Skip to comments.

Bloomberg Hides Government Causes of Financial Crisis

Townhall.com ^

| January 8, 2012

| Peter Ferrara

Posted on 01/08/2012 9:30:41 AM PST by Kaslin

click here to read article

Navigation: use the links below to view more comments.

first 1-20, 21-27 next last

1

posted on

01/08/2012 9:30:43 AM PST

by

Kaslin

To: Kaslin

Did I miss the role Obama took even though he was listed in the headline??? Trillion upons trillions spent, frittered away.

2

posted on

01/08/2012 9:50:46 AM PST

by

Freddd

(NoPA ngineers.)

To: Freddd

The fallacies of the last three Presidents, Clinton, Bush, and Obama, came together to cause the devastating financial crisis-——————

What role did Obama play? Nothing mentioned...

3

posted on

01/08/2012 9:52:09 AM PST

by

Freddd

(NoPA ngineers.)

To: Kaslin

4

posted on

01/08/2012 9:56:05 AM PST

by

Mortrey

(Impeach President Soros)

To: Mortrey

Ann Barnard isn’t she the one to whom Corzine is linked?

5

posted on

01/08/2012 10:01:14 AM PST

by

Kaslin

(Acronym for OBAMA: One Big Ass Mistake America)

To: Kaslin

She closed her brokerage firm BECAUSE of what Corzine did with MF Global.

She did it for the good of her clients because she believes there is 100% fraud in the market, and she’s telling everyone to get out.

Listen to the video...she admonishes everyone to buy guns, too.

To those who say “I can’t afford to lose the penalty for taking my money out”, she says they won’t have ANY money to take out if they don’t move quickly.

6

posted on

01/08/2012 11:06:05 AM PST

by

Mortrey

(Impeach President Soros)

To: Freddd

>>What role did Obama play? Nothing mentioned...

Uhuh. Observe what we DIDN'T hear in September/October 2008...

"Well, I'm glad my opponent brought up the economy. Mr. Obama, isn't your campaign's National Finance Chairwoman Penny Pritzker -- and didn't her Chicago Family-owned Superior Bank fail in 2001 from doing subprime loans for ACORN?"

Follow the....

http://www.campaignmoney.com/finance.asp?type=in&cycle=08&criteria=pritzker&fname=penny

Billionaire business mogul Penny Pritzker is a member of one of America’s richest families and was the Finance Chair for the presidential campaign of Barack Obama. It was Pritzker that led the prolific, and illegal, fundraising that helped power Barack Obama’s presidential campaign. She was the chair of Chicago-based Superior Bank’s board for five years. Pritzker was into subprime lending before it became all the rage starting in around 2000. Prtizker's chairmanship was to concentrate on sub prime lending, principally on home mortgages, but for a while in subprime auto lending, too, after the Pritzkers' bank acquired its wholesale mortgage organization division, Alliance Funding, in December 1992.

Back then they called it "predatory lending." Superior Bank went belly up in 2001 with over $1 billion in insured and uninsured deposits; 1,406 depositors lost much of their life savings. This collapse came amid harsh criticism of how Superior’s owners promoted sub-prime home mortgages.

On Nov. 1 [2002] the Federal Deposit Insurance Corp. pointed the finger at Ernst & Young, Superior’s auditor, in a fraud suit filed in federal court here. But that action came two months after a group of Superior depositors accused the bank’s owners and directors, including two members of the Pritzker family, of racketeering.... |

|

[snip]

...Pritzker is chairman of Classic Residence by Hyatt, luxury senior living communities in 11 states; chairman of The Parking Spot, which owns and operates off-airport parking facilities in nine cities; chairman of the credit data company TransUnion and chairman of Pritzker Realty. She also sits on the board of Global Hyatt and plays a role in numerous non-profit groups, including serving as chairman of the Olympic village portion of Chicago’s bid to win the 2016 Summer Games.

Nudge nudge nudge...

7

posted on

01/08/2012 8:23:08 PM PST

by

LomanBill

(Animals! The DemocRats blew up the windmill with an Acorn!)

