Posted on 05/03/2013 7:05:30 AM PDT by SeekAndFind

One of the darkest risks facing America is that so few of us are prepared for retirement.

It's shocking, really. According to ConvergEx Group, "Only 58% of us are even saving for retirement in the first place. Of that group, 60% have less than $25,000 put away ... a full 30% have less than $1,000." According to Nielsen Claritas, Americans age 55 to 64 have a median net worth of $180,000 -- less than they'll likely need for health care spending alone during retirement.

I recently asked Joseph Dear, chief investment officer of CalPERS, one of the world's largest pension funds, whether America was ready for retirement. Without delay, he snapped: "No!"

We have a retirement problem. A very serious one that shouldn't be discounted.

But it is nothing new.

Same as it ever was

The notion that these challenges are new -- that there was some golden era when Americans were prepared to kick up their feet and enjoy retirement in financial security -- is a myth. By some measures, retirees are in a better position today than at any other time in modern history.

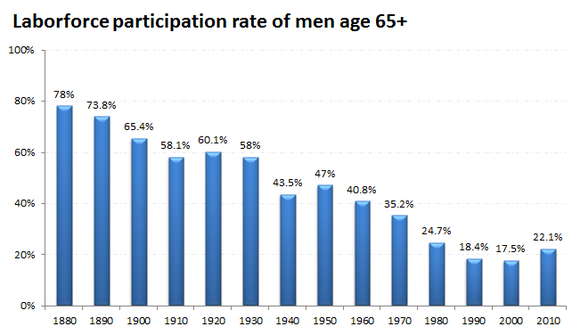

Let's start with something simple. The entire concept of retirement is unique to the late-20th century. Before World War II, most Americans worked until they died.

The best way to show this is the labor force participation rate for men age 65 and up:

Source: Economic History Association, Bureau of Labor Statistics.

For most of us, I think the nostalgic sense of America's golden era of retirement is set between the 1950s and the 1990s. That, we often hear, is when workers had pensions and were able to retire with security. But as much as twice the percentage of men were still working into their elderly years back then compared with today.

The truth is, that 20th century was brutal for most elderly. As Frederick Lewis Allen writes in his 1950 book The Big Change: "One out of every four families dependent on elderly people and two out of every three single elderly men and women had to get along in 1948 on less than $20 per week [$193 in today's dollars]."

There are a couple of reasons for this. First, those retiring in the 1940s, 1950s and 1960s, were in their prime earning years during the Great Depression. Not exactly fertile ground for saving.

More importantly, Social Security used to pay out much smaller benefits, even adjusted for inflation.

When Ida Mae Fuller cashed the first Social Security check in 1940, it was for $22.54, or $374 in current dollars. Today, the average monthly benefit in real (inflation-adjusted) terms is more than three times larger. Since payouts are set with a calculation based on wage growth, not just price inflation, real Social Security benefits have risen consistently over the last half-century:

Sources: Annual Statistical Supplement to the Social Security Bulletin, 2012; Bureau of Labor Statistics.

But hold on, I hear you say. Didn't workers have private pensions to rely on in previous decades?

Some did, yes. But only a minority. There has never been a time in American history when the majority of retirees took in income from either a private or public pension (outside of Social Security). Nothing close to it, in fact.

Nevin Adams of the Employee Benefit Research Institute tells the story: "Only a quarter of those age 65 or older had pension income in 1975 ... The highest level ever was the early 1990s, when fewer than 4 in 10 (both public- and private-sector workers) reported pension income."

Mr. Adams continues: "In other words, even in the 'good old days' when 'everybody' supposedly had a pension, the reality is that most workers in the private sector did not."

Here's what's really interesting. In 1975, 15% of all income reported by those 65 and older came from pensions, according to Adams. By 2010, that figure actually increased, to 20%.

The bottom line, Adams writes, is that "even when defined benefit pensions were more prevalent than they are today, most Americans still had to worry about retirement income shortfalls."

As a matter of fact, retirees had a lot more to worry about in past decades than they do today.

The Census Bureau's measure of poverty -- based largely on how much of a household's income is devoted to basic food necessities -- for those age 65 and up has plunged since the 1960s, continuing to fall even during the financial crisis:

Source: Census Bureau.

By this metric -- and I struggle to think of a more complete measure of financial wellbeing than poverty -- those age 65 and up have never been in better financial shape.

What about age?

The most common rebuttal to what I've presented so far is likely that we're living longer today than we were in the past. So, even if retirees have higher incomes and more security today, they need it because they have to finance a longer retirement.

There is some truth to this, but probably less than many assume.

While there has been tremendous progress in life expectancy over the last century, most of the gains have come to the young.

According to the Centers for Disease Control's actuary tables, someone born in 1950 could expect to live to age 68.2, while someone born in 2010 could expect to live to 78.7.

That's extraordinary: An extra decade of life expectancy gained inside of two generations.

But the gains have been much smaller for those who survive into their retirement years. A 65-year-old in 1950 could expect to live 14 more years, while a 65-year-old in 2010 could expect to live another 19 years. The gains continue to diminish from there. A 75-year-old in 1980 (the earliest we have data on for that age group) could expect 10.4 more years of life. Today, they can expect another 12 years -- a gain of a mere 1.6 years.

Just like the good old days

Let me clearly state what these statistics do not show. They do not show that Americans are prepared for retirement, or that there is no retirement crisis.

There is a retirement crisis.

But there always has been one.

The lack of savings is a grim problem that will affect millions of Americans for decades to come.

But that's nothing new.

Most retirees will have to cut back on their standard of living.

But they always have.

Many will be reliant on Social Security.

But that's been the case for decades.

