Posted on 01/13/2016 9:27:00 AM PST by NRx

You have a better chance of getting hit by lightning in a frog thunderstorm than you do winning the Powerball, but hey, it's always fun to play billionaire. If you were to win (and you won't), there are a few things you should to do to protect and optimize your winnings.

http://lifehacker.com/winning-the-po...

Ah, the age old question all lottery winners (well, big winners) have to contend with: Do you take the annuity or the lump sum amount?

With the annuity, you get your payout over time, and you'll get more money. If you win this Powerball Jackpot, you can opt for 30 annual payments that average to about $37 million, after Federal taxes. That adds up to just over a billion dollars over time. (This varies depending on what state you live in, because you have to consider those pesky state taxes).

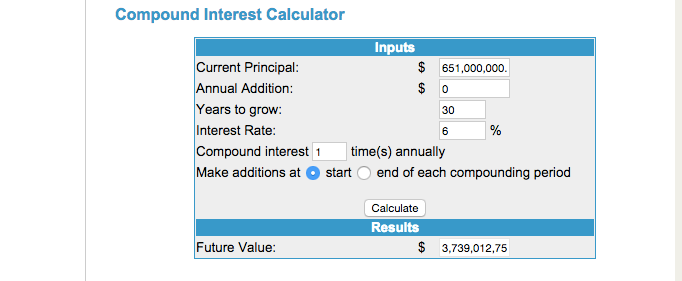

With the lump sum, you get all your money at once, but after Federal taxes, that's about $651 million. Pretty good, I guess, but it's no billion dollars. Here's the thing, though: even though the annuity adds up more over time, lump sum could still be a more lucrative option if you invest it, thanks to a little thing called compound interest. Let's say you invest that $651 million into the broad stock market, which earns about 6-7% each year, on average, after inflation. To keep things simple, we'll assume you don't have state taxes. In five years, you'd earn $871 million. In 30 years--the payout term for the annuity--you'd earn $3.74 billion. That more than makes up for the money you lost by opting for the lump sum amount.

It's not quite that simple, though. For one, you have to pay taxes on the money you earn from investing, and there's a big tax advantage to the annuity option. Tax Lawyer David Hryck explains:

If you take the lump sum, you will be paying taxes twice. You pay on the prize itself and again on your investments. If you go the annuity route you will pay taxes on each installment but you will not pay taxes on your investments of the money while the government essentially holds your winnings for you. Over time, this will add up for you as your winnings grow with no tax stipulations.

With the annuity option, Powerball basically invests the money on your behalf, and, according to Hryck, you earn a pre-tax rate of about 2.8%. That's not much, and you can do better investing on your own, but remember: that money is growing tax-free. As The New York Times points out, "you'll never beat the effective tax rate of zero on the investment income earned inside the Powerball annuity."

http://www.nytimes.com/2016/01/13/ups...

Of course, you can invest your annual annuity payout in the broad market, too, and then you pay taxes on those earnings as well. Like we said, it's complicated.

These scenarios also assume you'll invest your entire winnings, which is unrealistic (that private island isn't gonna pay for itself). They assume you have decades to invest and wait out market slumps. There are so many numbers to crunch and the outcome really depends on how long you have to invest, what kind of yield you can expect, and where you live.

A multimillionaire shouldn't have to do this much math.

Thankfully, Business Insider crunched some numbers with a lottery a few years ago, and here's what they concluded:

if you can score a rate of return somewhere between 3% and 4%, you're still better off with the lump sum...Factoring in investment, though, it only makes sense to take the lump sum if you think you can get an altogether reasonable rate of return.

Even the most basic, set and forget investment portfolio averages 6-7% on average, so those numbers point to lump sum. But it basically comes down to the advantage of investing the lump sum vs. the tax savings of the annuity. And most experts seem to think the tax savings of the annuity outweigh the return of the lump sum. You might also choose the annuity if you have a hard time managing your money.

Before rushing out to claim your ticket, take a moment to soak it all in. You're a multimillionaire, I know! It's time for couch jumping and champagne popping. However, if there's one thing I've learned from sitcoms, it's that acting impulsively when you win the lottery always backfires.

You need time to understand the rules and come up with a reasonable plan. And don't worry about missing the deadline: in most states, you have 180 days to claim your ticket. (Mark your calendar, though, because you'll be kicking yourself if you miss that deadline!)

Make a copy of your ticket and put the original in a safe place (like literally, a safe.) When friends, family, and creditors find out you won, they'll start hitting you up nonstop. Forbes recommends the following strategy to avoid this:

...check state rules to see whether you can dodge them all by remaining anonymous...rules on winner publicity vary by state. In New York, for example, winners' names are a public record. Elsewhere it may be possible to maintain your anonymity by setting up a trust or limited liability company to receive the winnings, says Beth C. Gamel, a CPA with Pillar Financial Advisors in Waltham, MA. A client of Gamel's who won a past lottery did that, and had a lawyer claim the prize on behalf of of the trust. In South Carolina, where the Sept. 18 winner bought his or her ticket, it's also possible to remain anonymous.

