Ah, now that something sensible to discuss. I can see a context.

Without spending lots of time recalling minute details, my take was that due to gov’t-compelled sure-loss loans (to wit mortgages unlikely to be repaid), banks had to invent a new process for insuring such high-risk loans; plethora of acronyms for misunderstood terms aside, upshot is that everyone involved was confident the lenders-insurance system was a solid AAA worthy construct.

Until everyone realized everyone was, in effect, insuring themselves with nothing. AAA -> junk status overnight.

Not so much fraud as doing government’s will under duress, and concocting some way to make it work, which it can’t and doesn’t. Subsequent repair of “progressive” damage is very, very expensive; at some point the rate of quantitative easing will be unable - at _any_ rate - to keep up with demands for payback. A run on dollars will ensue; hyperinflation occurs when there is simply not enough value in the system to satisfy current obligations.

Casting blame doesn’t help at this point. There just isn’t enough value in the system to satisfy obligations as they occur. Result: crash; those whose wealth depends on the value of the dollar won’t have any.

>>banks had to invent a new process for insuring such high-risk loans

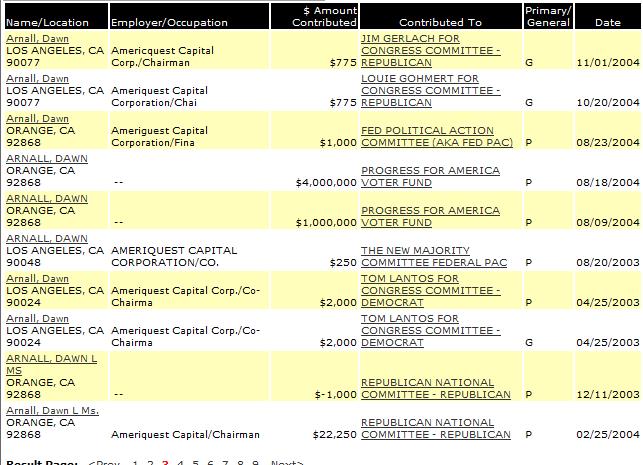

The Sub-prime leader for some time was Ameriquest/Argent Mortgage.

They were not a bank. They had no depositors.

http://www.ocregister.com/articles/subprime-14214-beach-mortgage.html

They existed only for the origination and securitization of subprime loans.

"Oops"

"Oops"

That would be W with his Ambassador to the Netherlands - Roland Arnall, the "Godfather of Subprime"

>>Not so much fraud as doing government’s will under duress,

Baloney.

Argent Mortgage falsified FICO scores for thousands of loan applications.

I know that for a fact.

Other entities manipulated LIBOR, to which a significant portion of Argent's originations were tied. Not surprising, given that their primary warehouse lender was Deutchesbank.

Did the gooberment force them to do that? Nope.