What we got here is that people say Trump likes Glass Steagall but so far I haven't been able to find Trump saying it. If anyone has a link to a video/audio of Trump saying this pse share.

In the meantime he's going to win and nothing can depress our enthusiasm.

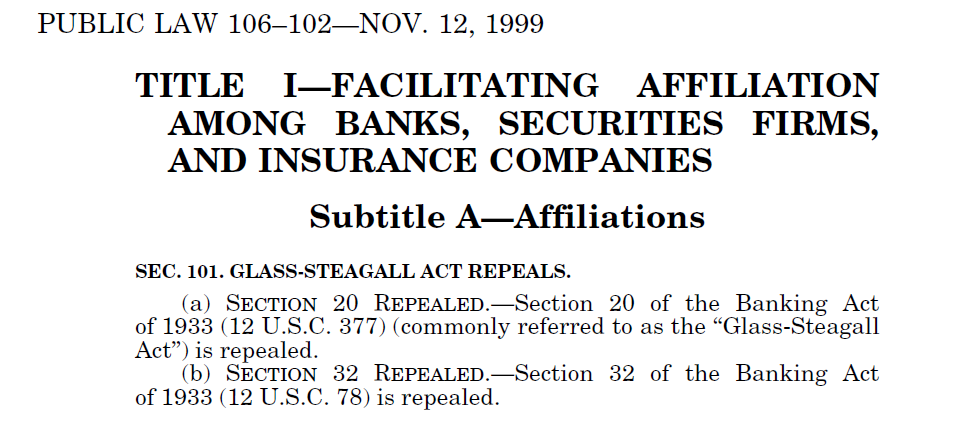

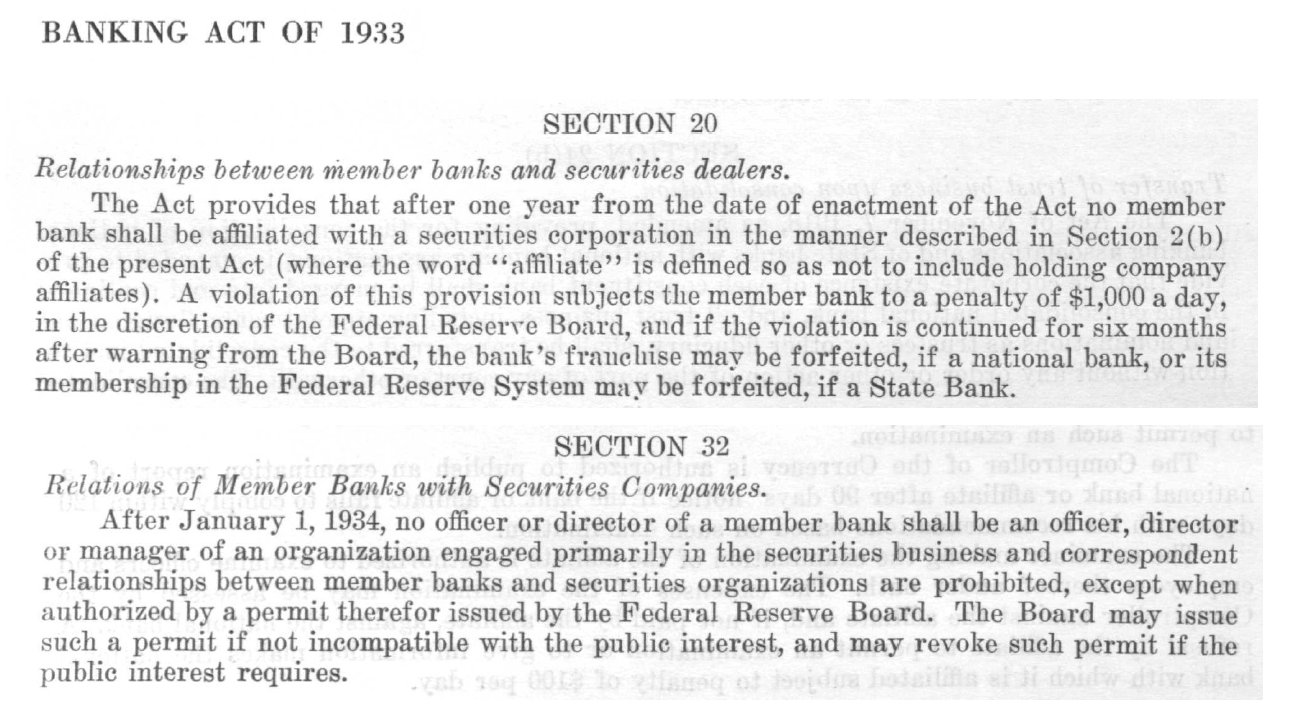

fwiw, here are all 32 Sections of the original 1933 Glass-Steagall Act, and this is the 1999 Actthat included this section:

--that removed Sections 20 and 32 or the 1933 act--

and still left in all the other 30 sections with that stuff about separation of "commercial and investment banks". The left-wingnut press keeps saying that the 1999 'deregulation' caused the 2008 crash, but that's so we don't blame the real culprit for all those forced minority loans.