To: Kaslin

Losses on subprime mortgage-backed securities didn't start shaking financial institutions until 2007,

Uhuh.

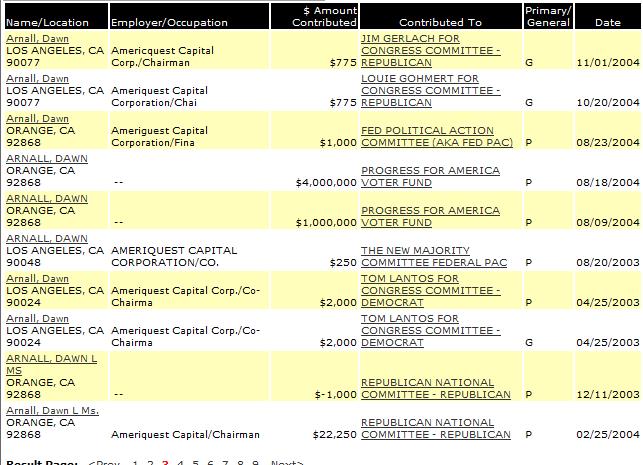

Arnall, paging the Godfather of Subpri... err, Ambassador Roland Arnall, please come to the White Hut courtesy phone....

"Oops"

"Oops"

Where's RICO, LEOs?

8

posted on

01/08/2012 8:28:57 PM PST

by

LomanBill

(Animals! The DemocRats blew up the windmill with an Acorn!)

To: aflaak

9

posted on

01/08/2012 8:40:27 PM PST

by

r-q-tek86

("It doesn't matter how smart you are if you don't stop and think" - Dr. Sowell)

To: Kaslin

The CRA and other government mandates didn’t cover Wall Street investment banks like Goldman Sachs, pure mortgage lenders like Ameriquest, nor hedge funds like John Paulson.

The IBs, pure mortgage lenders, and hedge funds cranked out trillions of dollars worth of subprime paper and derivatives, all in the private sector and all in competition with Fannie Mae and Freddie Mac. They did it without any government pressure. They did it because they were making a ton of money in the subprime market.

Peter Ferrara is perpetuating a politically convenient myth, that “the government caused it all”, which gets treated like Gospel around here because a lot of conservatives start with the belief that only government could do something so stupid and damaging, and the facts be damned if they indicate otherwise.

Well Wall Street spent a whole lot of money paying politicians of both stripes to dismantle the Glass Steagall act and to pass laws to prevent regulation of the derivatives industry. Google “Gramm–Leach–Bliley” and the “Commodities Futures Modernization Act of 2000”. The private shadow banking sector was in the subprime market up to their eyeballs, without government pressure, and they did a whole lot of stupid and destructive things, courtesy of their refusal to price risk correctly due to their idiotic belief in David X Li’s Gaussian Copula Function.

HUD and the CRA ought to be scrapped. But so should the claim that the government caused the crisis and that the lending business was simply an innocent victim of government regulation.

10

posted on

01/08/2012 9:12:43 PM PST

by

Pelham

(Islam. The original Evil Empire)

To: LomanBill

“Where’s RICO, LEOs?”

There may not be a way to prosecute the likes of Arnall. The shadow banking firms lobbied to keep themselves exempt from laws that cover banks.

11

posted on

01/08/2012 9:17:42 PM PST

by

Pelham

(Islam. The original Evil Empire)

To: Pelham

There may not be a way to prosecute the likes of Arnall. The shadow banking firms lobbied to keep themselves exempt from laws that cover banks.

"Argent is safe from investigation because the government got their $325 million settlement from Ameriquest and won't be looking into Argent, per the settlement agreement. "

Dear Mr. Lee: I was previously employed by Argent Mortgage for two and a half years and managed, among other areas, the corporation's fraud investigation, borrower complaints and repurchase departments. There are currently over 568 open fraud investigations involving hundreds of brokers and hundreds of millions of dollars in fraudulent loans that are being covered up by top executives in the company. If a broker sustains a certain monthly volume, Argent management looks the other way and, not only does not suspend the bad brokers, but knowingly sells these fraudulent loans on the secondary market to unwitting investors.