If you're married, your spouse is entitled to some of the winnings. According to Legal Zoom, spouses' earnings are generally considered marital income, so if you buy something with those earnings--even if it's a lottery ticket--that item becomes marital property. If you're going through a divorce and you won the lottery, your ex might be entitled to some of the winnings, too. It depends on how far along you are in the divorce and where you live (laws vary by state).

Maybe you won the Powerball as part of an office pool. In thie case, things get a little messy. You should've thought about that before asking Noel in accounting to go in with you, but here you are. In most states, there can only be one payee per ticket. So you'll have to create a single entity to represent all of the winners. AmericanBar.org explains how this works:

Thus, in a multiple- beneficiary situation, it is advisable to create an entity because if only one person in the pool claims the prize, when that person distributes shares of the prize to the other members of the group, it could be a taxable gift. In addition, only that individual will receive the W-2G, reporting the lottery winnings as 100 percent taxable to him or her for income tax purposes. Further, the other members of the pool may not be comfortable with just one member claiming the prize as the winner, individually... In these instances a group arrangement should be used for all purposes and should be documented appropriately.

A good lawyer will walk you through these issues, but it helps to know what to expect. Once you do claim your ticket, you'll have another 60 days to decide how you'll receive payment.

http://lifehacker.com/5826959/how-to...

Congratulations--you're in the one percent! This means you'll pay a ton of taxes, but unlike your peers, you won't get a chance to think about how to shelter your millions with tax loopholes. You've gotta pay up.

The Powerball website crunched the numbers for you so you can see what you'll pay in both Federal and state taxes, depending on where you live, and depending on whether you take the lump sum or annuity.

Assuming you quit your job, you'll have to pay estimated quarterly taxes now, too. A good CPA will help you figure this out so you can avoid tax penalties. It's pretty easy, though. When you don't have a full-time job, you don't have an employer to make regular tax payments during the year on your behalf. So you have to make these payments yourself every few months, using IRS Form 1040 ES, if you have any income during the year. You can pay these taxes online, too.

http://lifehacker.com/268406/pay-you...

Keep in mind: you're also in the highest possible tax bracket now, too. For 2016, that means your federal income tax rate is 39.6%. Again, you'll pay all of your taxes at once with the lump sum, so that rate won't change. However, if you opt for the annuity, your rate could very well change over the years. Here's how one tax pro explained it to Business Insider:

"As we know tax rates are always changing. If you take a lump sum you are looking at a 39.6% rate. If you take an annuity over the next 30 years the rates will probably be very different when you receive each payment." So people who expect that the top tax rate will decrease over time -- or that the Flat Tax crowd will win -- should take that annuity.

On the other hand, if you think the tax rate will only get higher over time, you'll want to take the lump sum.

At the very least, you're going to need an attorney, a Certified Financial Planner, and a tax preparer.

An estate attorney will help you figure out how to set up a Will and Trust as well as other complicated legal documents. Here's what estate lawyer Barry Nelson says you'll need:

In preparing a Will and Trust, the lottery ticket winner will have to consider difficult non-tax issues. For example, at what age should the winner's children inherit such large sums of money in the event of the lottery winner's death. Most of my clients believe that it is advantageous to delay large distributions to younger family members until they finish college and have work experience so they obtain a healthy work ethic.

Find a good lawyer by asking a trusted friend or family member or running a search on the American Bar Association website. You might even reach out to past lottery winners, suggests Richard Morrison, who won $165 million back in 2009.

http://business.time.com/2012/11/29/pow...

undefined business.​time.​com

When you meet with your lawyer or interview them over the phone, you should feel comfortable, and they should explain things clearly. And watch out for this big red flag, as lawyer John M. Phillips points out on his website:

Do NOT agree to allow them a percentage of your winnings or anything crazy like that. If they ask... that's the wrong lawyer. Just find someone who you trust and come up with fair retainer and/or hourly compensation to help you make good decisions and protect you from people who will look to separate you from your windfall.

When you look for a financial planner, make sure it's a Certified Financial Planner, who takes a fiduciary oath and is legally required to act in your best interest. Ideally, you want a fee-only financial advisor, too. This CFP should also be able to help you with taxes or refer you to someone who can help.

http://twocents.lifehacker.com/how-to-find-an...

A good lawyer will help protect your money. They'll suggest a series of legal moves and insurance products to help protect you against all the things that might possibly go wrong with your money: lawsuits, creditors, divorce.