Navigation: use the links below to view more comments.

first 1-20, 21-24 next last

To: expat_panama

Banks need to be broken up, Glass-Stegall brought back, Dodd-Frank done away. What we have now only benefits the top 10% of the population.

2 posted on

10/28/2016 4:27:25 AM PDT by

rstrahan

To: expat_panama

Bunkus. That the biggest economic downturn since the Depression occurred AFTER repeal of Glass-Steagall is absolutely NO accident.

It needs to come back.

Don’t listen to the establishment, who desperately want to keep their gravy train rolling.

3 posted on

10/28/2016 4:29:01 AM PDT by

freedomcrusader

(Proudly wearing the politically incorrect label "crusader" since 1/29/2001)

To: expat_panama

I would advise him to speak to people in the collections industry at length before even thinking about it. Extending credit is not the way to dig anyone out of poverty. That’s a bandage that will come back to bite the economy in a huge way. You’re going have to get more of them employed. I think they are ready and willing to work but they got to have jobs to go to. Need to make America a hotbed of innovative technological revolution and do our own manufacturing somehow. How to keep the costs down and pay our workers enough to live on. That’s the hard part.

To: expat_panama

The repeal of Glass-Steagall set the stage for the collapse of the mortgage market in 2007.

6 posted on

10/28/2016 4:34:12 AM PDT by

jonrick46

(The Left has a mental disorder: A totalitarian mindset..)

To: expat_panama

Minority loans were a good portion of the problem, but it would have collapse anyway. Whites, Asians, etc in CA, Vegas, and Florida were doing negative amort alt-A liar loans and 0 down loans in record numbers as well - in far greater total $ amounts than minority loans. That doesn’t even count the piggy back HELOC loans whites were taking out either. Glass-Steagall should either be reinstated or we should move to a 20-25% fractional reserve system over time rather than the 10% we normally allow and as low as 3-4% during the 2006-2008 time (bear sterns blew up with 50:1 leverage).

8 posted on

10/28/2016 4:36:11 AM PDT by

rb22982

To: 1010RD; A Cyrenian; abb; Abigail Adams; abigail2; AK_47_7.62x39; Alcibiades; Aliska; alrea; ...

It's Friday! Stocks were crashing yesterday almost to the support levels we've been enjoying for months now. While it was yet another bearish 'distribution day' this morning's futures are mixed, these mostly positive and these others at -0.78%. Metals seem flat/sideways both w/ current prices and in futures contracts.

Everyone must be looking for an election year rosey GDP:

8:30 AM Chain Deflator-Adv.

8:30 AM GDP-Adv.

8:30 AM Chain Deflator-Adv.

8:30 AM Employment Cost Index

10:00 AM Michigan Sentiment - Final

Also:

Don't Forget Sen. Warren, That Corporations are People - Ben Stein, TAS

Stocks Already Predicting Clinton/Trump Winner - Jen Wieczner, Fortune

Who Will Pay for HRC's Tax Code Social Engineering? - Alex Brill, RCM

Don't Assume that Next President Will Face a Recession - Neil Irwin, NYT

Here's Who Has the Billionaire Class Terrified - John Nichols, The Nation

Post Obama, Quest to Keep Behavioral Economics - David Johnson, TNR

It May Be Time to Turn Away From Index Funds - Philip van Doorn, MW

Global Policymakers Starting to Shiver - Jeffrey Snider, RealClearMarkets

China's in Better Shape Than Its Critics Believe - John Redwood, Telegraph

To: expat_panama

IBD upset with Trump, so they Fraud their poll to a +7 D.

13 posted on

10/28/2016 4:48:02 AM PDT by

BigEdLB

(Take it Easy, Chuck. I'm Not Taking it Back -- Donald Trump)

To: expat_panama

I consider myself a well-informed individual and I STILL didn’t realize just how much banks were ripping people off until my boss (with an alphabet soup of accolades and degrees) showed me. It’s no frigging wonder Occupy went from nothing to international nightmare seemingly overnight. Bring back GS, NOW!

To: expat_panama

no, bring back glas steagall. If you’re going to provide deposit insurance, you can’t allow banks gamble with that money

15 posted on

10/28/2016 4:53:42 AM PDT by

4rcane

To: expat_panama

He is certainly upsetting the money changers.

Lord, please protect Donald Trump.

16 posted on

10/28/2016 4:55:04 AM PDT by

polymuser

(Enough is enough!)

To: expat_panama

What needs to come back is the Bible.

Sweat of the brow. Tithing. Charity begins at home. Thou shalt not steal. Thou shalt not covet. Saving in times of plenty, preparing for times of famine.

The last is particularly relevant to banks and the economy at large, and their relationship to individuals.