I was terminated today and left with just my purse in tow, but I have names of individuals in the company who need to be served with subpoenas to enable them to turn over their spreadsheets and boxes full of documentation and evidence of all the fraud they have found that is being covered up by Argent Mortgage's executive management. The state regulators need to know the truth about the blind eye Argent turns to the fraud perpetrated on innocent consumers by high volume brokers. They also need to be aware that Argent knowingly bundles these fraudulent loans and sells them as mortgage-backed securities on Wall Street, thereby compromising the SEC, as well as our country's economic stability.

At a recent fraud seminar attended by hundreds of mortgage lenders in Washington D.C. a week ago, an attorney who works for Argent's retained law firm, Buchalter Nemer, stood up and told the seminar attendees that the wholesale lenders in the audience had better beware, unless their name is Argent. Argent is safe from investigation because the government got their $325 million settlement from Ameriquest and won't be looking into Argent, per the settlement agreement. I hope this isn't true because Argent Mortgage funded over $50 billion in 2005 and is gearing up to fund well over $80 billion dollars of fraudulent loans in 2007.

Nifty ehh?

12

posted on

01/08/2012 9:23:16 PM PST

by

LomanBill

(Animals! The DemocRats blew up the windmill with an Acorn!)

To: Pelham

their refusal to price risk correctly due to their idiotic belief in...

"We didn't truly know the dangers of the market, because it was a dark market," says Brooksley Born, the head of an obscure federal regulatory agency -- the Commodity Futures Trading Commission [CFTC] -- who not only warned of the potential for economic meltdown in the late 1990s, but also tried to convince the country's key economic powerbrokers to take actions that could have helped avert the crisis. "They were totally opposed to it," Born says. "That puzzled me. What was it that was in this market that had to be hidden?"

13

posted on

01/08/2012 9:26:27 PM PST

by

LomanBill

(Animals! The DemocRats blew up the windmill with an Acorn!)

To: LomanBill

Yes, infuriating and not a surprise.

Argent and Ameriquest were two of the largest subprime houses. They are largely forgotten because Argent was a division of Ameriquest and was later gobbled up by Citigroup.

And Ameriquest is one of the All Stars over at the Mortgage Lender Implode O Meter, and therefore no longer exists.

14

posted on

01/08/2012 9:38:33 PM PST

by

Pelham

(Islam. The original Evil Empire)

To: LomanBill

Brooksley Born was one of the few heroic figures who tried to prevent the subprime mess, although her attempt to regulate the OTC derivatives market was defeated.

It wasn’t like every regulator refused to do their job, although I think that was certainly the case with Greenspan and Cox over at the SEC. There were state attorneys general who investigated subprime lending abuses but were prevented from doing anything about it.

15

posted on

01/08/2012 9:49:34 PM PST

by

Pelham

(Islam. The original Evil Empire)

To: Pelham

[They are largely forgotten because Argent was a division of Ameriquest]

Yep.

And my observation was that the SEC couldn't find its own arse with both hands and a SQL statement telling them exactly where to find it... and a few thousand Liar Loan applications for which the AAA FICO score had been fabricated.

Largely forgotten? Yeah, fahgedaboudat.

16

posted on

01/08/2012 10:01:21 PM PST

by

LomanBill

(Animals! The DemocRats blew up the windmill with an Acorn!)

To: LomanBill

Cox’s tenure at the SEC bought into the same idea that you posted about Greenspan, the belief that the financial markets would self-regulate.

That experiment sure worked out great. It took 60 some years to forget the lessons of the 1930s and to dismantle the separation of commercial and investment banking. Ten years for investment bankers to blunder into another major financial crisis.

17

posted on

01/08/2012 10:08:43 PM PST

by

Pelham

(Islam. The original Evil Empire)

To: Pelham; Liz

[Ten years for investment bankers to blunder into another major financial crisis.]

And all of the above took place in the context of a culture that was being deliberately and systemically corrupted from within; culminating in the demoralized / amoral state of affairs where this...