"When all is said and done," Adams writes, "we're all still challenged to find the combination of funding -- Social Security, personal savings, and employment-based retirement programs -- to provide for a financially satisfying retirement."

"Just like in the 'good old days.'"

I don’t think so but it is possible. If say, the wife never worked, she might get more social security if she divorced the husband. I would never advise it since it would put her at risk going forward if husband decides to leave her but I suppose with the right agreement and estate plan it could be done. In Kansas however they would be common law married which could complicate things. There probably are people doing this. I did have a case once where the wife wanted to take care of a seriously disabled man but could not receive state aid for doing so since she was his wife. She divorced him, set up a separate address at the home, and continued living there.

I agree with you wholeheartedly....

except for the car thingie...

I buy em new and then drive them till they are dead..

what most people fail to accept is that your retirement is a bill, just like all your other bills..

it gets paid monthly, regardless...

and yes, EVERYONE can put something away, but that means doing without fancy cars, vacations, expensive furniture, eating out, etc...

living frugally is a lifestyle...

wifie and i were at one time both making just above minimum wage, with a house and 2 kids, and still put money away, we just did without the fancy stuff...

“Even with a very nice IRA and savings, I’m already looking for a large refrigerator’s empty box which I can live in, in a vacant lot, away from the city.”

I’m planning to live in a van down by the river.

That. One of the best posts I’ve ever seen in any personal finance related thread in the twelve years I’ve been a FReeper. I would add to the “it’s how much you spend” part of the plan by saying “it’s not how much you make, it’s how much you keep.”

The plan you describe works nearly every time it’s tried.

____________________________________________________________

I agree...found the post very thoughtful/helpful in explaining retirement financials.

We’ve put aside retirement funds since I was in my early 20’s. Always 15-20%...between retirement and personal savings. I just always went on the assumption that SS would not be there when I retired and so I had to be able to have enough put aside. The DH always put aside around 10-15% of his earnings as well (between retirement and savings). He also has a defined retirement plan.

We’ve been fortunate that our kids and grandkids have been self reliant and have never needed a ‘hand’. And they’ve been building their own nest eggs since they all started working.

I think for us, it’s our German/Dutch heritage...frugal and thrifty. :) And self reliant when it comes to finances.

Right now, today, this afternnon, or as soon as you can, should you be BEFORE retirement time or age, do this simple mathematics exercise.

If you are renting, outside of big cities, figure 3% a year MINIMUM.

If you are paying for cable connections, figure 5% a year MINIMUM.

Your light bill, for the sake of the exercise, figure 10% a year, MINIMUM.

Your telephone bill, again, for the exercise, figure 12% a year, MINIMUM.

Your auto gas bill ... the year before Obama was locally, $1.44 a gallon. It has gone up to $3.84 on the roller coaster. This is year 5, no? That’s $2.44 in 5 years, or

%0.588 a year. Remember, that is locally.

The cost of a loaf of bread, not made by the local now-shut-down Hostess bakery, has risen EQUAL to the price of auto gas! That does not count, those nice rye bread loaves, that cost $4.00 each.

Use these as indicators for the years ahead you have until you retire. Figure what your budget might be with those inflated costs, and decide if you can afford to retire, from THAT budget.

If you are buying the house, yes, you may reach the end of the mortgage, but you will never reach the ‘end’ of taxation upon that house! Don’t forget those figures, either.

Maybe the problem is that Americans expect to retire. It’s a relatively recent notion that was put forth to sell Social Security was it not?

In generations before that, when the elders were no longer able to work, their children took care of them.

Work and save all your life, retire, have a health issue, the government takes every dime of your money and throws you in a shitty nursing home on Medicare where you’ll eat tapioca pudding through a straw for your remaining days. Is that the “retirement” we are not ready for?

OK, I have a coupon for the Big Mac. What color will your refrigerator box be?

With retirement the feds lose tax money why would they want to help you to retire?.

I won’t be able to afford those ritzy neighborhoods.

Biggest and most powerful defense against personal economic disaster? The intact traditional family....Dad, mom, the kids, grandparents, aunts, and uncles. Add hard work and traditional values and you have the number one threat to liberal thinkers and career politicians.

I may have to draw SS anyway. Not because I need the money, but to punish my co-workers for being young. ;-)

I’ve come to the conclusion that God meant for Man to work as long as he could.

That is my plan. The house is paid off when I reach 70. Can’t retire before then. Work at least that long, and I’m thinking 72, socking some money away into the 401K. You can do that, so I’ve read.

I turned 65, today, so I’m thinking 7 more years. I’m in good health; I like what I do, the company I work for; the people I work with. Why not? I knew a man who was still working at 80.

How many of the percentage of retired people were government workers and how many were private sector?

I’m not going to worry if I DO win :)

My only issue is the older I get the less I am able to keep up with the new techie stuff. I just don’t have it in me to work 12-14 hours a day with the hipsters anymore. Going from lead engineer to a dev manager role helped.

So, I may have to change careers which is darn near impossible over 55 unless you self-employ or downgrade.

If anything beyond basic metallography, fracture analysis, hardness testing, and chemical analysis is needed, I send it out. I still have to put it all together for the report at the end, though.

Maybe, when I retire, I'll just get a part time, say 3 day-a-week job, for fishing money, or something.

I've trusted in the Lord all my life, sometimes with more faith than at others, and so far, it's worked out pretty well for me.

“Assuming businesses will hire you...”

Start your own business. Be self employed. Develop skills that people will pay for.

In the socialized 21st century, those who saved will be ripped off for the benefit of those who did not. It’s not fair, you see, that some scrimped and saved their whole lives and have more.

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.