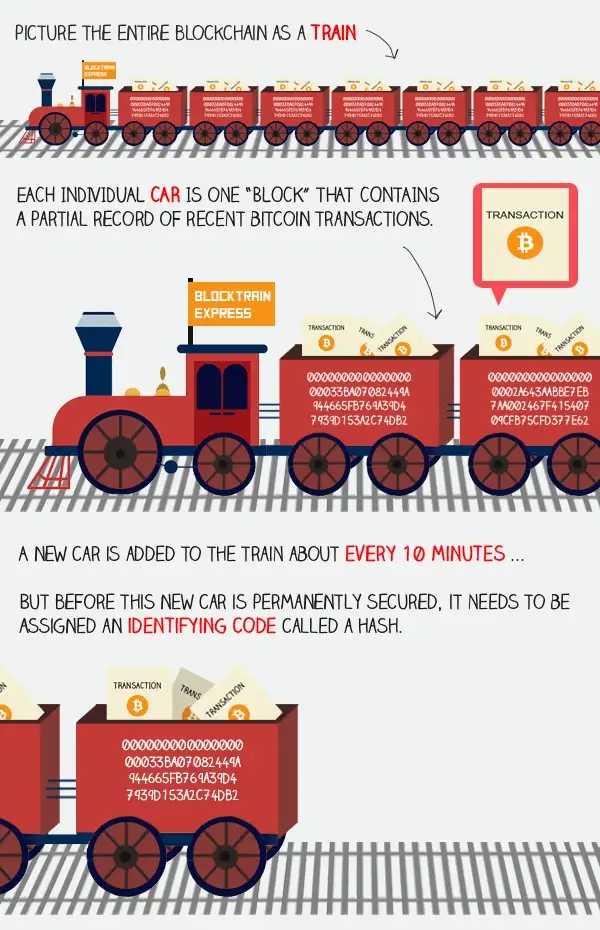

Imagine that the blockchain is a loooong train — a blocktrain, if you will.

This train contains a public record of all bitcoin transactions. Each time a trade is made through a cryptocurrency platform like Coinbase, the details of the transaction are coded and broadcast, along with other transactions, to a vast network of users called bitcoin miners.

From there, the following process unfolds:

- Miners compete to add the next car to the train by bundling up a bunch of transactions into “blocks.”

- Miners solve a computational problem (called “proof of work”) that assigns the block an identifying code (a hash).

- The “winning” block is distributed to, and verified by, all the other miners in the network and is added to the blockchain.

Only one car can be added to the train at any given time, and each one takes ~10 minutes on average to verify and attach.

These bitcoin miners serve 2 major functions:

- They are the printing press of bitcoin: Adding new blocks to the blockchain is the only way to release new bitcoin into circulation.

- They are the auditors of bitcoin: Through the process of mining, they verify the legitimacy of all transactions on the blockchain.

By solving the equation first and adding the next block to the chain, a miner is rewarded with a set amount of bitcoin.

When bitcoin mining first started, the reward was 50 bitcoin (BTC). But as dictated by the coin’s creator, the reward is cut in half every time 210k new blocks are added to the chain — or roughly every 4 years.

As of February 2021, miners receive 6.25 bitcoin for every new block they mine — or ~$294k based on the current market value. They also get to keep the transaction fees from the trades in that block, which are currently around $20/trade.

Today, it’s estimated that there are more than 1m bitcoin miners in operation — and they’re all competing to add the next block to the chain.

Combined, the rewards these miners earn top $1B per month.