Skip to comments.

An Economic Pillar on the Verge of Collapse

Washington Post ^

| December 6, 2006

| Steven Pearlstein

Posted on 12/07/2006 8:52:46 AM PST by GodGunsGuts

An Economic Pillar on the Verge of Collapse

By Steven Pearlstein Wednesday, December 6, 2006; D01

It's been more than a year since we've heard from those who denied there was a housing bubble.

Since then, the industry boosters, along with the "soft-landing" crowd over at the Federal Reserve, have coalesced around the idea that maybe the market got a bit frothy after all, but now the correction is almost complete, the unsold inventory's been worked off and the worst is behind us.

But just when you're feeling hopeful again, you get reports like yesterday's Wall Street Journal piece reporting that delinquency rates are suddenly soaring on all those loosey-goosey subprime mortgages. They are starting to cause real heartburn for pension funds and other investors who bought securities backed by those mortgages on the theory that they were no more risky than a Treasury bond.

"We are a bit surprised by how fast this has unraveled," Thomas Zimmerman, head of asset-backed securities research at UBS, told the Journal, removing his head from the sand. Trust me, Tom, you ain't seen nothin' yet. After the subprime loans come the 100 percent, interest-only loans, followed by the meltdown in the overbuilt multi-family housing sector....

(Excerpt) Read more at washingtonpost.com ...

TOPICS: Business/Economy; Culture/Society; Government; News/Current Events

KEYWORDS: alasandalack; bubble; depression; despair; doom; dustbowl; eeyore; endoftheworld; goldbuggery; grapesofwrath; home; homeimprovement; housing; hysteria; improvement; joebtfsplk; theskyisfalling; woeisme

Navigation: use the links below to view more comments.

first previous 1-20, 21-40, 41-60, 61-80 ... 181 next last

To: RobRoy

And to suggest that people with "agendas" don't have valid opinions is like saying a jew in late 1930's germany should be ignored when he comments on the nazis because he has an agenda.LOL Good grief.

It's not like that at all.

41

posted on

12/07/2006 9:58:33 AM PST

by

Petronski

(I just love that woman.)

To: RobRoy

This is one reason I don't give people individual sources. Your anecdotes are much stronger if you don't bother to source them.

42

posted on

12/07/2006 9:58:52 AM PST

by

Toddsterpatriot

(If you agree with EPI, you're not a conservative!)

To: o_zarkman44

In southern OR, the builders have been idling for more than the winter months.

To: Paleo Conservative

It will be, but now is not the time. The slide should continue to for several years and then bottom...that would be the time to buy.

To: GodGunsGuts; Toddsterpatriot

your real problem is with the message, not the sources.We're making progress here. We agree that I complain whether you justify your investments with a right-wing or with a right-wing rant. What I like is we first do our own research, and then we invest in what research points to. If we later find out something new, then we change the investments and not our findings.

It's easy; it's like yesterday I was talking about income balances and said "it always went up during recessions and down during expansions" --and today I plotted this and said I was "wrong. What came out is that sometimes they match and sometimes they don't."

To: Petronski

>>It's not like that at all.<<

Not all the time. Sometimes it is, sometimes it aint.

46

posted on

12/07/2006 10:41:06 AM PST

by

RobRoy

(Islam is a greater threat to the world today than Naziism was in 1937.)

To: Toddsterpatriot

>>Your anecdotes are much stronger if you don't bother to source them.<<

That is true as well. ;)

47

posted on

12/07/2006 10:41:37 AM PST

by

RobRoy

(Islam is a greater threat to the world today than Naziism was in 1937.)

To: RobRoy

Maybe you should check out Oprah? I heard there are lots of fact free, emotion filled stories that back up your view point. Hope that helps. :^)

48

posted on

12/07/2006 10:45:05 AM PST

by

Toddsterpatriot

(If you agree with EPI, you're not a conservative!)

To: Petronski

49

posted on

12/07/2006 10:52:39 AM PST

by

L,TOWM

(Liberals, The Other White Meat [This is some nasty...])

To: RobRoy

I don't give people individual sources.... ....see if the words stand of their own strength.

That works with points of belief and logic and not when you're trying to base that logic on an observation. If others aren't allowed to make the same observation independently, then they're being expected to take your word for it.

It's the choice between saying "unemployment is down because it's morally good to trust the government", or saying "the BLS announced lower unemployment".

To: expat_panama

And you trust that source?!

;)

51

posted on

12/07/2006 10:54:22 AM PST

by

RobRoy

(Islam is a greater threat to the world today than Naziism was in 1937.)

To: GodGunsGuts; expat_panama; Toddsterpatriot

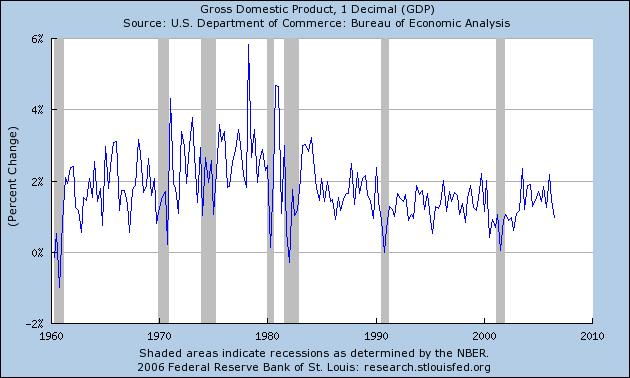

Nice graph. Looks like all those valleys in the 70's, 80's and 90's came during times of high unemployment and recession. I don't see the doomers effectively making the case that we're in a time of recession or that unemployment is high -- or rapidly increasing -- unless you consider 3.5% annualized GDP growth and 4.4% unemployment proof of a recession. You'd also have to explain away the fact that corporate pre-tax profits are up 31% through the third quarter, real consumer spending is about 3 percent above the third-quarter average annual rate and the overall consumer price index has fallen to 1.3% over the past year. 30-year mortgages can still be had for 6% and projections show continued growth for our economy.

