Posted on 04/06/2014 11:34:34 AM PDT by expat_panama

This is the thread where folks swap ideas on savings and investment --here's a list of popular investing links that freepers have posted here and tomorrow morning we'll go on with our--

Open invitation continues always for idea-input for the thread, this being a joint effort works well.

Keywords: financial, WallStreet, stockmarket.

|

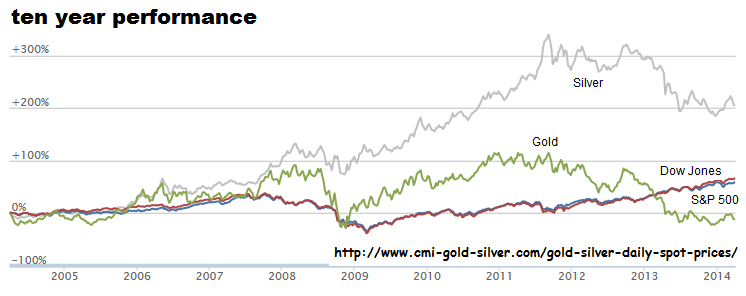

====================== A heck of a week, gold'n'silver lept back up and stocks plunged back down --10 year performance: (click pic to enlarge

Of course, while that's all well and good for what's been happening til now (telling us what we shudda done) but the plan we need now is for what we're supposed to do tomorrow. IBD TV mentions that last Friday's drop means the market's officially in a correction now, and they say it means we got to reduce holdings and show patience with new buys. |

|

Makes sense considering that stock price patterns are typically self-similar (English translation: "the trend is your friend"), but for the heck of it I checked out past IBD trend calls and saw that recent history showed--

---that correction beginnings have been great buying opportunities. Don't get me wrong, the IBD people aren't idiots and stock timing is not best done by throwing darts at a colander. The IBD editors stress that everyone's got his own set of goals for return risk/v/reward, and we all make our own choices.

|

Let's compare choices; I'll start. My choice is see what Monday brings and my stocks will either work for me or get replaced by EFT's (YAHOO's got a neat eft finder/screener here).

Hang on. Today may be interesting. Pall on the faces at CNBC

Yeah, am thinking we got a lot of folks pi$$ed that just as things were beginning to look like we were crawling our of our hole--

--that suddenly interest rates would have to creep back up....

NYSE MAC DESK MID-DAY MARKET UPDATE:

DOW 16,065 (-104 points), S&P500 1822 (-10 handles), Brent Crude $107.70/barrel (+$0.24), Gold $1,318.60/oz. (-$1.50)

MARKET DRIVERS: (Stocks are continuing their slide amid some mixed bank earnings and despite a much better-than-expected consumer sentiment reading.)

• The University of Michigan consumer sentiment index rose in April to 82.6 – the highest level since July – topping Street economists’ consensus which called for a lower reading of 81.

• According to the Labor Department, U.S. PPI (producer price index) rose by a seasonally adjusted 0.5% in March, from -0.1% in the preceding month. Analysts had expected U.S. PPI to rise 0.1% last month. (It marked the largest monthly increase since last June.)

• China’s consumer price index rose 2.4% from a year earlier in March, up from 2.0% in February and right in line with consensus expectations.

• Germany’s consumer price index rose 1.0% from a year earlier in March, unchanged from February’s pace and in line with consensus estimates.

• In the IPO-space, we had three more come to the NYSE this morning: 1) Fast-casual Mediterranean restaurant Zoe’s Kitchen (ZOES) priced 5.8 million shares at $15, high end of the upwardly revised $13 to $15 range. Shares are currently trading at $25.80! Also: 2) Farmland property REIT Farmland Partners (FPI) priced 3.8 million shares at $14. 3) Nat gas and crude oil LP Enable Midstream Partners (ENBL) priced 25 million shares at $20.

