1 posted on

08/29/2014 1:58:24 PM PDT by

ckilmer

To: ckilmer

The biggest mistake the West has made in at least the last 20 years is allowing China to become an economic power.

To: ckilmer

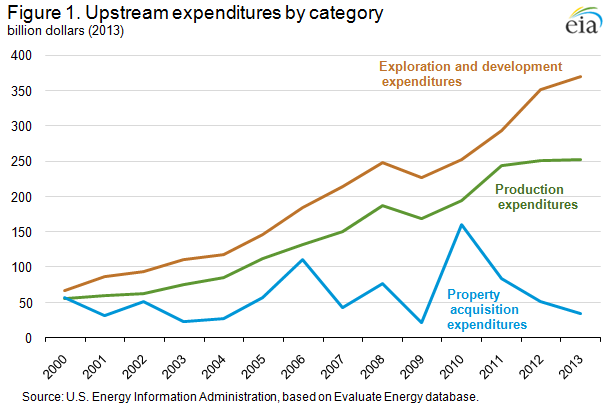

Upstream oil and gas spending continues to favor exploration and development activity

http://www.eia.gov/oog/info/twip/twiparch/2014/140416/twipprint.html April 16, 2014

For this analysis, EIA considered 42 U.S. and international oil and gas companies that have reported data on upstream expenditures since 2000. The companies range in size of production and include publicly traded as well as state-owned enterprises, including large producers such as ExxonMobil and Petrobras, and smaller ones such as Encana Corporation and Talisman Energy. The 42 companies made up approximately 39% of non-OPEC production in 2013, and had a combined market capitalization of more than $2.4 trillion.

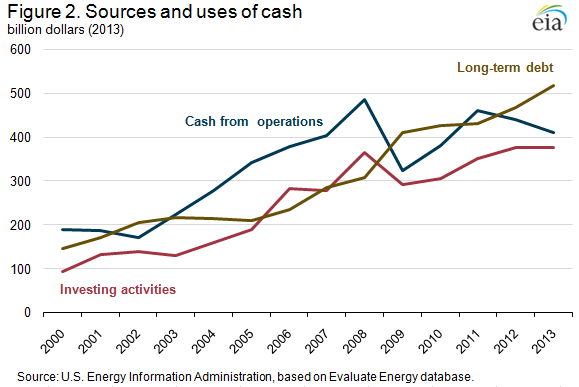

Generally rising oil prices from 2000 through 2011 contributed to large increases in the companies’ cash flow from operations (Figure 2) and provided the funds needed to increase upstream expenditures. As crude oil prices increased, projects that had been uneconomic became feasible. Companies significantly expanded operations related to tight oil production in the United States and oil sands production in Canada. With many companies expanding oil and gas production activities at the same time, costs for equipment and personnel also increased, further pushing up expenditures. Costs for raw materials increased as most commodities experienced a general price rise from 2002 through 2008, although commodity prices have come down since 2012. After the 2008-09 economic downturn, property acquisition expenditures slowed first, as spending shifted to exploration, development, and production.

Although oil prices remained relatively flat in 2012 and 2013, rising costs contributed to a decline in cash flow from operations. Nonetheless, cash spent on investing activities, which tends to lag changes in cash flow, increased slightly in 2013 as companies increased debt to maintain investment, taking advantage of interest rates that have been low since 2009. Companies have increased debt every year since 2006, with long-term debt increasing 9% and 11% in 2012 and 2013, respectively.

3 posted on

08/29/2014 2:06:24 PM PDT by

thackney

(life is fragile, handle with prayer.)

To: thackney

Your perspective would be valuable here.

4 posted on

08/29/2014 2:06:25 PM PDT by

wideawake

To: thackney; Kennard; bestintxas; nuke rocketeer; crusty old prospector

compare this story with thackney’s post about US midsize companies in the fracking boom—which if prices remain above +-$90@ barrel will go cashflow positive next year.

http://www.freerepublic.com/focus/f-news/3198117/posts

If they do go cash flow positive—it wouldn’t be unreasonable to think that a lot of the super major oil companies will try hard to buy into the US oil boom by buying midsize US oil companies.

My vote of course would be that US oil companies stay out of foreign hands and especially foreign state controlled company hands. If anything I’d rather the US midsized oil companies got too big fast for the super majors to gobble up.

5 posted on

08/29/2014 2:07:57 PM PDT by

ckilmer

(q)

To: ckilmer

This article is from a Peak Oil website, as in Chicken Little.

A major problem with this analysis is that companies are expensing, rather than capitalizing E&P activity.

To: ckilmer

"...127 of the world's largest oil and gas companies are running out of cash."

Except for those that got cozy with the Democrats and have refineries, too. Regular unleaded near tourist areas on the Rockies is still around $4 a gallon.

11 posted on

08/29/2014 3:43:03 PM PDT by

familyop

(We Baby Boomers are croaking in an avalanche of corruption smelled around the planet.)

To: ckilmer

And those new gas folks weren’t satisfied with their Democrat-tied move against U.S. coal. They’re bragging about cheating the Canadians, too. That will come back to bite ‘em. Canada will be a real net energy exporter for the foreseeable future, oil sands and conventional, and has the attentions of the bigger investors. Some constituents have also been running interference for the Russian threats against Canada—very stupid and traitorous policy.

12 posted on

08/29/2014 3:51:57 PM PDT by

familyop

(We Baby Boomers are croaking in an avalanche of corruption smelled around the planet.)

FreeRepublic.com is powered by software copyright 2000-2008 John Robinson