No, this time you say it's different because people are buying homes with mortgages they can't afford and once all those unaffordable mortgages catch up with them, doom will certainly befall us resulting in economic collapse. (and gold skyrocketing to $1,650 and ounce, or more!)

Figure 2 shows the distribution of property debt burdens for two years, 1995 and 2004. Notably, the distribution has shifted slightly towards higher debt burdens over this period. However, this shift is small enough that the 1995 and 2004 distributions remain similar. As in every year since 1989 a majority of households that had property debt in 2004 devoted less than 20% of their incomes to servicing that debt.

What we do know from the data is that the share of households with high debt burdens is similar now to what it has been in past years. In 2004 about 5.5% of households with property debt had debt burdens over 0.50, roughly similar to the fraction in earlier survey years.

Figure 3 shows the 2004 distribution of households' home debt burdens by whether or not they have an adjustable-rate property loan. It seems that holders of adjustable-rate loans fit almost exactly the same pattern as other households. They are more likely to have debt burdens in the range of 0.2 to 0.4, but all the differences are small. These statistics suggest that most households that use adjustable-rate loans are not using the lower interest rates to fund insupportably large debts.

I realize that this information is only through 2004 and that in 2005 the use of adjustable-rate mortgages increased thereby increasing total mortgage debt. However, can the doomers here show us that these changes have affected the distribution of debt burdens and that this increase in adjustable rate mortgages will lead to economic collapse? Even though the use of adjustable-rate mortgages has increased, where is the proof that just because households have some of their property debt in adjustable-rate mortgages that they have high debt burdens, and can't adapt successfully to higher interest rates. The trends identified above would indicate that most consumers have a lot more money and sense than doomers here give them credit for.

As the chart below shows, the added debt from those loans has barely impacted our median property debt burden through 2004.

Federal Reserve Bank of San Francisco

52

posted on

12/07/2006 11:24:20 AM PST

by

Mase

(Save me from the people who would save me from myself!)

To: RobRoy

And you trust that source?!Thanks for the compliment, but I honestly don't think that I'm all that important; but the next time you and I are trying to show others something like that there's been a drop in unemployment, we can respond with a BLS link and we can post your say-so.

Anybody who's not satisfied with a double-barrel combo like that is simply not worth our time and effort.

To: expat_panama

I too have learned a lot from you guys. It has definitely forced me to sharpen my understanding in a whole host of areas. It hasn't changed my overall outlook, but it certainly has changed how much significance I give to certain kinds of data. However, in regards to GDP vs. Balance of Income, I think there is a clear correlation, albeit with a few aberrations here and there. Thus, until proven otherwise, Balance of Income (the leading indicator or the two IMO), suggests that GDP will be heading south. Time will tell if I'm correct or not. At any rate, thanks for all the charts and analysis Expat...I'm definitely better off because of it (even if it does eat up ever increasing amounts of my time to come up with valid responses :o)

To: Mase; expat_panama; Toddsterpatriot

I will attempt to answer your analysis point by point (and add a few more), but it will have to wait until I have more time. Thanks for the post (and the challenge!).

To: GodGunsGuts

Off to Google University with you, Gigi.

56

posted on

12/07/2006 12:27:48 PM PST

by

Petronski

(I just love that woman.)

To: Mase

don't see the doomers effectively making the case that ... .... 3.5% annualized GDP growth and 4.4% unemployment proof of a recession

don't see the doomers effectively making the case that ... .... 3.5% annualized GDP growth and 4.4% unemployment proof of a recessionI kept laughing at that line so much I couldn't finish the post until I though about how doomers are so unable to imagine Americans being off.

The US has made so much progress realizing the dream of home ownership. I was looking at the Flow of Funds stats I got from the fed link that Remember shared. By taking the total real estate + mortgages, adjusting for inflation, and dividing by no. households --we get a truly inspiring picture of wealth creation.

Doomers actually know about this stuff, but what they push is the part about the real mortgage "burden" going to an all time high. They won't look at the increased equity position; they're the kind of people who'd rather own a $100 home with $1 debt, than have a $1,000,000 home with $10 debt.

To: Petronski

I'm currently trying to break the bad habbit of using Google. Not only is it a big supporter of hard-left domestic causes, it also assists the Chicoms in censoring their subjects.

And yes, I am forced to look things up all the time...it's called LEARNING.

To: steve8714

My old man built houses. I remember one year (back in the late 70's or early 80's?) he built and sold ONE house. Luckily he had planned ahead and saved up when he was so busy he was "running around like a chicken with his head cut off" (as quoted by one of his carpenters).

59

posted on

12/07/2006 12:49:51 PM PST

by

geopyg

(Don't wish for peace, pray for Victory.)

To: GodGunsGuts

Very interesting chart. This rise since 1990 seems to be very gradual and is along the major trend. The other large falls were preceded by a VERY sharp increase - something we don't see at the moment.

60

posted on

12/07/2006 12:52:56 PM PST

by

geopyg

(Don't wish for peace, pray for Victory.)

Navigation: use the links below to view more comments.

first previous 1-20, 21-40, 41-60, 61-80 ... 181 next last

Disclaimer:

Opinions posted on Free Republic are those of the individual

posters and do not necessarily represent the opinion of Free Republic or its

management. All materials posted herein are protected by copyright law and the

exemption for fair use of copyrighted works.

FreeRepublic.com is powered by software copyright 2000-2008 John Robinson

{kind=link}