At its last minus-tick, the S&P 500 index is now down 1.18% year-to-date. That’s it! Minus 1.18%, y-t-d!! Listening to some of the talking heads on the financial networks, you’d think that Armageddon was imminent!!(?) Here are a few thoughts we’d like to share with those panic-stricken talking-heads in the hope that we might be able to coax a couple of them off of the ledge… 1- Market players have been obsessed with a modest number of high-beta biotech and internet names which enjoyed explosive upside moves throughout this most recent bull-run. 2- What we are seeing is a rotation out of these 3 or 4 dozen ‘high beta/big momentum’ names and INTO dividend paying names, (like utilities and REITs), energy stocks, telecom and ‘old school’ tech stocks. Case in point, while some high beta names are down as much as 20%+ over the past 30 days, utilities are up 5.8% and telecoms are up 5.6% as money is “rotating” into these sectors. 3- Finally, for those of you who are wondering when the market is going to turn around and go higher again; we’d like to direct you to the splendid chart of the S&P 500 that I have cut-and-pasted below. Specifically, please direct your eyes to the green wavy line which represents the 100-day moving average for the index… You will notice that, over the past year, the Index has briefly fallen through the average five times, (June, August, October, early February and TODAY). Now, please look at the “Relative Strength Index – RSI” chart located at the bottom of the illustration. Each of the other four times that the S&P broke below its 100-DMA, the RSI dipped below 40, (to as low as 31.5 in February), before a rally ensued. With the RSI currently at 40.8158, I say we give it another few days before we can expect to see the “Rally Boys” come to the rescue… Again – not to belabor the point – the S&P 500 is only down 1.18% on the year, so relax, take a deep breath, pour yourself a cocktail after work and enjoy the weekend… Moving on, the Dow has settled into a narrow trading-range near session-lows, and volume remains heavier than normal, with ~285M shares on the tape at this time… Internally, breadth is mixed with issues and volume bearish while new highs to new lows are bullish (positive divergence). Advancing Issues: 1481 / Declining Issues: 2746 — for a ratio of 0.5 to 1. New 52-Week Highs: 67/ New 52-Week Lows: 63… Technically, 1819 represents critical support in the S&P. Thankfully, we bounced off that level this morning… Meanwhile, in the trading pits the 10-year US Treasury is trading flat following yesterday’s jaw dropping scramble/flight to safety trade that pushed the yield down to the 2.63% level… It is amazing to me how much money is piling into the 10-year at such a low yield. Might be telling us that US economic growth won’t be all it’s cracked-up to be this year… Stay tuned… Baseball trivia follows... Have a tremendous weekend!

Sector Highlights brought to you by http://www.streetaccount.com/

• Consumer discretionary underperforming with the S&P Consumer Discretionary Index (0.5%)

o Retail underperforming with the S&P Retail Index (0.7%), extending yesterday’s ~3% sell-off. JCP (8.6%) and SHLD (3.8%) leading the department stores lower. Not seeing any specific catalyst behind the JCP move. Stock now down >12% on the week. ARO (4.3%), LB (2.4%), EXPR (2%) and GPS (1.5%) the notable underperformers among the apparel names. GPS missed March comps expectations and said it expects Q1 gross margins to decelerate further from last quarter. The stock was downgraded at Janney Capital, which notes margin pressure as well as increasing promotions. CE space underperforming with HGG (3%), RSH (2.7%) and BBY (2%). FDO (1.9%) continuing its post-earnings move lower.

o Footwear and sporting goods underperforming. CROX (2.5%), DECK (2.5%) and DSW (1.7%) the laggards. DSW now down >6% on the week. SKX (1.1%) continuing its move lower from yesterday, when it fell 5.2% after Buckingham initiated the stock underperform. UA +1.2% the notable gainer in the space, recovering some of yesterday’s 5.9% losses.

o Autos mixed. GPI (1.8%) and GM (1.7%) the notable decliners. The latter confirmed a $1.3B charge in Q1 due to recall-related repairs. Note reports that the company may look at all senior level executives, including CEO Mary Barra, in relation to the ignition-switch issues. TM +2.2%, HMC +1.9% and F +1.6% the notable outperformers. TM was upgraded at both Jefferies and Mizuho Securities. F was upgraded at Deutsche Bank.

o Restaurants relatively outperforming after yesterday’s underperformance. CBRL +1.1%, RT +1%, JACK +0.9% and DNKN +0.6% leading the way higher. Recall RT rallied ~12% yesterday on an earnings beat. Stock now up >20% on the week. WEN (0.9%) and TXRH (0.8%) the notable underperformers.

