A 50 year mortgage which offers various ways of paying it off early would be a good guarantee for many. It’s like having a very high credit limit on your card when you only need a part of that. Security with the option of getting out early.

Longer lifespans make longer payoff timelines viable; mortgagors make far more in interest, satisfying the market; and yet amortizing benefits all.

There is no substitute for owning your first single-family home, even if it is the only home you ever own; and broad real property ownership creates conservatives.

The minute 50 year mortgages are approved, home values will double.

God forbid.

Lumber for a 30x30 two-story house

outside walls

~240’ of 2x6 studs 16” o.c. ~= 180 studs ~= $900

~360’ of 2x6 plates ~= 45 studs ~= $225

inside walls

~120’ of 2x4 studs 16” o.c. ~= 90 studs ~= $350

~120’ of 2x4 plates ~= 15 studs ~= $60

platform framing

24x2 of 2 16’x2”x12” joists [96 16’x2”x12” joists][Note: I-beams would usually be used]

+

4 16’x2”x12” platform ends ~= $3000

subtotal ~$4500

plywood

roof x 30’x30’ ~= 1000 sq. ft. ~= $1,100

floors ~1800 sq. ft. $42 4’x8’x3/4” sheet ~= $2,400

sheathing ~1920 sq. ft. ~= $2,000 [Note: Oriented Strand Board would normally be used]

truss wood

16(1+30/2 24” o.c.) x 70’ ~= 140 2x4 studs ~= $560

wood for house ~= $11,000 total

park side Upper West Side

20 blocks of brown stone about 900 feet long and 30 feet high with 60% coverage.

20*2*900*30*.6

20*900*36

648,000 square feet of brown stone

Park Slope, Brooklyn Heights, Fort Greene, Upper East Side, Upper West Side

~3,240,000 square feet of brown stone

~$25 million, total

The federal government owns the navigable airspace. What I suggest is closing that airspace to airports within 50 miles of any unaffordable area to soften the housing markets in those areas.

I also suggest building new state capital cities about once a decade to provide abundant affordable housing with amenities.

No, no and no again.

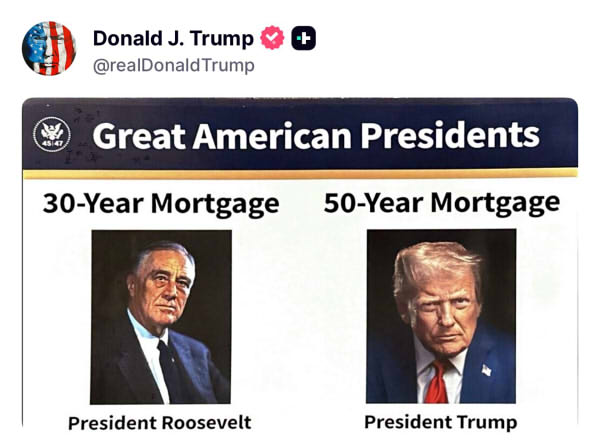

You already pay, in total (due to the total interest that will be paid) much more than most people realize on a 30 year mortgage.

On a 30 year mortgage for $400,000 at a 6% annual interest you’ll actually pay $463,323 by the end of the mortgage.

On a 50 year mortgage for $400,000 at a 6% interest rate you’ll actually pay $714,258 in total.

What is needed is a big dose of DEFLATION in the current housing prices that are highly inflated. Yes, sellers who are among more recent buyers will have to take a hair cut, and sellers who bought many years ago will have to not get the current inflated prices. I don’t know what else is going to “correct” the housing markets that are the most inflated.

If you need a 50 year mortgage, you can’t afford a house, period.

Aw what the hell. Why not? You never really own your home anyway, thanks to onerous and perpetual property taxes.

“You Will Own Nothing And You Will Be Happy”. Probably the worst idea I have heard in my lifetime. Canceling the 30 year would be a more appropriate, although temporary painful, solution. At the end of the day the monthly payment is always going to be about 1/3 of the median monthly pay for the area. monthly “Affordability” with credit is a paradox, it is going to come down to how much money it takes compared to your lifetime earnings.

Is this the Bee?

Worst. Idea. Ever.