"As a 19 then 20 year old boy, my managers and handlers taught me the ins and outs of mortgage fraud, drugs, sex, and money, money, and more money. My friend and manager handed out crystal methamphetamine to loan officers in a bid to keep them up and at work longer hours. At any given moment inside the restrooms - cocaine and meth was being snorted by my estimates more than a third of the staff, and more than half the staff manipulating documents to get loans to fund and more then 75% just completely made falses tatements on 1003s regarding stated income etc to get loans funded. "

http://www.freerepublic.com/focus/news/2184646/posts?page=8

...was considered to be bidness as usual -- from the liars who falsified their incomes on the mortgage application, the originators who helped them fill out the paperwork, the folks who securitized the resulting mortages, those who failed their fiduciary responsibility to rate the a$$paper accordingly... etc etc etc.

Evidently progressive "fiscal" conservatism... isn't.

As Liz succinctly put it:

18

posted on

01/08/2012 10:30:02 PM PST

by

LomanBill

(Animals! The DemocRats blew up the windmill with an Acorn!)

To: LomanBill

That same generation inculcated with moral relativity and situation ethics has segued into The Entitlement Generation.

The new motto is “Pay Me—I’m a Victim.”

19

posted on

01/09/2012 4:52:22 AM PST

by

Liz

To: All

Obama presided over the biggest political heist in US history. What the so-called "collapse" of the banking system wrought:

FOURTEEN TRILLION DOLLARS: Behind The Real Size of the Bailout; A guide to the abbreviations, acronyms, and obscure programs that make up the $14 trillion federal bailout of Wall Street

SOURCE motherjones.com

Mon Dec. 21, 2009 12:23 PM PST

The price tag for the Wall Street bailout is often put at $700 billion—the size of the Troubled Assets Relief Program. But TARP is just the best known program in an array of more than 30 overseen by Treasury Department and Federal Reserve that have paid out or put aside money to bail out financial firms and inject money into the markets.

To get a sense of the size of the real $14 trillion bailout, see our chart at web site. Below, a guide to the pieces of the puzzle:

Treasury Department bailout programs

(Remember that Obama's Treasury Dept was controlled by his then-COS Rahm Emanuel---a G/S lobbyist in the WH)

Money Market Mutual Fund: In September 2008, the Treasury announced that it would insure the holdings of publicly offered money market mutual funds. According to the Special Inspector General for the Troubled Asset Relief Program (SIGTARP), these guarantees could have potentially cost the federal government more than $3 trillion [PDF].

Public-Private Investment Fund: This joint Treasury-Federal Reserve program bought toxic assets from banks and brokerages—as much as $5 billion of assets per firm. According to SIGTARP, the government's potential exposure from the PPIF is between $500 million and $1 trillion [PDF].

TARP: As part of the Troubled Asset Relief Program, the Treasury has made loans to or investments more than 750 banks and financial institutions. $650 billion has been paid out (not including HAMP; see below). As of December 21, 2009, $117.5 billion of that has been repaid.

Government-sponsored enterprise (GSE) stock purchase: The Treasury has bought $200 million in preferred stock from Fannie Mae and another $200 million from Freddie Mac [PDF] to show that they "will remain viable entities critical to the functioning of the housing and mortgage markets."

GSE mortgage-backed securities purchase: Under the Housing and Economic Recovery Act of 2008, the Treasury may buy mortgage-backed securities from Fannie Mae and Freddie Mac. According to SIGTARP, these purchases could cost as much as $314 billion --- SNIP---.

LONG READ---go to web site to read more and checkout the shocking charts.

SOURCE http://motherjones.com/politics/2009/12/behind-real-size-bailout

20

posted on

01/09/2012 4:56:17 AM PST

by

Liz

Navigation: use the links below to view more comments.

first 1-20, 21-27 next last

Disclaimer:

Opinions posted on Free Republic are those of the individual

posters and do not necessarily represent the opinion of Free Republic or its

management. All materials posted herein are protected by copyright law and the

exemption for fair use of copyrighted works.

FreeRepublic.com is powered by software copyright 2000-2008 John Robinson