Forbes explains how this asset protection plan works in a little more detail.

The best defense is to erect a variety of roadblocks that make it difficult, if not impossible, for creditors to reach your money and property. These asset protection strategies, as they are called, can range from relying on state-law exemptions to creating multiple barriers through the use of trusts and family limited partnerships or limited liability companies. It may be possible to rely on a variety of strategies, either separately or in combination with each other.

For example, Morrison told Time that his lawyers even suggested kidnap and ransom insurance to protect his family. He says he opted out but hired security to protect his home and children. He also suggested claiming your ticket at a lottery office far from your home town.

Of course, it's probably a good idea to pay off old debt and learn a few good financial habits, too. You're rich, I get it, but if it can happen to Wayne Newton, it can happen to you. Plus, when you have debt to pay, that means you're paying interest. Obviously, you want to pay all of that off at once so your debt interest doesn't offset the interest you earn from investing.

In general, though, you'll probably be fine. With some proper planning and a basic understanding of how the system works, you should be in pretty good shape. That is, assuming you actually win.

I am going to buy a large sample of every CHEESE made.

I remember when the Georgia Lottery was first established and the very first winner was asked what he was going to do with his winnings and his answer was, “ I’m going to buy me a doublewide and move to Alabama”. :-)

I don’t know where you can get 2% interest on a savings account these days.

The last 2 savings accounts/money market accounts I had paid a whopping 1/4 of 1% interest. 1/8 of what you are talking about.

Still more than twice as good a payout than lotto.

First, your family’s safety and security is Priority 1.

Next:

Short example of what’s possible:

$1.5B pot

$930M Lump sum, pre-tax.

~$560 after tax payout

30% of taxable income is max amount of deductible, charitable contributions.

~$280M

At a 40% tax rate, ~$110M would be refunded in 2017.

Give away the remaining $280M

In 2 yrs:

You’ll have given away all of the original $560M check and still have $110M.

85% of possible # combinations have been sold so odds suggest a strong probability of one or more winners tonight. BUT if there is no winner Saturday’s jackpot will start at $2 billion ($1.24 billion pre-tax cash).

I think I would try to build a state of the art animal rescue facility..........

Never let your name become public knowledge. That’s the most important rule of all.

If my very small "investment" should pay off big time tonight, I'll destroy my cell phone and go underground to avoid the relatives and charities that will be hounding me immediately.

Then, once I'm rational, I'll make some informed decisions that will involve gifts to my sister and my wife's sisters, large donations to reputable charities working on ovarian cancer research (in memory of my mother), and will tie the rest up in investments that will provide an eternal revenue stream.

Not one nickle to a politician or to a school or anything like that.

“WHY would anyone older than 50 ask for 30 annual payments????”

You can set up a trust that will continue to get the payments. Depending upon how you handle it when you cash in the ticket.

Puerto Rico? Chicago? Dallas?

Marry the girl of my dreams. Failing that, fast cars and slow women.

bkmk

Best movie ever.

Out of 42,000 issuers and over a million individual issues, there are 500-600 distressed with a fraction of those in actual default.

Awww... Good for you. Best response yet.

I have had my eye on a few South Pacific islands and large tracts of land. Would have to buy one (or two or three) of those and a deluxe fishing boat and a Matrix76 catamaran. Would sponsor some good causes (like the above comment to end Freepathons) and make sure I had a trust set up to take care of all my family members and a few close friends.

Definitely not going to party a bunch of it away with a ridiculous posse like some of the rappers do. Not into jewelry.

Wouldn’t mind buying a gold mine in Alaska or the Klondike for some fun summer adventures. Would love to get a nice motorhome and travel around the U.S. and see the sights and meet the people.

Then in year 2...

I don’t mind paying the “voluntary tax on the stupid” when I get a few lottery tickets. It’s worth a few bucks to rev up the imagination about all the “what if” ideas.

Superjumbo CDs ($100k deposit)

Everbank 2.35%

5 other banks 2.00% or higher. (Including Discover and State Farm Banks)

http://www.bankrate.com/funnel/cd-investments/cd-investment-results.aspx?ic_id=CDI_compare_rates_module:www.bankrate.com:5_Yr_Jumbo_CD&local=false&prods=26

For a $10k 5 year CD, ELoan is offering 2.45%; Everbank will give you 2.35% for as little as $1,500.00

You can take what Brick-n-Mortar bank offers when you walk in, or you can shop online for some much better returns.

(Note numbers given are APY over the life of the loan; posted rates slightly lower. Returns may vary based on how the bank posts interest).

Special for small savers - Barclays is offering 2.25% on a 5 year with no minimums.

Note - offering change frequently - go to Bankrate to look for current. Top listings are usually advertised, and may not be the best.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.