o Other notable performers: CVC (2.1%), KORS (1.7%), MGM +1.5%

• Financials underperforming with the S&P Financials Index (0.5%)

o Banking group lagging with BKX (0.2%). Q1 earnings season began today with JPM (2.5%) and WFC +1.8% showing mixed results, although both banks showed weakness in mortgage banking. JPM the laggard after top and bottom line miss, with analyst commentary highlighting broad-based weakness. WFC outperforming as earnings and revenue beat, with slowing mortgage business offset by better expense controls and stronger credit quality. BAC (0.2%) also lower, while regionals performing better with KRX +0.4%.

o Insurers mostly lower. GNW (1.5%), HIG (0.7%) and LNC (0.5%) lagging, while AFL +0.8%, ACE +0.6% and TRV +0.4% outperform.

o Online brokers outperforming. Recovering some of the week’s losses with AMTD +1.1%, ETFC +0.8% and SCHW +0.4%.

• Materials underperforming with the S&P Materials Index (0.5%)

o Industrial metals underperforming. Worries about slowing growth out of China cited as a headwind. Steel space led lower by AKS (3%) and X (2.3%). Note the steel equities have had a nice run up over the past few weeks, amid a flurry of positive catalysts including price hikes, positive sell-side commentary and Chinese stimulus measures. AA (1.7%) and KALU (1.2%) the notable decliners among the aluminum names, while CENX +1.1% outperforms. ACH (0.6%) stable after its ~9.5% rally yesterday. CLF (2.2%) the other notable performer among the industrial metals.

o Precious metals equities mostly lower. Underlying assets slightly lower today, with SLV (0.1%) and GLD (0.1%). NEM (1.4%) and GG (1%) the notable decliners. Upside limited, with ABX +0.7% the notable outperformer.

o Other notable performers: CF (1.8%)

• Utilities outperforming with the S&P Utilities Index (0.1%)

o Sector remains the big beneficiary of the heightened risk aversion and defensive rotation in equities that has also driven the rally in Treasuries. In addition, it has been the best performing sector in 2014. According to Bespoke, since the start of WWII, sector is having its sixth best year vs broader market. Also note that while Q1 earnings sentiment has been negative, utilities has been the only sector to actually see an upward revision to growth expectations since the start of the quarter. At the same time however, there has been some focus on technically overbought conditions.

• Energy outperforming with the S&P Energy Index +0.2%

o Continuing on from yesterday’s outperformance, aided by recent rise in crude oil prices. WTI +0.7% to $104.08 today. Natural gas (0.8%) lower on the day after this week’s strong rally.

o Majors outperforming. COP +2.3% the leader, rebounding from yesterday’s decline. Yesterday’s analyst day was generally met with positive reaction, however modest downward revision to 2014 volume guidance seemed to be focus of yesterday’s price decline. COP upgraded at Morgan Stanley. CVX +0.7% also outperforming, while BP (1.1%) lags.

o Refiners underperforming. WNR (2.1%) lagging, with HFC (1.9%), TSO (1.7%) and VLO (1.3%) also underperforming.

o Coal broadly lower. WLT (4.4%), ANR (3.4%) and BTU (2.4%) the laggards.

o E&Ps outperforming with the EPX +0.4%. KWK +2.3%, WTI +2.1% and SWN +1.5% among the best performers.

• Healthcare outperforming with the S&P Healthcare Index +0.2%

o Biotechs outperforming and rebounding from yesterday’s sharp sell-off, when the NBI and IBB both fell more than 5%. NBI +1.4% and IBB +1.4% today. GILD +4.7% and INCY +4% leading the way higher. The former announced results the phase 2 studied of GS-US-334-0125 and GS-US-334-0126. RGDO (15.9%) the notable laggard after a secondary share offering.

o Pharma mostly lower with the DRG (0.2%). Downside rather limited, however, with PRGO (1.1%) and MYL (1%) the notable underperformers. ACT +1.3% and MRK +1.2% the notable gainers.

o Other notable performers: SPNC +3.4%, WCG (4.3%). The former received FDA clearance for two medical lead extraction devices. Recall WCG shares rallied in the afternoon yesterday on takeover speculation.

People selling stock to cover taxes? Everyone I’ve talked to has just gotten slammed with tax payments...

That would explain a lot of the trades being made as well as fit nicely into my political views, but I’m thinking the vast majority of shares are traded by institutions whose taxes don’t come due on April 15.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.

)

)

(click pic to enlarge)

(click pic to enlarge)