Posted on 09/20/2007 4:55:46 PM PDT by NYer

It’s a conspiracy among the Knights of Malta, the Knights Templars, and the Illuminati. They played the world conspiracy softball championship in Davos.

I know bankers of every religion. Nope, not seeing the connection.

Just keep them out of the temple, I guess.

They also kicked butt in the sack race!

Well, that was the only connection I could make at the moment. Otherwise, I have no idea why the Catholic ping.

Herbert Hoover took a needed market correction "seriously." The result of his seriousness, incidentally, WAS the crisis of 1929.

Must have something to do with Michael Corleone, the Vatican Bank and Immobiliare. Stay away from any operas.

Wow, just read the Columbia thread! The temps must have really dropped in Hell. Hope the virgins are bundled up! :-)

?

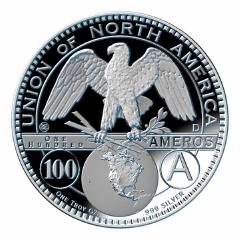

From Malkins site, last November

In an interview with CNBC, a vice president for a prominent London investment firm yesterday urged a move away from the dollar to the “amero,” a coming North American currency, he said, that “will have a big impact on everybody’s life, in Canada, the U.S. and Mexico.”

Steve Previs, a vice president at Jefferies International Ltd., explained the Amero “is the proposed new currency for the North American Community which is being developed right now between Canada, the U.S. and Mexico.”

The aim, he said, according to a transcript provided by CNBC to WND, is to make a “borderless community, much like the European Union, with the U.S. dollar, the Canadian dollar and the Mexican peso being replaced by the amero.”

Previs told the television audience many Canadians are “upset” about the amero. Most Americans outside of Texas largely are unaware of the amero or the plans to integrate North America, Previs observed, claiming many are just “putting their head in the sand” over the plans.

” Apparently, no one, neither the general public nor professionals on Wall Street, has yet to realise the extent of the hole, a hole of 20 trillion dollars with no market, nor value.”

a lot of folks on the street are very worried about this. The CMO trader I work with is convinced more bad news is down the line, but psychologically the market put in a short-term bottom a few weeks ago and I guess it takes either time or something particularly nasty to take it back down again.

True Believer Rule #33 - Never let facts get in the way of the your message.

William J. Clinton, the forty-second President of the United States (1993-2001)

Ah Haa! I have no idea of the distinction between the two.

Liquidity means not having sufficient cash. Solvency (or lack thereof) means not having sufficient cash to pay your bills. Correct?

Huh? This is BS worthy of the Weekly World News. I had no trouble rolling an $80 million 90-day LIBOR loan last week, and nothing has changed since then.

Condi wanted The Pope to bail out the hedge funds....

j/k

The difference is really between illiquidity and insolvency. It is quite possible to be solvent (i.e. all your assets minus all your liabilities equals a positive number) while being illiquid (i.e. no cash on hand to pay bills coming due right now. It’s a whole lot worse to be insolvent than to be illiquid. If you’re just illiquid but still solvent, it’s just a matter of time until you’re lquid again, and creditors will keep that in mind when negotiating with you about your currently overdue bills. If you’re insolvent, you’ll be pushed directly into bankruptcy court, so your creditors can start the process of claiming whatever reduced percentage of what they’re owed, is salvageable given your insolvent condition.

If you own a house free and clear that will easily sell for $100,000 even in this market, but only have $50 cash in the bank, and have an electric bill for $300 that’s due tomorrow, you have a liquidity problem, but you’re not insolvent. It’s reasonable to expect that the electric bill will get paid fairly soon (probably when you take out a home equity loan). But if you owe $150,000 on a house that will sell for $100,000 in this market, and $125,000 even when the housing market is back to normal, and you have that electric bill for $300 due tomorrow, you’re not just illiquid but also insolvent.

Insolvent banks are a big problem; illiquid banks are really just a little problem, that can be easily solved by emergency loans from a central bank, without any negative impact on the economy, inflation, etc.

I read an article about this early this a.m.

Not good news on the horizon at all.

Yes, it’s striking me as weird, and a bit worrisome, that everyone who has a clue is absolutely certain that a huge drop is on the way very soon. And yet it just keeps not happening. Mortgage derivative hedge funds go belly-up, CP markets freeze up, one money market fund failed to honor redemptions, a British retail bank has customers lined up at dawn to make panic withdrawals despite British Central Bank assurances that this isn’t necessary, and yet the stock market keeps toddling along as usual. This has gone on long enough that I’m starting to get seriously perplexed. I bailed out a while back, with the S&P just a hair over 1500, and I’m just sitting back waiting for the show to start. But it’s taking an inexplicably long time to start.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.