Posted on 11/10/2025 6:56:25 AM PST by Red Badger

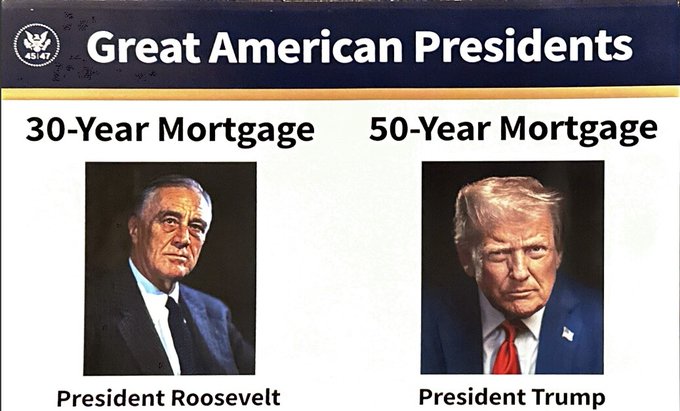

President Trump likes to test policy proposals on social media.

This was his newest one, shared by Bill Pulte, the U.S. Director of Federal Housing and the chairman of Fannie Mae and Freddie Mac 👇

Thanks to President Trump, we are indeed working on The 50 year Mortgage - a complete game changer. https://t.co/HZDPzO0qJG— Pulte (@pulte) November 8, 2025

A 50-year mortgage would result in a slightly lower monthly payment, stretched out over 5 decades, with hundreds of thousands of extra dollars in interest.

The reactions were not kind.

But they were funny!

MANY TWEETS AT LINK>........................

I think it's safe to say that this proposal might end up in the "no-go" category.

(Excerpt) Read more at notthebee.com ...

Sigh, I know.

I *am* a conservative. And there just *IS* no other reasonable political tent for me.

With a tough midterm coming up, I just want to at least have my say.

We all know the leftists would be even worse, but I just really want my 2 cents to stop that point where I’m just... done. Out.... Left in a place where there is NO party or vote for me.

I was banned when Trump was banned. When Musk took over, I just requested to have my ban reviewed. 5 minutes later, I was back on.

This is what has been happening in Italy for ten years or more.

Housing prices were dropping. To the point that in a lot of the rural villages houses were almost worthless. Give them back to the state. The state then sells them for 1EU IF you agree to fix them up and live in them.

This is not the case in the larger cities of tourist areas. Especially, IF you can rent your apartment/house on AirBnB.

You can still buy plenty of nice houses in southern Italy close to the Med for well under $400K.

This is all because Italians are not having enough BAMBINOS.

Incomes around here are rather high.

Per google AI:

County Median Annual Tax Bill Average Effective Tax Rate (as % of market value)

Nassau Approximately $11,613 (as of March 2025 data) Around 2.10% - 2.24%

Suffolk Approximately $9,500 - $10,000 Around 2.37% - 2.42%

“The math *rarely* works out in the manner you suggest.”

Please cite my math in the post you replied to and explain why it rarely works out.

“Your math simply does not work in all but the once-in-a-lifetime rare situation where someone well-capitalized and financially astute finds a sweet spot.”

Not true.

If you disagree please cite my math and explain how you disagree.

“Your math simply does not work in all but the once-in-a-lifetime rare situation where someone well-capitalized and financially astute finds a sweet spot.”

My math works right now even for the average person who may not be financially astute.

Not a “once-in-a-lifetime rare situation”

“Those situations simply do not come around very often.”

Came around for me six times over the last 50 years.

“Maybe Trump thinks the answer to the giant federal debt is to redo it in 100 year bonds.”

Where have you been hiding?

It’s a terrible idea, not the least of which is that it doesn’t actually make the house that much more affordable.

Let’s take an example, let’s say you buy a house for $400,000, $100,000 down and $300,000 loan with a 6% interest.

At 30 years, your monthly payment is $1,798.65 per month, with a 50 year mortgage, your monthly pay is $1,579.21 per month, so roughly $210 per month. Basically a 11% reduction in payment but a 67% increase in the length of the loan.

The total payment you pay to the bank is $647,515 in the 30 year scenario, take out the $300,000 principle and it is $347,515 in interest. Your total payment to the bank in the 50 year scenario is $947,529, or $647,529 in interest.

You you essentially double your interest payment, increase the length of the loan by 67%, all for a 11% reduction in monthly payment, the only one who wins in this deal is the bank, and the builder who can sell you the bigger house.

If the $210 savings is the difference in one’s ability to buy a house, then they should just buy a cheaper house.

I’m just grabbing the first google result I got - and SmartAsset at least has fairly proper calculators - but my point is that amortization schedules are not linear.

https://smartasset.com/financial-advisor/amortization-table

The longer the note, the more of even FIXED rates are going to pay the interest on the note first.

Sure - you can pre-pay/pri-pay (but I’ll emphasize again, if you can afford a big payment? Why go 50 — or even 30 - if you can go 20 or 15?)

It’s just NOT a straight line; it’s a curve. It’s just how basic finance works.

The link above is a 7% over 30 - but bump that to 50? Yikes.... Now you’re *really* at the mercy at inflation, hoping you didn’t over pay, you’d damn well better have put down a big down payment, and hoping you bought in an area where your property appreciates and doesn’t run into a bubble crash or otherwise do anything other than appreciate.

There are absolutely some niche situations where a *smart* buyer might well find a perfect storm: Ridiculously low fixed rates (like 2021 or so), big down payment (at least, 20% or so), and it *absolutely* makes sense to take the longer term loan.

Like I said, my son and DIL got lucky to hit a sweet spot — the spread between a 15 and 30 fixed was less than 25 basis points. That’s a no-brainer. Take the 30. But that is EXCEEDINGLY rare... to the once-in-a-lifetime (if even that) situation.

They could/can self-amortize down to 15 easily - but at a 2.75 fixed? When even basic MM yields are 3-4%? Why bother.

However, I doubt we’ll EVER see that again... On a *50* year? You’ll be paying the interest by a huge ratio far longer.

It’s “rent to own”.... and that never works out well over the long term.

Exactly.

I’d normally lean more towards “buyer beware” and the idea that fools will be separated from their money regardless, but I’ll reiterate:

I highly suspect theoretical 50 yrs are going to be weighted towards FHA-backed loans; which is gonna put the taxpayer on the hook.

It’s going to artificially constrain the market, even if you eliminate the FHA? By putting people in homes/mortgages they’ll be stuck with for 10+ years.

I guess if you solve the former? Maybe I don’t care about the latter... Eliminate FHA loans and the only people who buy 50 yr notes are savvy (or well-capitalized) borrowers that can get a private lender to underwrite. I’m skeptical there’s a big market for that, but maybe.

Forget the 2008 subprime crisis - you’re creating the mother of all landmines so long as home lending continues to work the way it does.

That was during the real estate bubble in the 80’s . 35 years is standard in Japan .

Disclaimer: Opinions posted on Free Republic are those of the individual posters and do not necessarily represent the opinion of Free Republic or its management. All materials posted herein are protected by copyright law and the exemption for fair use of copyrighted works.