It was not so long ago that banks only loaned out what they had on deposit, and they only loaned to those who could pay it back. Banks charged a reasonable interest rate to borrowers which covered overhead, plus a profit.

The banks, in turn, paid interest to savings depositors, incentivizing individual savings that could then be loaned out, and repaid to the depositors.

Wise, frugal people prospered.

Then the government decreed that common sense and incentives were racist, and that “income inequality” must be eliminated, by disincentivizing the productive folks and rewarding loafers.

And here we are.

19 posted on

10/28/2016 5:10:55 AM PDT by

mumblypeg

(We've had a p***y in the White House for 8 years. Make America Macho Again.)

To: expat_panama

Restore Glass-Stegall and strike RFA (the original source for mandated Non Performing Loans) and make it legal for bankers to shoot anyone that protests in front of their house about “minority” rights.

20 posted on

10/28/2016 5:11:05 AM PDT by

cashless

(Obama told us he would side with Muslims if the political winds shifted in an ugly direction.)

To: expat_panama

Only the banksters fear Glass-Steagall, which is reason enough to pass it.

22 posted on

10/28/2016 5:18:26 AM PDT by

Jim Noble

(Look out kid, they keep it all hid)

To: expat_panama

25 posted on

10/28/2016 5:52:38 AM PDT by

Beagle8U

(Giggles the pig for POTUS - 2016)

To: expat_panama; All

Trump is right again and you are siding the Globalist/Establishment and the Central Banks.

All it leads to his bubbles, then crash and consolidation. Then it makes it easier to command and control fewer companies.

The repeal of Glass Stergall has been disastrous. Less than 10 years after it was repealed. We are currently sitting on top of another derivatives bubble that’s bigger than 2008. Only 8 years after the first collapse.

Being able to resale a morgatge a thousand times is criminal too. That’s what you get with the 1999 repeal. It failed us in 1929, 2008 and it’s about to fail us again after the election.

BTW, it’s not liberal like you are claiming to be for Glass Stegall. Its fiscally conservative to be economically responsibility which is conservative. Liberal is being against Glass Stegall.

To: expat_panama

I never took Econ 101, but this is how I see it.

By and large, the Gramm, Leach Bliley Act of 1999 was passed to legitimize the then illegitimate merger between Citicorp and Travelers Group. Clinton and Sec. of Treas. Robert Rubin pushed hard for its passage. Now the banks had access to mountains of money they could use for sub-par loans while passing the liability on to investors and depositors. Previously, Rubin had been successful in opposing Commodity Futures Trading Commission oversight of over-the-counter credit derivative trading (slicing and dicing) which, with later legislative exemption, played no small part in the collapse.

Within a week of its passage, Rubin resigned from the Treasury and a month later (vacation?) joined the board of CitiGroup.

Everybody was playing fast and loose at the time and although the passage of GLB 1999 which removed part of Glass Steagall was not the *sole* cause of the collapse, the implosion would not have happened without it. It was one of the “wheels within wheels” that were spinning with the goal of getting money out of the pockets of the public and into the wallets of a few. After all, our government is nothing if not the greatest extortion racket ever devised.

32 posted on

10/28/2016 6:47:23 AM PDT by

Roccus

(When you talk to a politician...ANY politician...always say, "Remember Ceausescu")

To: expat_panama

We need Glass-Steagall because look at how that very law prevented economic meltdowns in 1987 and 1997 because bank assets were protected from stock market rapid falls. When Lehman Brothers collapsed in 2008, a lot of banks collapsed with catastrophic results—and we’ve still not recovered fully from that crash.

33 posted on

10/28/2016 6:58:15 AM PDT by

RayChuang88

(FairTax: America's economic cure)

To: expat_panama

In the simplest of terms I’m for whatever the elite are against until I’m convinced otherwise. Banking was already a license to steal before Glass Stegall was repealed but it was at least a steady business.

Now we lurch from one crisis to the next. Glass Stegall had a good reason for being that needed to be understood before it was destroyed.

Greed is all I can see as a motive any more. The ledger is out of balance between rich and the rest. Like a monopoly game, when one player has all the property and money nobody else can buy or sell. Everyone is a rent slave to the winner.

We are almost all rent slaves to the winners now. Winners can be the property owners or the tax collector but either way we are slaves to them.

36 posted on

10/28/2016 7:16:09 AM PDT by

Sequoyah101

(It feels like we have exchanged our dreams for survival. We just have a few days that don't suck.)

To: expat_panama

Glass-Steagall was a bad law written based on bad history. In 20s the LEAST likely banks to fail were those that had brokerage houses.

38 posted on

10/28/2016 7:19:02 AM PDT by

LS

("Castles Made of Sand, Fall in the Sea . . . Eventually" (Hendrix))

To: expat_panama

46 posted on

10/28/2016 7:52:35 AM PDT by

Ray76

(DRAIN THE SWAMP)

Navigation: use the links below to view more comments.

first 1-20, 21-24 next last

FreeRepublic.com is powered by software copyright 2000-2008 John Robinson