problem is even worse than stated by Dabrowski above.

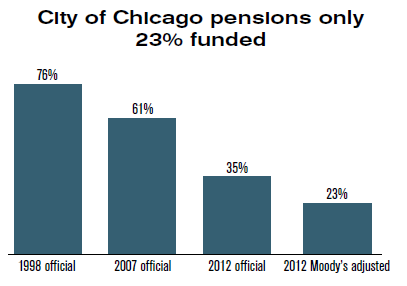

Pension funds have long assumed unrealistically high investment returns, which make the funds look healthier than they actually are. Moody’s Investors Service now calculates unfunded pension liabilities using more appropriate discount rates.

Under new Moody’s methodology, Chicago’s unfunded pension liabilities are at least $23 billion higher than what’s officially reported. Today, the systems have only 31 cents for every dollar

they should have to make necessary pension payouts in the future.

When summing up Chicago’s total debt, it’s necessary to use the Moody’s calculation of unfunded pension liabilities instead of those officially reported by the city. That’s because the municipal bond market depends heavily on Moody’s ratings when investing in Chicago bonds.

Moody’s based its recent triple-notch downgrade of the city’s debt on the agency’s new methodology for valuing pension shortfalls. The downgrade has led to a collapse in Chicago’s bond prices and a significant increase in its borrowing rates.

Chicago’s credit rating is now only four notches away from junk-bond status. Many institutional investors are not allowed to invest in junk bonds, meaning the city will face significant

pressure in accessing the bond market going forward if this downward trend continues.

Ignoring the Moody’s pension calculation not only understates the severity of Chicago’s debt crisis, but also the true burden that Chicago taxpayers may be forced to shoulder.

If you adjust pension obligations for a more realistic rate of return, the problem looks like this.

Chicago Obligations

Chicago Pension Funding

Four Long Term Solutions

The above long-term solutions will stop the problem from growing as well as ensure labor costs are market-priced, not union-priced.

I wish that was enough but it isn't. Those things will slow the rate of growth of the problem, but cannot address 77% pension underfunding.

Two Short Term Solution

Pension and benefit cuts are necessary, but how best to do it?

I propose the burden of pension cuts spread out in an equitable manner with those receiving the highest benefits taking the biggest percentage cuts.

All pension income above a certain cap could be taxed at a very high rate. This would protect the smaller pensioners from massive haircuts.

The alternative, as we saw in Central Falls, Rhode Island Bankruptcy, was an across the board 50% pension haircut.

Someone with a $200,000 pension had it cut to $100,000. Someone with a $25,000 pension had it cut to $12,500.

My proposal would cap the top-end rather than applying uniform haircuts. If one picks the cap carefully, a majority of union members would fare better under my plan than bankruptcy.

The Union Choice

Public unions can scream all they want, but the entire defined benefit pension system is insolvent.

There is no choice other than pension haircuts. There is a choice as to how:

Bankruptcy Here We Come

Unfortunately, unions are highly unlikely to accept my common sense proposal.

Ultimately, Chicago will play around with superficial remedies just like Central Falls, Detroit, and several cities in California (all of which succumbed to the inevitable).

In the meantime, Chicago will probably follow some other major cities into bankruptcy, such as Oakland and Los Angeles.

Investors better pick their municipal bonds carefully, because some major hits are on the way.

It does sound like a reason... and yeah, the end could be closer than we think... Thanks for sharing.

>>When she retired her pension checks were SIGNIFICANTLY larger then her pay had been when working.<<

Taking inflation into consideration, that is the way retirement should be planned for.

Nonsense. No private firm would pay a pension greater then the salary the person was earning while actually working. I’m not saying the payments increased with inflation, I’m saying the week after she retired she noticed a significant increase. That’s just crazy.

I retired 18 years ago. My income now, from my pension plan and the private retirement investments I made before I retired are paying me twice what I normally received as a paycheck during the last five years I was working. I planned it that way. It wasn’t an approved plan, it was self designed for the future that I saw beyond the horizon thirty years ago.

Am I lucky? Darn right I am because I saw beyond the then failing SSI checks that most people attempt to survive on. I scrimped and saved while I was working so that I hopefully wouldn’t have to during my retirement years and it worked.

Here’s the blunt truth. Out of the top twenty cities in America....all are in some sort of financial ailment. I would probably say that fifteen are ten years away from being a Detroit, and the remaining five are probably twenty years away.

Personally, I don’t see how you avoid this unless you stop the pension and healthcare cost spiral by city management folks.

I would also recommend that all folks sit down and read the Detroit Free Press examination of how Detroit came to this end-point...posted about a week ago on their site. There were signs in the 1980s...when property values started to slide and folks were leaving town (for the burb’s). If they had reacted then....they would have pushed the bankruptcy back another decade or two. If you see that your town’s population has peaked, property values are slipping for a 2nd consecutive year....you need to trim city cost and prepare for a dry-spell.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.